Market Overview

The pp compound for automotive market is expanding steadily due to increasing demand for lightweight materials, improved fuel efficiency standards, and rising adoption of polymer-based automotive components. Polypropylene compounds are widely used in interior, exterior, and under-the-hood applications due to their excellent balance of strength, durability, and cost efficiency.

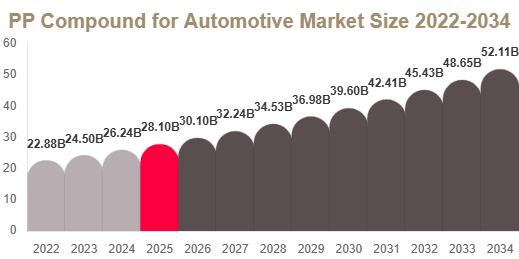

Market Size

The global pp compound for automotive market size was valued at USD 32.48 billion in 2025 and is projected to reach USD 34.15 billion in 2026. By 2034, the market is expected to reach USD 58.72 billion, growing at a CAGR of 7.1% during 2025–2034.

Get Your Sample Report Here: https://www.redlinepulse.com/report/pp-compound-for-automotive-market/request-sample

Buy Now: https://www.redlinepulse.com/report/pp-compound-for-automotive-market

Market Trends

Shift Toward Lightweight Automotive Materials

A key trend in the pp compound for automotive market is the shift from metal-based components to lightweight polymer materials. Automakers are increasingly adopting PP compounds to reduce vehicle weight, improve fuel efficiency, and meet stringent emission regulations.

Increasing Use in Electric Vehicles

Electric vehicle manufacturers are using PP compounds extensively in battery housings, interior trims, and structural components to reduce overall vehicle weight and extend driving range.

Market Drivers

Rising Demand for Fuel-Efficient Vehicles

Global regulations on carbon emissions are pushing automakers to improve fuel efficiency. PP compounds help reduce vehicle weight, directly contributing to lower fuel consumption and improved performance.

Growth in Automotive Production

Increasing vehicle production in emerging economies is boosting demand for cost-effective materials like PP compounds. Expanding automotive manufacturing hubs in Asia Pacific are significantly driving market growth.

Market Restraint

Volatility in Raw Material Prices

The PP compound market is highly dependent on crude oil derivatives, making it vulnerable to price fluctuations. This affects production costs and profit margins for manufacturers.

Market Opportunities

Expansion in Electric Vehicle Lightweighting

The rapid growth of electric vehicles presents major opportunities for PP compounds due to their lightweight nature and ability to replace heavier metal components.

Development of Sustainable Polymer Compounds

Manufacturers are investing in recyclable and bio-based PP compounds to meet sustainability goals and reduce environmental impact in automotive production.

Segmental Analysis

By Application

According to Redline Pulse, interior components dominated the market with a 44.62% share in 2025 due to extensive use in dashboards, door panels, and seating structures. Exterior components are expected to grow at the fastest CAGR due to increasing demand for lightweight bumpers and body panels.

By Vehicle Type

Passenger cars accounted for a 62.38% share in 2025 due to high production volumes and rising consumer demand. Commercial vehicles are also increasing usage of PP compounds for durability and cost efficiency.

By Material Type

Talc-filled PP compounds dominated with a 51.19% share in 2025 due to improved stiffness and heat resistance. Mineral-filled compounds are growing steadily in automotive structural applications.

By End Use

OEMs held the largest share in 2025 due to large-scale integration of PP compounds during vehicle manufacturing. The aftermarket segment is growing with rising replacement and customization demand.

Regional Analysis

North America

North America accounted for 31.84% of the market in 2025, driven by strong automotive manufacturing and demand for lightweight vehicle components in the United States.

Europe

Europe held 27.52% share in 2025, supported by strict emission regulations and advanced automotive engineering capabilities, with Germany leading the region.

Asia Pacific

Asia Pacific accounted for 32.11% share in 2025 and is expected to grow at the fastest CAGR due to high vehicle production in China, India, and Japan.

Middle East & Africa

The region held 4.18% share in 2025, driven by rising automotive imports and infrastructure development in UAE and Saudi Arabia.

Latin America

Latin America accounted for 4.35% share in 2025 with Brazil leading due to expanding automotive manufacturing and rising vehicle demand.

Competitive Landscape

The pp compound for automotive market is moderately consolidated with global chemical and material manufacturers focusing on innovation, recyclability, and high-performance polymer solutions. Companies are investing in R&D to develop advanced PP compounds with improved heat resistance and mechanical strength.

Key Players Analysis

1. LyondellBasell Industries – Leading global supplier of polypropylene compounds for automotive applications.

2. Borealis AG – Major producer of advanced PP compounds with strong focus on sustainable materials.

3. SABIC – Offers high-performance PP compounds widely used in automotive interior and exterior components.

4. ExxonMobil Chemical – Provides specialty polymer solutions for automotive lightweighting.

5. Sumitomo Chemical – Focuses on advanced polypropylene materials for vehicle manufacturing.

6. INEOS Group – Known for durable PP compound solutions used in automotive engineering.

7. RTP Company – Specializes in engineered thermoplastic compounds for automotive use.

8. Celanese Corporation – Offers high-performance materials for structural and interior automotive parts.

9. LG Chem – Provides innovative polymer materials supporting EV and lightweight vehicle applications.

10. Mitsui Chemicals – Focuses on advanced polypropylene compounds for global automotive OEMs.