Automotive All Wheel Drive Market Size

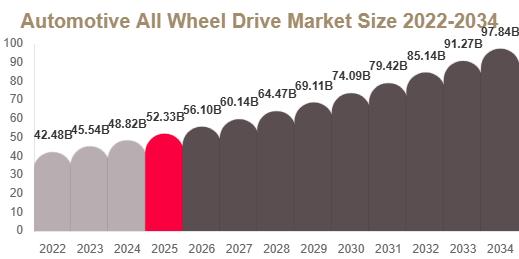

The automotive all wheel drive market size is estimated at USD 52.4 billion in 2025 and is projected to reach USD 56.1 billion in 2026. By 2034, the market is expected to attain approximately USD 98.7 billion, registering a CAGR of 7.2% (2025–2034).

The global automotive all wheel drive market is witnessing steady expansion as demand increases for improved vehicle stability, traction control, and performance across varied road and weather conditions.

Get Your Sample Report Here: https://www.redlinepulse.com/report/automotive-all-wheel-drive-market/request-sample

Buy Now: https://www.redlinepulse.com/report/automotive-all-wheel-drive-market/buy-now

Market Overview

The automotive all wheel drive market is expanding due to rising consumer preference for SUVs and crossovers, increasing integration of advanced drivetrain technologies, and growing focus on safety and driving comfort. Automakers are increasingly deploying AWD systems to enhance vehicle performance in diverse driving conditions while meeting evolving consumer expectations for premium mobility experiences.

Market Trends

Shift toward intelligent and on-demand AWD systems

A major trend is the growing adoption of on-demand AWD systems that activate only when required. These systems use sensors and electronic control units to distribute torque efficiently between axles, improving fuel efficiency while maintaining traction and stability. This technology is increasingly being integrated into mid-range passenger vehicles and SUVs.

Electrification of AWD systems in EV platforms

Another key trend is the rapid integration of AWD systems in electric vehicles. Electric AWD systems, typically based on dual-motor configurations, provide precise torque control, better acceleration, and improved stability. This architecture eliminates many mechanical components, making EV AWD systems more efficient and compact.

Market Drivers

Rising demand for SUVs and crossovers

The growing global preference for SUVs and crossover vehicles is a major driver of the AWD market. These vehicles often require AWD systems to deliver better traction, off-road capability, and enhanced safety. Automakers are expanding SUV lineups across all regions, increasing AWD adoption significantly.

Increasing focus on vehicle safety and performance

Consumers and regulators are increasingly prioritizing vehicle safety and performance. AWD systems improve grip and stability on slippery and uneven surfaces, reducing accident risks. This makes them highly desirable in regions with extreme weather conditions or diverse terrain.

Market Restraints

High system complexity and increased vehicle cost

One of the key restraints is the higher cost and mechanical complexity of AWD systems. Components such as transfer cases, differentials, and driveshafts increase production costs and vehicle weight. This reduces fuel efficiency in conventional vehicles and limits AWD penetration in entry-level segments.

Market Opportunities

Expansion of AWD systems in electric vehicles

Electric vehicles present a major opportunity for AWD adoption. EV platforms enable dual or multi-motor configurations, allowing precise torque distribution without complex mechanical linkages. This enhances performance and makes AWD integration simpler and more efficient.

Development of lightweight and efficient drivetrain systems

Manufacturers are focusing on lightweight AWD architectures using advanced materials and optimized driveline designs. These innovations improve fuel efficiency and extend EV driving range, making AWD systems more suitable for next-generation mobility solutions.

Segmental Analysis

By AWD System Type

On-demand AWD systems dominated the market with a 48.21% share in 2024 due to their efficiency and adaptability. These systems engage only when needed, reducing energy loss.

Electric AWD systems are expected to grow at the fastest CAGR of 8.9%, driven by rising EV adoption and dual-motor configurations that enhance performance and efficiency.

By Vehicle Type

SUVs dominated with a 62.44% share in 2024 due to strong global demand for versatile and high-performance vehicles.

Electric vehicles are expected to grow at the fastest CAGR of 9.2%, supported by increasing electrification and AWD integration in EV platforms.

By Drive Type

Passenger vehicles held 71.18% share in 2024 due to high global demand for personal mobility.

Commercial vehicles are expected to grow at a CAGR of 6.8%, driven by logistics expansion and fleet modernization.

Regional Analysis

North America

North America accounted for 34.56% share in 2025 and is projected to grow at a CAGR of 7.4%. The region benefits from strong SUV penetration and high demand for premium vehicles.

The United States dominates due to widespread adoption of AWD-equipped SUVs and pickup trucks, along with strong consumer preference for all-weather driving capability.

Europe

Europe held 28.14% share in 2025 and is expected to grow at a CAGR of 7.1%. Growth is driven by strict safety regulations and strong demand for luxury vehicles.

Germany leads the region due to advanced automotive engineering and high adoption of AWD in premium vehicles.

Asia Pacific

Asia Pacific accounted for 30.22% share in 2025 and is projected to grow at the fastest CAGR of 8.3%. Rapid urbanization and rising vehicle production support strong growth.

China dominates due to large-scale automotive manufacturing and increasing SUV demand in urban markets.

Middle East & Africa

The region held 4.1% share in 2025 and is expected to grow at a CAGR of 6.5%. Demand is driven by off-road and high-performance SUVs.

Saudi Arabia leads due to terrain conditions favoring AWD-equipped vehicles.

Latin America

Latin America accounted for 3.0% share in 2025 and is projected to grow at a CAGR of 6.2%. Growth is driven by increasing vehicle imports and SUV demand.

Brazil dominates due to rising vehicle ownership and preference for rugged vehicles.

Competitive Landscape

The automotive all wheel drive market is moderately consolidated, with major players focusing on electrification and advanced drivetrain technologies. Companies are investing in lightweight AWD systems, torque vectoring technologies, and EV-compatible architectures.

ZF Friedrichshafen AG is a leading player, known for its advanced AWD and torque vectoring systems. The company has expanded its electric AWD portfolio for next-generation EV platforms.

Other key players include BorgWarner Inc., GKN Automotive, Magna International, Aisin Corporation, and Dana Incorporated, all focusing on innovation and electrified drivetrain solutions.

Key Players List

- ZF Friedrichshafen AG

- BorgWarner Inc.

- GKN Automotive

- Magna International

- Aisin Corporation

- Dana Incorporated

- American Axle & Manufacturing

- Schaeffler AG

- JTEKT Corporation

- Hyundai WIA

- Showa Corporation

- Neapco Holdings

- Meritor Inc.

- ZF TRW

- Ricardo plc