Electric Vehicle Reducer Market Overview

The electric vehicle reducer market is a critical segment of the EV drivetrain ecosystem, responsible for reducing motor speed while increasing torque delivered to the wheels. As electric mobility expands globally, reducers are becoming increasingly important for improving efficiency, performance, and energy optimization in EV powertrains. According to Redline Pulse, the growing shift toward compact and high-efficiency drivetrain systems is significantly accelerating demand for advanced EV reducers.

Get Your Sample Report Here: https://www.redlinepulse.com/report/electric-vehicle-reducer-market/request-sample

Electric Vehicle Reducer Market Size

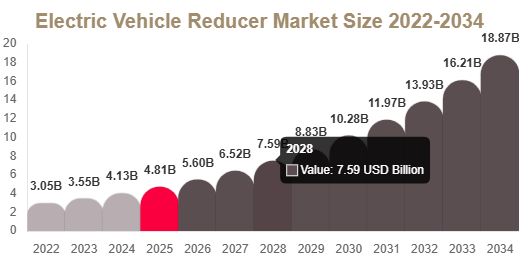

Market Size in 2025: USD 4.8 Billion

Market Size in 2026: USD 5.6 Billion

CAGR (2025–2034): 16.4%

Market Size in 2034: USD 18.9 Billion

The market is expanding rapidly due to rising EV adoption, advancements in drivetrain technologies, and increasing demand for lightweight and high-torque power transmission systems.

Key Market Insights

Asia Pacific dominated the market with 45.32% share in 2025.

Europe is expected to be the fastest-growing region with a CAGR of 17.2%.

Single-stage reducers held 61.48% share in 2025.

Passenger EVs dominated with 58.91% share in 2025.

Battery electric vehicles (BEVs) accounted for 63.27% share in 2025.

OEM segment led the market with 72.64% share in 2025.

The U.S. market was valued at USD 1.6 billion in 2025 and reached USD 1.9 billion in 2026.

Market Trends

Shift Toward Integrated E-Axle Reducer Systems

A major trend in the EV reducer market is the adoption of integrated e-axle systems that combine motor, reducer, and power electronics into a single compact unit. This improves energy efficiency, reduces weight, and simplifies vehicle architecture. These systems are widely used in compact and mid-range EVs where space optimization and cost efficiency are critical.

Rising Demand for Low-Noise and High-Efficiency Reducers

Another key trend is the focus on reducing noise, vibration, and energy loss in EV reducers. Manufacturers are improving gear design, lubrication systems, and material quality to ensure smoother operation and higher efficiency, which directly contributes to extended vehicle range and improved driving comfort.

Market Drivers

Rapid Expansion of Electric Vehicle Production

The global increase in EV production is a primary growth driver. Government incentives, emission regulations, and infrastructure development are pushing automakers to scale EV manufacturing. This directly increases demand for efficient reducers that optimize torque transfer in electric drivetrains.

Technological Advancements in EV Drivetrain Systems

Continuous innovation in drivetrain architecture is another key driver. Automakers are shifting toward single-speed and dual-speed reducers designed specifically for EVs, improving acceleration, efficiency, and overall performance. Advances in materials and simulation-based design are also enhancing durability and reliability.

Market Restraints

High Precision Manufacturing Complexity

A major restraint is the high precision required in reducer manufacturing. Tight tolerances and advanced machining processes increase production costs and limit scalability. The use of high-grade materials and strict quality requirements further add to manufacturing expenses.

Smaller manufacturers face barriers due to high capital requirements and technical complexity, which restricts market entry and expansion.

Market Opportunities

Growth of High-Performance Electric Vehicles

The increasing demand for high-performance EVs creates strong opportunities for advanced reducer systems. These vehicles require multi-speed reducers capable of handling higher torque and speed variations, driving innovation in compact and high-efficiency designs.

Expansion of Commercial Electric Mobility

The rise of electric buses, trucks, and logistics fleets is creating significant demand for durable reducers. These vehicles require robust systems that can handle heavy loads and long operational cycles, making this segment a key long-term growth opportunity.

