Electric Vehicle Test Equipment Market Overview

The electric vehicle test equipment market is expanding rapidly as automotive electrification accelerates across major global economies. EV manufacturers are increasingly relying on advanced testing systems to validate safety, performance, battery efficiency, and drivetrain reliability. According to Redline Pulse, the growing complexity of electric vehicle architectures and rising regulatory standards are significantly driving demand for sophisticated testing solutions.

Get Your Sample Report Here: https://www.redlinepulse.com/report/electric-vehicle-test-equipment-market/request-sample

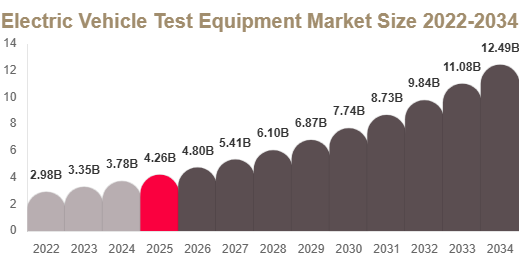

Electric Vehicle Test Equipment Market Size

Market Size in 2025: USD 4.2 Billion

Market Size in 2026: USD 4.8 Billion

CAGR (2025–2034): 12.7%

Market Size in 2034: USD 12.6 Billion

The market is experiencing strong growth due to increasing EV production, stricter safety regulations, and rising demand for high-precision validation systems for batteries and powertrains.

Key Market Insights

North America dominated with 34.62% share in 2025.

Asia Pacific is expected to be the fastest-growing region at a CAGR of 14.1%.

Battery test systems held 38.45% share in 2025.

Powertrain testing accounted for 41.27% share in 2025.

Hardware-based systems dominated with 57.18% share in 2025.

OEM segment led with 64.33% share in 2025.

The U.S. market was valued at USD 1.46 billion in 2025 and reached USD 1.68 billion in 2026.

Market Trends

Expansion of AI-Driven and Automated Testing Systems

A major trend is the adoption of artificial intelligence and automation in EV test equipment. These systems improve accuracy, reduce manual intervention, and accelerate validation processes. AI-enabled platforms analyze large datasets from battery and drivetrain testing to detect faults and optimize performance. This is increasingly important as EV systems become more complex and software-driven.

Growth of Digital Twin and Virtual Simulation Technologies

Digital twin technology is transforming EV testing by enabling virtual simulation of real-world conditions. Engineers can analyze battery behavior, thermal performance, and energy efficiency in a controlled digital environment. This reduces physical testing costs and improves development speed, especially for next-generation EV architectures.

Market Drivers

Rapid Expansion of Electric Vehicle Production

The surge in EV production is a key driver of the test equipment market. Automakers must rigorously test batteries, motors, and electronic systems to meet safety and performance standards. This has increased demand for high-voltage testing systems capable of handling complex EV architectures.

Stringent Regulatory and Safety Requirements

Governments and regulatory bodies are enforcing strict safety standards for EV components. Manufacturers must comply with global certification requirements for battery safety, crash testing, and energy efficiency. This is driving demand for advanced testing systems capable of simulating extreme operating conditions.

Market Restraints

High Capital Investment Requirements

One of the major restraints is the high cost of EV test equipment. Advanced systems require significant investment in hardware, software, maintenance, and calibration. This limits adoption among small and mid-sized manufacturers.

Cost barriers are especially strong in emerging markets, where companies often rely on outsourced testing instead of building in-house facilities. Continuous upgrades required for evolving EV technologies also increase long-term operational costs, slowing adoption in cost-sensitive regions.

Market Opportunities

Advancements in Next-Generation Battery Testing

The rise of advanced battery technologies such as solid-state and high-energy lithium-ion batteries is creating strong demand for sophisticated testing solutions. These batteries require specialized validation under extreme temperature, load, and lifecycle conditions, opening new opportunities for test equipment manufacturers.

Expansion of EV Charging Infrastructure Testing

The global rollout of EV charging infrastructure is creating additional demand for testing systems. Fast-charging stations, high-voltage connectors, and grid integration systems require validation for efficiency, durability, and safety under high-load conditions.

