Automotive Interior Material Market

Get Your Sample Report Here

https://www.redlinepulse.com/report/automotive-interior-material-market/request-sample

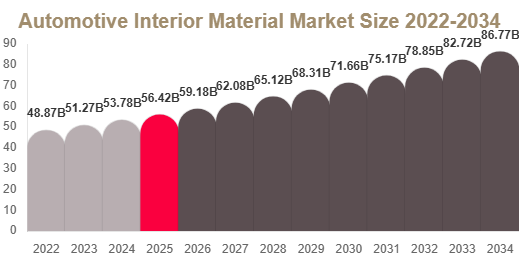

Automotive Interior Material Market Size

The automotive interior material market size was valued at USD 56.42 billion in 2025 and is projected to reach USD 59.18 billion in 2026.

The market is expected to expand to USD 86.74 billion by 2034, registering a CAGR of 4.9% from 2025 to 2034.

Automotive interior materials include plastics, leather, fabrics, vinyl, polyurethane, thermoplastic elastomers, wood trims, and advanced soft-touch composites used across dashboards, door panels, seats, headliners, carpets, consoles, and pillar trims. These materials play a central role in vehicle comfort, aesthetics, durability, thermal insulation, acoustic performance, and perceived quality.

Market Overview

Automotive interior materials are no longer limited to functional cabin components. They have become a defining factor in vehicle branding, user experience, and premium positioning across passenger and commercial vehicles. Increasing electrification, digital cockpit integration, and consumer expectations for comfort and sustainability are reshaping material selection strategies across global OEMs.

Market Trends

Rising Adoption of Sustainable and Recycled Interior Materials

Automakers are increasingly shifting toward recycled polyester fabrics, bio-based foams, natural fiber composites, and low-emission coatings. These materials are widely used in seats, headliners, carpets, and door trims to reduce environmental impact. Sustainability has become a core design principle, especially in electric and premium vehicle segments.

Premium Cabin Design Expansion into Mass Vehicles

Soft-touch plastics, synthetic leather, acoustic foams, and decorative trims are increasingly being integrated into mid-range vehicles. This trend reflects the growing importance of cabin experience, where tactile quality and visual refinement are becoming key purchase drivers.

Market Drivers

Rising Demand for Comfort and Cabin Experience

Consumers now prioritize interior comfort, aesthetics, and technology integration when purchasing vehicles. Features such as seat quality, dashboard finish, noise insulation, and ambient design significantly influence buying decisions. This is driving strong demand for premium interior materials across all vehicle categories.

Expansion of Electric Vehicles

Electric vehicles are accelerating the demand for lightweight, low-noise, and sustainable interior materials. EV cabin designs rely heavily on engineered polymers, recycled fabrics, and advanced foams to improve range efficiency and enhance passenger experience.

Market Challenges

Raw Material Price Volatility

Fluctuations in petroleum-based polymers, foams, synthetic leather inputs, and textile chemicals significantly impact production costs. This creates pricing pressure for OEMs and suppliers, especially in high-volume vehicle platforms where cost control is critical.

Sustainability and Recycling Limitations

Certain interior materials, especially mixed composites and thermosets, present recycling challenges. This limits full alignment with circular economy goals and forces automakers to balance sustainability with performance and cost efficiency.

Market Opportunities

Growth in Sustainable Luxury Interiors

Demand is rising for eco-friendly yet premium-feel cabin materials such as recycled leather alternatives, bio-based foams, and natural fiber trims. This is particularly strong in electric SUVs and premium passenger vehicles.

Innovation in Smart Cabin Architecture

Modern vehicle interiors are evolving toward digital, modular, and connected designs. This creates demand for lightweight, durable, and multifunctional materials that support ambient lighting, large displays, and integrated surfaces.

Segment Analysis

By Material Type

Plastics and Polymers Segment

Plastics and polymers dominate the market due to their cost efficiency, design flexibility, and lightweight properties. Materials such as polypropylene, ABS, and thermoplastic elastomers are widely used in dashboards, consoles, trims, and structural cabin parts.

Sustainable and Recycled Materials Segment

This segment is expanding rapidly as automakers adopt recycled fabrics, bio-based foams, and low-VOC materials. It is strongly supported by electric vehicle production and sustainability-focused vehicle platforms.

By Application

Seats Segment

Seats represent the largest application segment due to high material usage. Leather, foam, fabrics, and synthetic materials are used to enhance comfort, durability, and ergonomic performance.

Dashboard and Door Panels Segment

This segment is growing rapidly due to increasing integration of soft-touch surfaces, ambient lighting, digital displays, and decorative trims that enhance cabin aesthetics.

By Vehicle Type

Passenger Cars Segment

Passenger cars dominate the market due to high production volume and extensive interior material usage across seating, trims, and cabin systems.

Electric Vehicles Segment

Electric vehicles are the fastest-growing segment due to demand for lightweight, sustainable, and noise-reducing interior materials designed for modern cabin architectures.

Regional Analysis

Asia Pacific

Asia Pacific leads the market due to high vehicle production and rapid EV adoption. Strong demand for affordable and durable interior materials supports regional growth across passenger and commercial vehicles.

Europe

Europe shows strong demand for sustainable and premium interior materials. High adoption of eco-friendly trims and advanced cabin design technologies drives market expansion.

North America

North America is driven by SUVs and pickup trucks with feature-rich interiors. Demand for comfort-oriented seating, soft-touch materials, and durable trims remains strong.

Latin America

Latin America is growing steadily due to increasing vehicle production and rising demand for cost-efficient interior materials in compact vehicles.

Middle East and Africa

Demand is supported by SUVs and luxury imports requiring durable, heat-resistant interior materials suitable for harsh climates.

Competitive Landscape

The automotive interior material market is highly competitive, with companies focusing on sustainability, lightweight materials, and premium cabin experience innovation. Strong OEM partnerships and material technology advancements define market leadership.

1. Lear Corporation

Lear Corporation is a leading supplier in seating systems and interior integration. It provides advanced seating materials and modular interior solutions across global OEM platforms.

2. Adient plc

Adient specializes in automotive seating systems with strong material engineering capabilities focused on comfort, durability, and lightweight design.

3. Faurecia SE

Faurecia SE focuses on cockpit systems, seating, and interior technologies, with strong emphasis on sustainable and connected cabin solutions.

4. Grupo Antolin

Grupo Antolin provides interior trim systems including headliners, door panels, and lighting-integrated components.

5. Toyota Boshoku Corporation

Toyota Boshoku specializes in integrated interior systems including seats, trims, and filtration materials with strong OEM alignment.

6. Yanfeng Automotive Interiors

Yanfeng delivers cockpit systems and interior modules with strong expertise in modular and digital cabin design.

7. BASF SE

BASF develops advanced polymers, foams, and coating materials used widely in automotive interior applications.

8. Covestro AG

Covestro provides high-performance polyurethanes and coatings used in seats, dashboards, and decorative interior surfaces.