Electric Vehicle E-Axle Market Overview

The electric vehicle e-axle market is witnessing rapid expansion due to the global transition toward electrified mobility and the rising demand for compact and efficient drivetrain solutions. An e-axle integrates key powertrain components such as the electric motor, transmission, and power electronics into a single unit, improving efficiency, reducing weight, and optimizing vehicle space utilization. According to Redline Pulse, increasing EV adoption and advancements in integrated drivetrain technologies are driving strong market growth.

Get Your Sample Report Here: https://www.redlinepulse.com/report/electric-vehicle-e-axle-market/request-sample

Electric Vehicle E-Axle Market Size

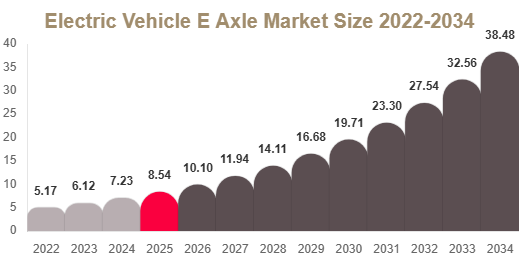

Market Size in 2025: USD 8.6 Billion

Market Size in 2026: USD 10.1 Billion

CAGR (2025–2034): 18.2%

Market Size in 2034: USD 40.7 Billion

The market’s strong growth reflects accelerating electrification across passenger and commercial vehicles, supported by regulatory pressure, technological advancements, and increasing focus on energy efficiency.

Key Market Insights

North America dominated with 34.26% share in 2025.

Asia Pacific is expected to be the fastest-growing region with a CAGR of 20.1%.

Integrated e-axle systems held 46.52% share in 2025.

Battery electric vehicles accounted for 61.38% share in 2025.

Passenger electric vehicles dominated with 58.74% share in 2025.

OEM segment led the market with 72.15% share in 2025.

The U.S. market was valued at USD 2.94 billion in 2025 and reached USD 3.48 billion in 2026.

Market Trends

Integration of High-Voltage Modular Drivetrain Systems

A key trend is the adoption of high-voltage modular e-axle systems that combine motor, inverter, and transmission into a single compact module. The increasing use of 800V architectures is improving energy efficiency and enabling faster charging capabilities. This trend is particularly strong in premium electric vehicles and high-performance models.

Shift Toward Scalable EV Platforms

Automakers are increasingly developing scalable EV platforms that support multiple vehicle models using standardized e-axle systems. This approach reduces production complexity and costs while improving manufacturing flexibility. It also enables global vehicle platforms that can be adapted across different markets.

Market Drivers

Rising Electrification of the Automotive Industry

The global shift toward electric mobility is a major driver of the e-axle market. Governments are enforcing strict emission regulations and promoting EV adoption through incentives. E-axles provide a highly efficient solution by integrating multiple drivetrain components into a single system, reducing energy losses and improving performance.

Demand for Lightweight and Efficient Powertrains

Reducing vehicle weight is critical for improving EV range and efficiency. E-axles eliminate multiple mechanical components, resulting in lighter and more efficient powertrains. Automakers are increasingly investing in advanced materials and compact designs to enhance performance.

Market Restraints

High Development and Production Costs

E-axle systems require complex integration of motors, electronics, and transmission units, leading to high manufacturing costs. This limits adoption in entry-level vehicles and price-sensitive markets. Smaller manufacturers also face challenges due to limited R&D and production capabilities.

Cost barriers are particularly evident in emerging economies, where affordability remains a key factor in vehicle purchasing decisions. As a result, advanced e-axle systems are often restricted to premium EV segments, slowing wider market penetration.

Market Opportunities

Expansion of Electric Commercial Vehicles

Electric commercial vehicles such as trucks, buses, and delivery vans present significant growth opportunities. E-axles are well-suited for these applications due to their high torque output and durability. Increasing demand for logistics electrification is expected to accelerate adoption.

Advancements in Silicon Carbide Power Electronics

The adoption of silicon carbide and other advanced semiconductor materials is improving efficiency and thermal performance in e-axle systems. These innovations reduce energy loss and enhance driving range, making EVs more competitive with traditional vehicles.

Segmental Analysis

By Configuration

Integrated E-Axle Systems

Integrated systems dominated the market with 46.52% share in 2024. These systems combine motor, inverter, and transmission into a single unit, improving efficiency and reducing space requirements. They are widely preferred by automakers for modern EV platforms.

