Automotive Brake Shims Market Report

Get Your Sample Report Here: https://www.redlinepulse.com/report/automotive-brake-shims-market/request-sample

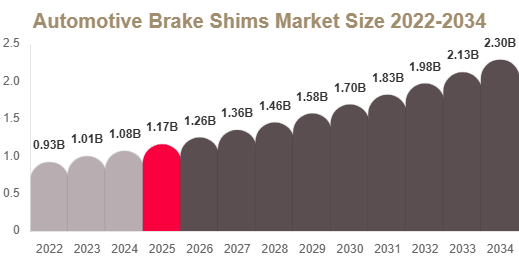

Automotive Brake Shims Market Size

The Automotive Brake Shims market size was valued at USD 1.18 billion in 2025 and is projected to reach USD 1.26 billion in 2026. By 2034, the market is expected to attain approximately USD 2.34 billion, expanding at a CAGR of 7.8% during 2025–2034.

The Automotive Brake Shims Market is witnessing steady expansion driven by rising demand for NVH (noise, vibration, and harshness) reduction solutions, increasing vehicle production, and growing adoption of advanced braking systems across global automotive platforms.

Market Overview

Automotive brake shims are thin damping components placed between brake pads and calipers to reduce vibration and brake noise. They are increasingly becoming standard components in modern braking systems, especially in passenger vehicles and electric vehicles where noise reduction is a critical performance factor. OEM integration and aftermarket replacement demand are both contributing to market stability and growth.

Market Drivers

Rising Demand for NVH Reduction in Vehicles

One of the strongest drivers is increasing consumer expectation for quieter and smoother braking performance. Automotive manufacturers are focusing on NVH reduction to improve driving comfort, particularly in premium vehicles and EVs. Brake shims play a critical role in eliminating brake squeal and vibration, making them essential in modern braking systems.

Growth in Global Vehicle Production

Rising vehicle production, especially in emerging economies, is directly supporting demand for brake system components. Passenger cars and light commercial vehicles are the largest contributors. Every new vehicle requires brake assemblies, ensuring consistent OEM demand for brake shims.

Expansion of Electric Vehicles

Electric vehicles are accelerating demand for brake shims because reduced engine noise makes brake sound more noticeable. This increases the need for advanced damping solutions, particularly multi-layer and rubber-coated shims designed for EV platforms.

Strict Noise and Safety Regulations

Regulatory standards in Europe and North America are pushing automakers to adopt low-noise braking systems. These regulations are encouraging OEMs to integrate advanced brake shim technologies across all vehicle categories.

Market Challenges

Price Pressure from Low-Cost Manufacturers

The market faces strong competition from low-cost aftermarket suppliers, especially in price-sensitive regions. This creates pressure on established manufacturers to balance cost efficiency with performance quality.

Raw Material Cost Fluctuations

Steel, rubber, and adhesive materials used in brake shims are subject to price volatility. This affects production costs and can impact profit margins for manufacturers.

Performance Variation in Aftermarket Products

Inconsistent quality in aftermarket brake shims can affect reliability and safety perceptions, creating challenges for brand trust and long-term adoption.

Market Trends

Adoption of Multi-Layer Steel Shim Technology

Multi-layer steel (MLS) shims are increasingly used due to their superior vibration damping and durability. These shims are widely integrated into OEM braking systems for high-performance and EV applications.

Growth of EV-Specific Brake Shim Designs

EV-specific brake shims are being developed to address unique NVH challenges in electric vehicles. These solutions focus on thermal stability and noise suppression under regenerative braking conditions.

Lightweight and Corrosion-Resistant Materials

Manufacturers are increasingly focusing on lightweight and corrosion-resistant coatings to improve product lifespan and performance under harsh conditions.

Segment Analysis

By Material Type

Multi-layer steel shims dominated the market in 2025 with a share of 46.2% due to their superior durability and vibration control. Their strong compatibility with modern braking systems makes them widely adopted in OEM applications.

Rubber-coated shims are gaining traction due to superior noise absorption and cost-effectiveness, particularly in passenger vehicle applications and aftermarket replacement segments.

By Vehicle Type

Passenger vehicles dominated with a share of 58.4% in 2025, driven by high global vehicle ownership and demand for comfort-oriented braking systems. OEM integration across mass-market vehicles further supports dominance.

Electric vehicles are expected to be the fastest-growing segment due to increasing focus on NVH reduction in silent powertrains.

By Sales Channel

OEM segment dominated the market with a share of 61.7% in 2025 due to direct integration of brake shims during vehicle manufacturing.

Aftermarket segment is expanding steadily due to frequent brake pad replacement cycles and increasing vehicle parc globally.

Regional Analysis

North America

North America held 33.9% share in 2025, driven by strong automotive manufacturing and high adoption of advanced braking technologies. The United States leads due to its large vehicle fleet and growing EV penetration.

Europe

Europe accounted for 28.4% share in 2025, supported by strict noise regulations and strong automotive engineering capabilities. Germany leads due to its premium vehicle manufacturing base.

Asia Pacific

Asia Pacific dominated with 31.6% share in 2025 and is the fastest-growing region. China leads due to large-scale automotive production and rising demand for cost-efficient NVH solutions.

Middle East & Africa

The region shows steady growth supported by rising vehicle imports and increasing demand for luxury vehicles with improved braking comfort.

Latin America

Latin America is growing steadily, led by Brazil, driven by expansion of automotive aftermarket services and increasing vehicle ownership.

Competitive Landscape

The automotive brake shims market is moderately consolidated with global players focusing on product innovation, material advancement, and EV-compatible solutions. Manufacturers are increasingly investing in multi-layer damping technologies and corrosion-resistant materials to enhance performance and durability.

Key Players Analysis

- Nisshinbo Holdings Inc.

A leading global supplier of brake friction materials, Nisshinbo focuses on advanced NVH solutions and strong OEM partnerships. The company emphasizes multi-layer shim technologies designed for modern braking systems and EV applications. - Tenneco Inc.

Tenneco is a major player offering integrated braking solutions through its global aftermarket and OEM channels. The company focuses on performance-enhancing brake components with strong durability standards. - Robert Bosch GmbH

Bosch plays a significant role in automotive braking innovation with advanced engineering capabilities. Its focus includes precision-engineered brake components designed for high-performance and electric vehicles. - Akebono Brake Industry Co., Ltd.

Akebono specializes in brake systems with strong expertise in NVH reduction technologies. The company supplies OEM-grade brake shims for global automotive manufacturers. - Brembo S.p.A.

Brembo is known for high-performance braking systems and premium vehicle applications. It focuses on advanced material technologies and precision engineering for performance vehicles. - Continental AG

Continental provides integrated automotive solutions including brake system components. The company emphasizes innovation in lightweight and efficient braking technologies. - Hitachi Astemo Ltd.

Hitachi Astemo focuses on advanced mobility solutions, including brake system technologies optimized for electric and hybrid vehicles. - ADVICS Co., Ltd.

ADVICS specializes in braking systems with strong OEM relationships. The company focuses on safety, durability, and high-performance brake technologies. - Mando Corporation

Mando supplies braking systems globally with a focus on cost-effective and reliable solutions for passenger and commercial vehicles. - Knorr-Bremse AG

Knorr-Bremse is a leader in commercial vehicle braking systems, focusing on heavy-duty applications with advanced safety and durability standards.