Segmental Analysis

By Reducer Type

Single-Stage Reducers

Single-stage reducers dominated with 61.48% share in 2024 due to their simplicity, high efficiency, and cost-effectiveness. They are widely used in passenger EVs and standard electric platforms.

Multi-Stage Reducers

Multi-stage reducers are expected to grow at a CAGR of 17.8%, driven by demand for high-performance EVs requiring advanced torque control and efficiency optimization.

By Vehicle Type

Passenger EVs

Passenger EVs held 58.91% share in 2024 due to strong global adoption and increasing consumer preference for electric mobility.

Commercial EVs

Commercial EVs are expected to grow at a CAGR of 18.2% due to expanding electric logistics fleets and public transport electrification.

By Propulsion Type

Battery Electric Vehicles (BEVs)

BEVs dominated with 63.27% share in 2024 as global markets shift toward full electrification.

Hybrid Electric Vehicles (HEVs)

HEVs continue steady adoption in transitional markets where full electrification is still developing.

Regional Analysis

North America

North America accounted for 21.38% share in 2025 and is expected to grow at a CAGR of 15.8%. Growth is driven by EV adoption and increasing production of electric SUVs and pickup trucks. The U.S. leads due to strong R&D and manufacturing capabilities.

Europe

Europe held 27.44% share in 2025 and is projected to grow at a CAGR of 17.2%. Strict emission regulations and strong EV adoption targets are key drivers. Germany leads due to advanced automotive engineering and premium EV production.

Asia Pacific

Asia Pacific dominated with 45.32% share in 2025 and is expected to grow at a CAGR of 16.9%. China leads due to large-scale EV production and strong government support for electrification.

Middle East & Africa

The region held 3.7% share in 2025 and is expected to grow at a CAGR of 14.6%. Growth is driven by emerging EV infrastructure and smart mobility initiatives, particularly in the UAE.

Latin America

Latin America accounted for 2.1% share in 2025 and is expected to grow at a CAGR of 15.1%. Brazil leads due to emerging EV assembly programs and government incentives for clean mobility.

Competitive Landscape

The EV reducer market is moderately consolidated, with leading companies focusing on high-efficiency designs, compact integration, and advanced drivetrain technologies. ZF Friedrichshafen AG is a key market leader with strong expertise in e-drive reducer systems and ongoing expansion in e-mobility production capacity.

Top Players Analysis

- ZF Friedrichshafen AG

A global leader in EV drivetrain systems, specializing in integrated reducer and e-axle technologies for next-generation electric mobility platforms. - BorgWarner Inc.

Focuses on high-efficiency drivetrain and e-mobility solutions with strong innovation in EV reducers. - GKN Automotive

Specializes in advanced e-drive systems and integrated powertrain solutions. - Robert Bosch GmbH

Provides cutting-edge automotive technologies including EV drivetrain and reducer systems. - Aisin Corporation

Offers high-performance transmission and reducer systems for electric mobility. - Schaeffler AG

Focuses on precision engineering solutions for EV drivetrains. - Magna International

Develops integrated EV powertrain systems and drivetrain components. - Hyundai Transys

Specializes in electrified drivetrain and transmission technologies. - JTEKT Corporation

Provides advanced steering and drivetrain solutions for EV applications. - Dana Incorporated

Focuses on electrified propulsion systems and drivetrain technologies. - AVL List GmbH

Offers simulation and engineering solutions for EV powertrain development. - Nidec Corporation

Specializes in electric motor and drivetrain component technologies. - Ricardo PLC

Provides engineering and consulting services for EV drivetrain systems. - Valeo

Focuses on innovative electrification and drivetrain solutions. - Hitachi Astemo

Develops advanced mobility systems including EV reducers and e-axle components.

Conclusion

The electric vehicle reducer market is set for rapid expansion driven by rising EV adoption, technological advancements in drivetrain systems, and increasing demand for high-efficiency torque transmission solutions. While precision manufacturing complexity remains a challenge, innovations in integrated e-axle systems and commercial EV applications are expected to unlock strong growth opportunities over the forecast period.

Get More Details: https://www.redlinepulse.com/report/electric-vehicle-reducer-market

Buy Now: https://www.redlinepulse.com/report/electric-vehicle-reducer-market/buy-now