Automotive LCD Display Market Research Report

Get Your Sample Report Here: https://www.redlinepulse.com/report/automotive-lcd-display-market/request-sample

Market Overview

The Automotive LCD Display Market is experiencing strong growth as automotive manufacturers increasingly adopt digital cockpit systems and advanced infotainment solutions. According to Redline Pulse, LCD displays have become a core component of modern vehicles, used across instrument clusters, center stack displays, and rear-seat entertainment systems.

The increasing shift toward connected, electric, and autonomous vehicles is further driving demand for high-resolution and energy-efficient display systems. Advancements in TFT-LCD, OLED, and curved display technologies are enhancing visibility, functionality, and user experience inside vehicles.

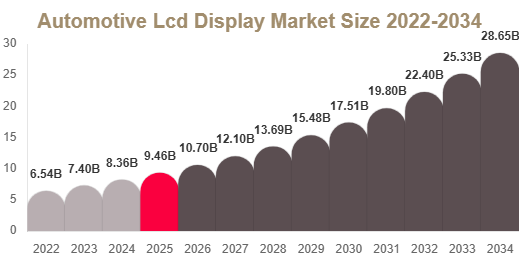

Market Size

The Automotive LCD Display market size was valued at USD 9.4 billion in 2025 and is projected to reach USD 10.7 billion in 2026.

The market is expected to reach approximately USD 28.6 billion by 2034, registering a CAGR of 13.1% from 2025 to 2034.

Market Drivers

Rising Demand for Digital Cockpit Systems

Automotive manufacturers are increasingly replacing analog dashboards with fully digital cockpit systems. LCD displays integrate instrument clusters, infotainment, and navigation into a unified interface, improving user experience and vehicle safety.

Growth of Electric and Connected Vehicles

Electric vehicles rely heavily on LCD displays to provide real-time data such as battery status, range, and energy consumption. Connected vehicles also use displays for navigation, entertainment, and diagnostics.

Technological Advancements in Display Panels

Innovations in TFT-LCD, OLED, and curved screen technologies are enhancing brightness, clarity, and energy efficiency. These improvements are enabling more immersive and interactive vehicle interiors.

Increasing Demand for In-Vehicle Entertainment

Consumers are demanding advanced infotainment systems with larger and more responsive displays. Rear-seat entertainment systems are also gaining popularity, especially in premium vehicles.

Market Challenges

High Cost of Advanced Display Systems

High-resolution and multi-display setups increase overall vehicle production costs, limiting adoption in low-cost vehicle segments.

Integration Complexity

Integrating LCD systems with vehicle electronics, sensors, and infotainment platforms requires complex engineering and increases development time.

Durability Concerns

Automotive environments expose displays to heat, vibration, and sunlight, requiring durable and high-performance materials that increase manufacturing costs.

Limited Adoption in Entry-Level Vehicles

Budget vehicles often avoid advanced display systems due to cost constraints, limiting market penetration in developing regions.

Segment Analysis

According to Redline Pulse, the Automotive LCD Display Market is segmented by display type, application, vehicle type, and sales channel.

By Display Type

TFT-LCD

TFT-LCD dominates the market due to its cost-effectiveness, durability, and wide usage in instrument clusters and infotainment systems.

OLED

OLED displays are gaining rapid traction due to superior image quality, flexibility, and energy efficiency.

AMOLED

AMOLED displays are used in premium vehicles for high contrast, vivid colors, and enhanced visual performance.

By Application

Instrument Cluster

Instrument clusters dominate the market as they provide essential driving information such as speed, fuel, and navigation.

Center Stack Display

Center stack displays are growing rapidly due to increasing demand for infotainment and connectivity features.

Rear Seat Entertainment

Rear-seat displays are gaining popularity in luxury and family vehicles, offering enhanced passenger experience.

By Vehicle Type

Passenger Vehicles

Passenger vehicles dominate the market due to high adoption of digital infotainment systems and connected features.

Commercial Vehicles

Commercial vehicles are adopting LCD displays for fleet management, navigation, and driver assistance.

Electric Vehicles

Electric vehicles are the fastest-growing segment due to their reliance on digital interfaces for operational data.

By Sales Channel

OEM

OEM channels dominate due to factory-installed display systems ensuring reliability and integration.

Aftermarket

Aftermarket sales are growing as consumers upgrade vehicle interiors with advanced display systems.

Online Retail

Online retail is expanding rapidly due to easy access, competitive pricing, and wide product availability.

Regional Analysis

North America leads the market due to high adoption of connected vehicles and advanced automotive technologies. Europe follows with strong demand for premium vehicles and digital cockpit integration.

Asia Pacific is the fastest-growing region due to large-scale automotive production, rising EV adoption, and increasing consumer demand for smart vehicle technologies. China, Japan, and India are key contributors.

The Middle East & Africa region is witnessing steady growth driven by luxury vehicle demand and increasing adoption of smart mobility solutions. Latin America is also growing due to rising vehicle ownership and infotainment system adoption.

Key Players Analysis

According to Redline Pulse, the Automotive LCD Display Market is highly competitive with strong participation from global electronics and automotive suppliers.

- LG Display Co., Ltd.

A leading manufacturer of advanced automotive display technologies including LCD and OLED panels. - Samsung Display Co., Ltd.

Focuses on high-resolution display technologies used in premium automotive infotainment systems. - BOE Technology Group Co., Ltd.

A major supplier of LCD panels with strong presence in automotive and consumer electronics markets. - Panasonic Holdings Corporation

Provides advanced infotainment and display solutions integrated into modern vehicles. - Continental AG

Develops integrated cockpit systems combining LCD displays with vehicle electronics. - Robert Bosch GmbH

Offers advanced automotive electronic systems including digital display interfaces. - Visteon Corporation

Specializes in digital cockpit platforms and automotive display solutions. - Denso Corporation

Focuses on automotive electronics and integrated display technologies for vehicles. - Nippon Seiki Co., Ltd.

Known for precision instrument clusters and automotive display systems. - Hyundai Mobis Co., Ltd.

Develops next-generation cockpit systems with advanced LCD display integration.

Competitive Landscape

The market is highly competitive, with companies investing in advanced display technologies, miniaturization, and energy-efficient solutions. Strategic partnerships between display manufacturers and automotive OEMs are driving innovation in digital cockpit systems. The focus remains on enhancing user experience, safety, and connectivity.

Conclusion

The Automotive LCD Display Market is expected to grow significantly through 2034, driven by rising adoption of connected vehicles, electric mobility, and advanced infotainment systems. Despite challenges such as high costs and integration complexity, continuous technological advancements are expected to fuel long-term market expansion.

Get Your Sample Report Here: https://www.redlinepulse.com/report/automotive-lcd-display-market/request-sample