Automotive Rain Light Humidity Sensor Market Overview

Get Your Sample Report Here: https://www.redlinepulse.com/report/automotive-rain-light-humidity-sensor-market/request-sample

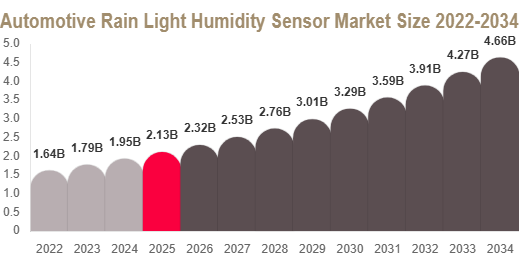

Market Size

The global market size is estimated at USD 2.14 billion in 2025, and it is projected to reach USD 2.32 billion in 2026. By 2034, the market is expected to reach approximately USD 4.68 billion, expanding at a CAGR of 9.1% during the forecast period (2025–2034).

The Automotive Rain Light Humidity Sensor Market is growing steadily due to rising adoption of ADAS, increasing demand for vehicle comfort automation, and rapid integration of smart sensing systems in modern vehicles. Expansion of electric and autonomous vehicles is further strengthening demand for multi-functional environmental sensing technologies.

Market Drivers and Challenges

Rising demand for vehicle automation and comfort systems

The market is strongly driven by increasing consumer demand for automated comfort features such as automatic wipers, adaptive headlights, and climate-responsive systems. These sensors reduce driver workload by automatically responding to changing weather conditions. Premium and mid-range vehicles are increasingly integrating these systems as standard features, improving driving convenience and safety.

Expansion of ADAS and smart mobility systems

The rapid expansion of ADAS is a major growth driver for the Automotive Rain Light Humidity Sensor Market. These sensors support intelligent functions such as automatic headlight activation and weather-based driving adjustments. As regulatory standards for vehicle safety tighten globally, integration of ADAS-enabled sensing systems is becoming essential across vehicle categories.

Growth of electric and autonomous vehicles

Electric and autonomous vehicles rely heavily on environmental sensing systems for real-time decision-making. Rain light humidity sensors play a key role in enabling automated visibility and cabin control systems. Increasing EV adoption is driving demand for energy-efficient and highly accurate sensor technologies.

High cost and calibration complexity

A key challenge is the high cost and calibration complexity of advanced sensor systems. These sensors require precise alignment and optical calibration to function under varying environmental conditions. Factors such as dirt accumulation, vibration, and harsh weather conditions can impact performance and increase maintenance requirements.

Market Trends

Integration of smart cabin automation systems

Modern vehicles are increasingly equipped with smart cabin automation systems that automatically control wipers, headlights, and air conditioning. Rain light humidity sensors are integrated with vehicle ECUs and ADAS platforms to enable real-time environmental response. This trend is particularly strong in premium vehicles and electric vehicles.

Shift toward multi-functional sensor modules

Automakers are adopting multi-functional sensor systems capable of detecting rain, light intensity, and humidity within a single module. This reduces wiring complexity, improves space efficiency, and lowers production costs. These systems also enhance accuracy by combining multiple environmental inputs into a unified control mechanism.

Advancements in optical and infrared sensing

Continuous innovation in optical and infrared sensing technologies is improving detection accuracy and response time. These advancements are enabling better performance in extreme weather conditions, supporting wider adoption across all vehicle categories.

Segmental Analysis

By Sensor Type

Optical rain sensors dominated the market with 42.6% share in 2025 due to high accuracy in detecting rainfall intensity and light conditions. These sensors are widely used in automatic wiper and headlight control systems across passenger vehicles.

Capacitive humidity sensors are the fastest-growing segment, driven by increasing adoption in electric vehicles and smart climate control systems. These sensors enable precise cabin environment monitoring and improve passenger comfort.

By Vehicle Type

Passenger vehicles accounted for 61.4% share in 2025 due to high production volumes and increasing integration of automated comfort features. Growing demand for SUVs and premium cars further supports this dominance.

Electric vehicles are the fastest-growing segment as they increasingly rely on intelligent sensing systems for energy efficiency and automated environmental control.

By Application

Automatic wiper control dominated with 46.3% share in 2025 due to widespread adoption across global vehicle platforms. These systems enhance safety and visibility during adverse weather conditions.

Headlight control systems are the fastest-growing application, driven by rising adoption of ADAS and smart lighting technologies.

Regional Analysis

North America

North America held 35.2% share in 2025, driven by strong adoption of ADAS-equipped vehicles and high demand for automotive comfort features. The United States leads the region due to advanced automotive innovation and widespread use of smart cabin systems. Growth is further supported by increasing EV adoption and connected vehicle platforms.

Europe

Europe accounted for 29.4% share in 2025, supported by strict safety regulations and strong demand for premium vehicles. Germany leads the region due to advanced automotive engineering and integration of smart sensor systems in EVs and hybrids.

Asia Pacific

Asia Pacific dominates the market with 44.8% share in 2025 and is the fastest-growing region. China leads due to massive automotive production and EV expansion. India and Japan are also contributing through rising vehicle demand and sensor technology adoption.

Middle East & Africa

This region held 6.2% share in 2025, driven by increasing demand for premium vehicles and gradual adoption of automotive automation technologies. Saudi Arabia and the UAE lead due to strong luxury vehicle markets.

Latin America

Latin America accounted for 5.0% share in 2025, supported by rising automotive production and increasing adoption of modern vehicle electronics. Brazil and Mexico are the key contributors to regional growth.

Competitive Landscape

The market is moderately consolidated with strong competition focused on sensor innovation and integration with automotive electronics systems. Companies are investing heavily in ADAS-compatible sensing solutions and AI-driven environmental detection technologies.

- Bosch

Bosch is a leading player in automotive sensing technologies, offering advanced rain, light, and humidity sensor systems integrated with smart cabin automation and ADAS platforms. - Continental AG

Continental AG focuses on high-performance sensor systems designed for real-time environmental detection and integration with vehicle control units. - Denso Corporation

Denso develops advanced automotive sensors with strong focus on precision, durability, and energy-efficient vehicle applications. - HELLA GmbH

HELLA specializes in optical sensing technologies used in automatic wiper and lighting control systems across passenger and commercial vehicles. - Valeo

Valeo is a key innovator in smart automotive sensor systems, focusing on multi-functional environmental sensing for modern connected vehicles.

Key Players List

- Bosch

- Continental AG

- Denso Corporation

- HELLA GmbH

- Valeo

- Aptiv PLC

- Sensata Technologies

- Infineon Technologies

- TE Connectivity

- Honeywell International

- NXP Semiconductors

- ZF Friedrichshafen

- Panasonic Automotive

- Stoneridge Inc.

- Mitsubishi Electric