Fleet Electrification Market Overview

Get Your Sample Report Here: https://www.redlinepulse.com/report/fleet-electrification-market/request-sample

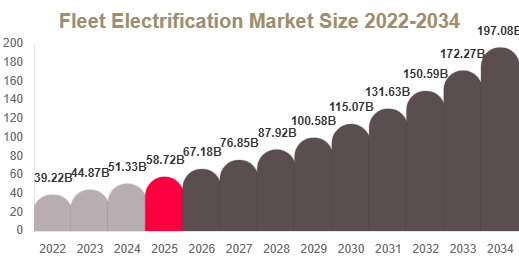

Market Size

The global fleet electrification market size was valued at USD 58.42 billion in 2025 and is projected to reach USD 67.18 billion in 2026. By 2034, the market is forecast to reach USD 196.54 billion, registering a CAGR of 14.4% from 2025 to 2034.

Fleet electrification includes electric vehicles, charging infrastructure, energy management systems, telematics integration, and fleet analytics that support operational efficiency and emission reduction across commercial transport ecosystems.

Market Drivers

Regulatory Pressure and Sustainability Commitments

One of the primary drivers of the fleet electrification market is the increasing regulatory push for emission reduction. Governments are implementing strict carbon targets, low-emission zones, and fleet transition incentives. At the same time, enterprises are aligning with net-zero goals, accelerating electric fleet adoption across logistics, municipal, and corporate mobility operations.

Lower Operating Costs and Total Cost of Ownership Advantage

Electric fleets are increasingly preferred due to lower fuel and maintenance costs compared to internal combustion vehicles. Fleet operators are shifting toward lifecycle cost evaluation, where EVs offer long-term economic benefits, especially in urban and delivery-based operations with predictable routes.

Market Challenges

High Infrastructure Investment and Deployment Complexity

A major challenge in fleet electrification is the high upfront investment required for charging infrastructure, grid upgrades, and fleet management systems. Operators must also manage route optimization, depot redesign, and energy planning, which increases operational complexity and slows large-scale adoption.

Grid Dependency and Transition Barriers

Fleet electrification depends heavily on grid capacity and charging availability. In regions with weak infrastructure, scaling electric fleets becomes difficult due to limited charging access, long installation timelines, and energy load constraints, especially for heavy-duty applications.

Segment Analysis

By Vehicle Type

Light commercial vehicles dominate the market due to strong adoption in delivery and logistics fleets. Their predictable routes and return-to-base operations make them ideal for electrification. Electric buses and medium-duty fleets are emerging rapidly as governments support public transport electrification programs.

By Propulsion Type

Battery electric vehicles (BEVs) hold the largest share due to zero emissions and lower operating costs. Plug-in hybrid electric vehicles (PHEVs) are growing as transitional solutions in fleets requiring extended range and flexible operations across mixed urban and regional routes.

By Charging Type

Depot charging dominates the market as most fleet vehicles return to centralized locations. Smart depot systems with energy optimization and load balancing are becoming essential for managing large-scale EV operations efficiently.

By End Use

Logistics and delivery fleets lead the market due to the rise of e-commerce and last-mile delivery demand. Public transportation and municipal fleets are growing fastest, driven by government funding and urban sustainability initiatives.

Top Players Analysis

1. Ford Motor Company

Ford is strengthening its position in commercial electrification with expanding electric van and fleet mobility solutions. The company focuses on integrated fleet services, charging ecosystems, and scalable EV deployment for logistics operators.

2. Tesla, Inc.

Tesla plays a key role in fleet electrification through its electric vehicle platforms and energy ecosystem. Its vehicles are widely adopted in corporate and delivery fleets due to efficiency, range, and software integration.

3. BYD Company Ltd.

BYD leads in electric buses and commercial EV manufacturing. The company has strong penetration in public transportation electrification projects across global markets, especially in Asia and Europe.

4. Rivian Automotive, Inc.

Rivian focuses on electric delivery vans and logistics fleet solutions. Its collaboration with major delivery operators supports large-scale electrification of last-mile transportation networks.

5. ABB Ltd.

ABB is a major charging infrastructure provider, offering fast-charging and depot electrification solutions. The company plays a critical role in enabling fleet scalability through energy and charging system integration.

Market Opportunities

Heavy-Duty Fleet Electrification Expansion

The electrification of buses, trucks, and vocational fleets represents a major growth opportunity. Advancements in battery capacity and charging infrastructure are enabling expansion into long-haul and high-load applications.

Fleet-as-a-Service Models

Integrated fleet-as-a-service models combining vehicles, charging, maintenance, and software are gaining traction. These solutions reduce complexity for operators and accelerate electrification adoption across SMEs and municipal fleets.

Conclusion

The fleet electrification market is entering a rapid expansion phase driven by sustainability mandates, cost efficiency, and technological advancement. While infrastructure challenges remain, strong government support and evolving fleet models are expected to accelerate adoption across global transportation ecosystems.