Segmental Analysis

By Equipment Type

Battery Test Systems

Battery test systems dominated with 38.45% share in 2024. These systems evaluate energy storage performance, charging efficiency, and thermal stability, making them essential for EV safety and development.

Powertrain Test Systems

Powertrain testing is expected to grow at a CAGR of 13.6%. Increasing complexity of EV drivetrains is driving demand for advanced validation tools that measure torque, efficiency, and durability.

By Application

Powertrain Testing

Powertrain testing dominated with 41.27% share in 2024 due to its critical role in vehicle performance and efficiency validation.

Battery Testing

Battery testing is expected to grow at a CAGR of 14.2%, driven by innovation in battery chemistry and increasing safety requirements.

By End Use

OEMs

OEMs held 64.33% share in 2024 as automakers invest heavily in in-house testing infrastructure to ensure compliance and accelerate development cycles.

Testing Laboratories

Testing laboratories are expected to grow at a CAGR of 13.1%, as smaller manufacturers increasingly outsource testing due to high equipment costs.

Regional Analysis

North America

North America accounted for 34.62% share in 2025 and is projected to grow at a CAGR of 11.8%. Strong EV adoption and advanced R&D capabilities are key drivers. The U.S. leads the region due to strong presence of EV manufacturers and technology companies investing in testing infrastructure.

Europe

Europe held 28.41% share in 2025 and is expected to grow at a CAGR of 12.3%. Strict environmental regulations and strong EV adoption drive demand. Germany dominates due to its advanced automotive engineering ecosystem.

Asia Pacific

Asia Pacific accounted for 27.18% share in 2025 and is expected to grow at the fastest CAGR of 14.1%. China leads due to large-scale EV production and strong government support for testing infrastructure.

Middle East & Africa

The region held 5.12% share in 2025 and is expected to grow at a CAGR of 10.2%. The UAE leads due to smart mobility initiatives and investment in sustainable transport systems.

Latin America

Latin America accounted for 4.67% share in 2025 and is expected to grow at a CAGR of 10.9%. Brazil dominates due to automotive sector modernization and foreign investment in EV production.

Competitive Landscape

The market is moderately consolidated, with key players focusing on innovation, automation, and AI-driven testing platforms. Companies are investing heavily in R&D to develop integrated EV validation systems. Keysight Technologies is a leading player, offering advanced high-voltage and battery testing solutions for EV applications.

Top Players Analysis

- Keysight Technologies

A leading provider of EV testing solutions, focusing on battery validation, power electronics testing, and high-voltage simulation systems. - National Instruments Corporation

Offers advanced automated test systems and modular platforms for EV component validation. - Siemens AG

Provides integrated industrial testing and simulation solutions for electric mobility applications. - Horiba Ltd.

Specializes in automotive testing systems, including battery and emission validation technologies. - AVL List GmbH

Focuses on powertrain development and advanced EV testing and simulation solutions. - Rohde & Schwarz

Provides high-precision measurement and testing equipment for electronic and EV systems. - Chroma ATE Inc.

Specializes in power electronics and battery testing equipment for EV applications. - Bosch Rexroth AG

Develops industrial automation and testing solutions for automotive electrification. - Teradyne Inc.

Focuses on automated test equipment for complex electronic systems. - ABB Ltd.

Provides electrification and automation solutions including EV testing infrastructure. - Emerson Electric Co.

Offers advanced testing and measurement systems for industrial and automotive applications. - Dürr Group

Specializes in automotive manufacturing and testing technologies. - Instron (Illinois Tool Works Inc.)

Provides material testing systems used in EV component validation. - Kistler Group

Focuses on sensor-based measurement and testing solutions for automotive systems. - Dewesoft d.o.o.

Offers data acquisition and testing systems for EV performance validation.

Conclusion

The electric vehicle test equipment market is set for strong and sustained growth, driven by rapid EV adoption, strict regulatory standards, and advancements in testing technologies. While high costs remain a challenge, innovation in AI-driven systems, digital twins, and battery testing technologies is expected to significantly enhance market expansion over the forecast period.

Get More Details: https://www.redlinepulse.com/report/electric-vehicle-test-equipment-market

Buy Now: https://www.redlinepulse.com/report/electric-vehicle-test-equipment-market/buy-now