Automotive Anti Lock Braking System Market Size

The automotive anti lock braking system market is positioned for steady expansion as vehicle safety standards tighten and braking control becomes a core purchasing factor across passenger and commercial vehicle categories. Anti lock braking systems (ABS) prevent wheel lock-up during emergency braking, improving steering control and road safety.

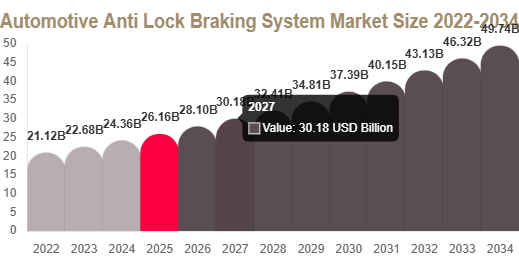

The market was valued at USD 26.4 billion in 2025 and is estimated to reach USD 28.1 billion in 2026. By 2034, the market is projected to attain USD 49.7 billion, registering a CAGR of 7.4% from 2025 to 2034.

Get Your Sample Report Here: https://www.redlinepulse.com/report/automotive-anti-lock-braking-system-market/request-sample

Market Overview

The automotive anti lock braking system market is evolving from a regulatory compliance feature into an integrated intelligent braking ecosystem. ABS is now combined with electronic stability control, traction systems, and advanced driver assistance technologies, strengthening overall vehicle safety architecture.

Market Drivers

Strict global safety regulations

Mandatory safety regulations across regions are making ABS standard in passenger cars, commercial vehicles, and two-wheelers, significantly boosting market penetration.

Rising demand for vehicle safety

Consumers increasingly prioritize safety features, and ABS has become essential for maintaining control during sudden braking and slippery road conditions.

Growth in vehicle production

Rising global production of passenger and commercial vehicles is directly increasing demand for ABS integration across all vehicle categories.

Integration with advanced safety systems

ABS is now integrated with ESC, traction control, and ADAS platforms, improving braking intelligence and overall vehicle performance.

Market Challenges

Cost pressure in entry-level vehicles

ABS increases vehicle cost, limiting full penetration in low-cost segments despite regulatory progress.

Maintenance complexity

System components such as sensors and hydraulic modules require specialized diagnostics and repair capabilities.

Uneven adoption in developing regions

Some emerging markets still show slower adoption in older vehicle fleets due to cost sensitivity and awareness gaps.

Market Segmentation

By Vehicle Type

Passenger vehicles dominate with 61.7% share due to regulatory compliance and high production volumes. Light commercial vehicles are growing fastest due to logistics expansion and safety requirements.

By Component

Electronic Control Units (ECU) lead the segment with 34.9% share as they manage real-time braking decisions and system coordination.

By Sales Channel

OEM segment dominates with 78.3% share due to factory installation of ABS in new vehicles across global markets.

By Technology

Four-channel ABS systems are most widely used due to precise control of individual wheel braking and enhanced stability performance.

Regional Analysis

Asia Pacific dominates the market with 38.6% share due to high vehicle production. North America follows with strong safety adoption, while Europe shows mature integration. Latin America and Middle East & Africa are gradually increasing penetration driven by regulatory improvements and fleet modernization.

Top Players Analysis

- Robert Bosch GmbH – Leading global supplier of ABS and integrated braking systems with strong OEM partnerships.

- Continental AG – Focuses on advanced braking electronics and integrated vehicle safety platforms.

- ZF Friedrichshafen AG – Develops intelligent braking systems combined with chassis control technologies.

- DENSO Corporation – Specializes in automotive electronics and precision braking components.

- Hyundai Mobis – Key supplier of integrated braking and safety systems for global OEM platforms.

- Aisin Corporation – Provides hydraulic and electronic braking system solutions for passenger and commercial vehicles.

- Knorr-Bremse AG – Leading supplier for heavy-duty ABS systems in trucks, buses, and rail applications.

- Hitachi Astemo Ltd. – Focuses on advanced braking technologies and electronic vehicle control systems.

Conclusion

The automotive anti lock braking system market is expected to maintain steady growth through 2034 driven by regulatory mandates, rising safety awareness, and integration with advanced vehicle electronics. ABS is evolving into a core component of intelligent mobility systems.

Get Your Sample Report Here: https://www.redlinepulse.com/report/automotive-anti-lock-braking-system-market/request-sample