Tanzania Used Car Market Size

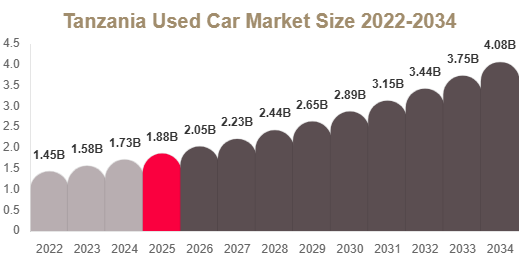

The Tanzania Used Car market size is estimated at USD 1.85 billion in 2025, and it is projected to reach USD 2.05 billion in 2026. By 2034, the market is expected to reach approximately USD 4.10 billion, registering a CAGR of 9.0% during 2025–2034.

This growth reflects strong dependence on pre-owned vehicles as an affordable mobility solution across Tanzania’s expanding urban and semi-urban regions.

Get Your Sample Report Here: https://www.redlinepulse.com/report/tanzania-used-car-market/request-sample

Market Overview

The Tanzania Used Car Market is expanding steadily due to rising demand for cost-effective transportation, increasing urban population, and improving access to imported vehicles. Consumers in Tanzania heavily rely on imported used cars, especially from Japan, Europe, and the Middle East, due to affordability and availability of reliable models.

The market is also supported by limited penetration of new vehicles, high import costs, and growing entrepreneurial activities in transport and logistics sectors.

Market Drivers

Rising demand for affordable mobility

One of the strongest drivers of the Tanzania Used Car Market is affordability. New vehicles remain expensive due to import duties, taxes, and financing limitations. Used cars provide a practical alternative for middle-income consumers, small business owners, and ride-hailing operators.

Expansion of urban transportation and ride services

The growth of ride-hailing services and informal transport businesses is increasing the demand for low-cost vehicles. Many drivers prefer used cars due to lower upfront investment and easier maintenance, which supports continuous market demand.

Increasing vehicle imports from Japan and Europe

Tanzania depends heavily on imported used vehicles. Japan remains a dominant source due to fuel-efficient and durable cars, while Europe supplies high-quality models. This import-driven supply chain ensures consistent availability of vehicles in the market.

Market Challenges

Import restrictions and regulatory limitations

Government regulations such as age limits on imported vehicles and emission standards can restrict supply. These policies, while improving environmental standards, sometimes increase vehicle costs and reduce availability of preferred models.

Currency fluctuations and import cost pressure

Exchange rate volatility impacts import costs significantly. Since most used vehicles are imported, any currency depreciation increases pricing pressure for end users, affecting overall market stability.

Presence of unorganized market players

The market includes a large number of informal dealers who often offer inconsistent quality. This creates trust issues among buyers and affects organized dealerships competing on quality assurance and transparency.

Market Trends

Growth of online used car platforms

Digital platforms are transforming the Tanzania Used Car Market. Buyers now prefer browsing vehicles online, comparing prices, and accessing inspection reports before purchase. This improves transparency and expands buyer reach.

Increasing demand for fuel-efficient vehicles

Rising fuel prices are pushing consumers toward fuel-efficient cars such as compact gasoline vehicles and hybrid models. This trend is influencing import preferences and reshaping demand patterns.

Shift toward certified used cars

There is growing interest in certified pre-owned vehicles, where dealers offer inspected cars with warranties. This is improving consumer confidence and increasing organized dealership participation.

Segment Analysis

Vehicle Type Segment

Passenger cars dominate the Tanzania Used Car Market with a share of 62.80% in 2025, driven by high demand for personal transportation in urban areas. Compact and mid-size cars are preferred due to affordability and fuel efficiency. Expanding urbanization in cities like Dar es Salaam is further strengthening demand.

Commercial vehicles are the fastest-growing segment with increasing demand from logistics, construction, and public transport sectors. Entrepreneurs prefer used commercial vehicles due to lower investment costs and quick business deployment.

Fuel Type Segment

Gasoline vehicles dominate the market with a share of 54.10% in 2025 due to their availability, lower cost, and suitability for urban driving conditions. They remain the most imported category from Japan and Europe.

Diesel vehicles are the fastest-growing segment, driven by demand in commercial transport and logistics. Their fuel efficiency and durability make them suitable for heavy-duty applications and long-distance travel.

Sales Channel Segment

Offline dealerships dominate the market with a share of 57.90% in 2025 due to customer preference for physical inspection and trust-based transactions. Dealerships also offer financing support and after-sales services.

Online platforms are the fastest-growing segment as digital adoption increases. Platforms such as listing websites and mobile apps allow users to compare vehicles easily and access a wider selection, improving market transparency.

Regional Analysis

North America

North America contributes significantly as an export source of used vehicles. The United States dominates due to large vehicle inventory and strong export channels to Tanzania.

Europe

Europe is a key exporter of used cars, especially Germany and the UK, known for high-quality and fuel-efficient vehicles. Strict maintenance standards ensure reliable supply to African markets.

Asia Pacific

Asia Pacific dominates supply, with Japan leading exports due to strong demand in Tanzania for reliable and affordable vehicles. Japanese used cars are highly preferred for durability and fuel efficiency.

Middle East & Africa

The region acts as a re-export hub, with the UAE playing a central role in vehicle redistribution to African markets, including Tanzania.

Latin America

Latin America contributes smaller volumes but remains part of global used vehicle supply chains, supporting market diversity.

Competitive Landscape

The Tanzania Used Car Market is fragmented, consisting of international exporters, local dealers, and online platforms competing on price, availability, and service quality. Companies are focusing on digital transformation and logistics efficiency to strengthen their presence.

Key Players Analysis

- Be Forward Co., Ltd.

A leading global exporter of used vehicles with strong presence in East Africa. The company focuses on large inventory availability and direct export services to Tanzania. - SBT Japan

Specializes in Japanese used car exports. It benefits from strong sourcing networks and offers a wide range of fuel-efficient vehicles preferred in Tanzania. - Car Junction Tanzania

Focuses on direct import and local distribution. The company provides customized vehicle sourcing and supports both retail and wholesale buyers. - Autochek Africa

A digital automotive marketplace that is transforming vehicle buying through online listings, financing solutions, and inspection services. - Jiji Tanzania

A popular online classifieds platform enabling peer-to-peer used car transactions and dealer listings, increasing market accessibility.

Conclusion

The Tanzania Used Car Market is expected to grow strongly over the forecast period due to affordability, rising urbanization, and increasing dependence on imported vehicles. Expansion of digital platforms, financing options, and certified pre-owned programs will further strengthen market structure and improve transparency across the ecosystem.