Automotive Energy Absorption (EA) Pad Market Research Report

Get Your Sample Report Here: https://www.redlinepulse.com/report/automotive-energy-absorption-ea-pad-market/request-sample

Market Overview

The Automotive Energy Absorption (EA) Pad Market is witnessing steady expansion as vehicle manufacturers increasingly prioritize passenger safety and crash protection standards. According to Redline Pulse, EA pads play a critical role in absorbing impact energy during collisions, thereby reducing injury risk and enhancing overall vehicle safety performance.

These components are widely used across door panels, dashboards, pillars, and roof liners, making them essential for modern automotive safety architecture. Growing adoption of electric vehicles and advancements in material science are further accelerating market development.

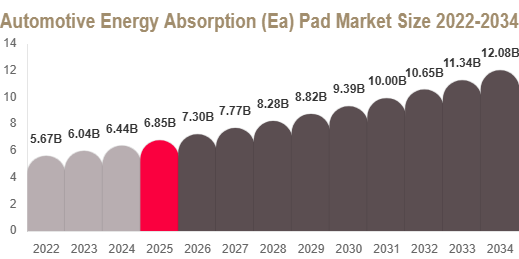

Market Size

The Automotive Energy Absorption (EA) Pad market size was valued at USD 6.8 billion in 2025 and is projected to reach USD 7.3 billion in 2026.

The market is expected to reach approximately USD 12.9 billion by 2034, registering a CAGR of 6.5% from 2025 to 2034.

Market Drivers

Stringent Vehicle Safety Regulations

Increasing global safety regulations are pushing automakers to integrate advanced energy absorption systems. EA pads are essential for meeting crash safety standards and improving occupant protection during collisions.

Rising Production of Passenger Vehicles

The growing production of passenger vehicles is significantly driving demand for safety components. Increasing vehicle ownership in emerging economies is further supporting market expansion.

Growth of Electric Vehicles

Electric vehicles require specialized safety solutions due to battery placement and structural design differences. This is increasing demand for advanced EA pads with higher energy absorption capabilities.

Increasing Consumer Awareness of Safety

Consumers are becoming more aware of vehicle safety features, encouraging automakers to integrate advanced materials that improve crash protection and cabin comfort.

Market Challenges

High Cost of Advanced Materials

Advanced materials such as composite foams and high-performance polymers increase production costs, limiting adoption in low-cost vehicle segments.

Manufacturing Complexity

The production of multi-layer and high-performance EA pads requires specialized equipment and technical expertise, increasing operational complexity.

Raw Material Price Fluctuations

Volatility in raw material prices impacts manufacturing costs and can affect profitability for producers.

Limited Adoption in Entry-Level Vehicles

Cost constraints in budget vehicle segments often lead manufacturers to use basic materials instead of advanced EA solutions.

Segment Analysis

According to Redline Pulse, the market is segmented by material type, vehicle type, application, and end-use.

By Material Type

Polymer Foam

Polymer foam dominates the market due to its excellent energy absorption capacity, lightweight nature, and cost efficiency. It is widely used across multiple vehicle applications.

Composite Materials

Composite materials are witnessing rapid growth due to superior performance, durability, and lightweight characteristics, making them ideal for modern automotive safety systems.

Rubber-Based Materials

Rubber-based materials are used in specific applications requiring flexibility, vibration control, and moderate energy absorption.

By Vehicle Type

Passenger Vehicles

Passenger vehicles dominate the market due to high production volume and increasing demand for advanced safety features.

Commercial Vehicles

Commercial vehicles are adopting EA pads to improve crash safety and structural durability.

Electric Vehicles

Electric vehicles represent the fastest-growing segment due to increasing adoption and demand for specialized safety solutions.

By Application

Door Panels

Door panels hold a significant share as they are critical for side-impact protection and occupant safety.

Dashboard Systems

Dashboards use EA pads to enhance safety and reduce injury risk during frontal collisions.

Pillars

Pillar applications are growing rapidly due to increased focus on structural reinforcement and crash energy distribution.

Roof Liners

Roof liners incorporate EA pads for improved head protection and overall cabin safety enhancement.

By End-Use

OEM

OEM segment dominates due to direct integration of EA pads during vehicle manufacturing for compliance with safety standards.

Aftermarket

Aftermarket demand is growing as vehicle owners upgrade or replace safety components for improved performance.

Regional Analysis

North America leads the market due to strict safety regulations and strong automotive manufacturing presence. Europe follows with a focus on lightweight materials and sustainability-driven safety solutions. Asia Pacific is the fastest-growing region due to high vehicle production, rising safety awareness, and expanding automotive industries.

The Middle East & Africa region is gradually adopting advanced safety technologies, supported by increasing premium vehicle demand. Latin America is also witnessing steady growth due to rising vehicle ownership and improving automotive safety standards.

Key Players Analysis

According to Redline Pulse, the market includes major global material suppliers and automotive component manufacturers focusing on innovation and safety advancements.

- BASF SE

A leading chemical company providing advanced polymer foams and energy absorption materials for automotive applications. - Dow Inc.

Specializes in high-performance materials used in automotive safety and structural applications. - Huntsman Corporation

Develops polyurethane-based solutions widely used in energy absorption systems. - 3M Company

Offers advanced adhesive and material solutions enhancing vehicle safety and durability. - Saint-Gobain

Focuses on innovative material solutions for automotive safety and insulation applications. - Covestro AG

Provides advanced polycarbonate and polyurethane materials for automotive safety systems. - Zotefoams plc

Specializes in lightweight foam materials used in energy absorption applications. - JSP Corporation

Known for expanded polypropylene foam used in automotive safety components. - Armacell International

Focuses on flexible foam materials for vibration control and energy absorption. - Recticel Group

Provides polyurethane foam solutions widely used in automotive safety systems.

Competitive Landscape

The market is moderately competitive, with companies focusing on material innovation, lightweight solutions, and sustainability. Strategic collaborations between material suppliers and automotive OEMs are driving advancements in energy absorption technologies. Continuous R&D efforts are focused on improving performance while reducing material costs.

Conclusion

The Automotive Energy Absorption (EA) Pad Market is expected to grow steadily through 2034, driven by increasing safety regulations, rising vehicle production, and expanding electric vehicle adoption. Despite challenges related to cost and manufacturing complexity, innovation in materials and design is expected to support long-term market expansion.

Get Your Sample Report Here: https://www.redlinepulse.com/report/automotive-energy-absorption-ea-pad-market/request-sample