Distributed E-Axle Systems

Distributed systems are expected to grow at a CAGR of 19.4%. These systems offer flexibility in multi-motor EV architectures and are used in high-performance vehicles requiring independent axle control.

By Propulsion Type

Battery Electric Vehicles

Battery electric vehicles held 61.38% share in 2024. Their fully electric drivetrain architecture makes e-axle integration essential, supported by government incentives and expanding charging infrastructure.

Hybrid Electric Vehicles

Hybrid vehicles are expected to grow at a CAGR of 16.8%, driven by transitional adoption in regions where full electrification is still developing.

By Vehicle Type

Passenger Vehicles

Passenger vehicles dominated with 58.74% share in 2024 due to rising consumer demand for electric cars and increased focus on energy efficiency.

Commercial Vehicles

Commercial vehicles are projected to grow at a CAGR of 20.5%, driven by fleet electrification and logistics modernization.

By Distribution Channel

OEM

The OEM segment dominated with 72.15% share in 2025 as manufacturers integrate e-axles during vehicle production to optimize performance and efficiency.

Aftermarket

The aftermarket segment is gradually expanding as EV servicing and component replacement demand increases.

Regional Analysis

North America

North America held 34.26% share in 2025 and is projected to grow at a CAGR of 17.4%. Strong EV adoption and government incentives are key growth drivers. The U.S. leads due to strong EV manufacturing capabilities and innovation in drivetrain technology.

Europe

Europe accounted for 29.18% share in 2025 and is expected to grow at a CAGR of 18.6%. Strict emission regulations and rapid EV adoption among premium automakers drive growth. Germany leads due to strong automotive engineering capabilities.

Asia Pacific

Asia Pacific held 28.42% share in 2025 and is projected to grow at the fastest CAGR of 20.1%. China dominates due to large-scale EV production and government subsidies supporting electrification.

Middle East & Africa

The region accounted for 4.12% share in 2025 and is expected to grow at a CAGR of 15.3%. The UAE leads due to early adoption of electric mobility initiatives.

Latin America

Latin America held 4.02% share in 2025 and is expected to grow at a CAGR of 16.1%. Brazil dominates due to increasing investment in EV infrastructure and automotive expansion.

Competitive Landscape

The electric vehicle e-axle market is highly competitive, with major players focusing on innovation, partnerships, and expansion of production capabilities. Companies are investing heavily in R&D to improve system efficiency, reduce cost, and enhance performance. Bosch, ZF Friedrichshafen AG, and BorgWarner are among the key leaders driving technological advancements in integrated drivetrain systems.

Top Players Analysis

- Robert Bosch GmbH

A leading player focusing on integrated e-axle systems and large-scale EV drivetrain production expansion to meet growing global demand. - ZF Friedrichshafen AG

Specializes in advanced electrified drivetrains and integrated mobility solutions with strong R&D capabilities. - BorgWarner Inc.

Focuses on high-efficiency electric propulsion systems and expanding its EV product portfolio globally. - Magna International Inc.

Provides integrated automotive systems with strong capabilities in electrified powertrain development. - GKN Automotive

A key innovator in e-axle systems with strong focus on all-wheel-drive electric solutions. - Continental AG

Develops intelligent mobility and drivetrain technologies with emphasis on system integration. - Schaeffler AG

Focuses on high-performance e-mobility solutions and integrated drivetrain systems. - Dana Incorporated

Provides electrified drivetrain systems for passenger and commercial vehicles. - Hitachi Astemo Ltd.

Specializes in advanced automotive technologies including electric powertrain systems. - Nidec Corporation

A major supplier of electric motors and integrated e-axle components. - Hyundai Mobis

Develops next-generation EV platforms and integrated drivetrain technologies. - Valeo SA

Focuses on electrification solutions and advanced mobility systems. - AVL List GmbH

Provides engineering solutions for electrified powertrain development. - Mitsubishi Electric Corporation

Develops power electronics and motor systems for electric mobility. - Dana TM4 Inc.

Specializes in electric propulsion systems and integrated e-drive technologies.

Conclusion

The electric vehicle e-axle market is set for exponential growth driven by rapid EV adoption, technological advancements, and regulatory support for zero-emission mobility. While high costs and engineering complexity remain challenges, innovations in materials, power electronics, and scalable platforms are expected to accelerate adoption across global automotive markets.

Get More Details: https://www.redlinepulse.com/report/electric-vehicle-e-axle-market

Buy Now: https://www.redlinepulse.com/report/electric-vehicle-e-axle-market/buy-now