Market Overview

The Non OEM EV MRO Market is gaining strong momentum as electric vehicle adoption accelerates globally and demand rises for affordable maintenance, repair, and overhaul services outside OEM networks. As per Redline Pulse, the market is driven by increasing EV fleet penetration, cost advantages offered by independent service providers, and rising demand for post-warranty vehicle servicing across passenger and commercial segments.

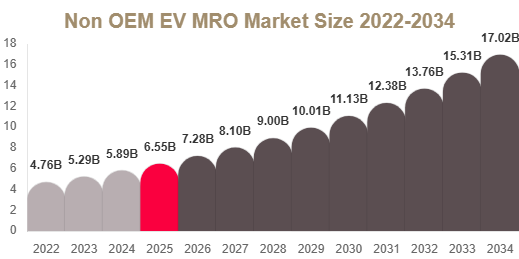

Non OEM EV MRO Market Size

Market Size 2025

The Non OEM EV MRO Market size is estimated at USD 6.45 billion in 2025, supported by increasing electric vehicles reaching mid-life service cycles.

Market Size 2034

By 2034, the market is forecasted to reach USD 18.90 billion, driven by expanding EV fleets and growing independent service networks.

CAGR (2025–2034)

The market is expected to grow at a CAGR of 11.2% during 2025–2034, reflecting strong demand for cost-effective EV maintenance solutions.

Market Drivers

Rapid Expansion of Electric Vehicle Fleets

The growing number of electric vehicles on roads is increasing demand for maintenance and repair services beyond OEM networks. As EVs enter mid-life cycles, service requirements are rising significantly.

Cost Advantages of Independent Service Providers

Non OEM workshops offer more affordable repair and maintenance services compared to OEM service centers, making them attractive for fleet operators and individual EV owners.

Growth of Shared Mobility and EV Fleets

Electric taxis, ride-hailing services, and logistics fleets are expanding rapidly, increasing demand for continuous maintenance and fast repair solutions.

Market Challenges

Limited Access to OEM Software and Diagnostics

Independent service providers often face restrictions in accessing proprietary EV software and diagnostic tools, limiting their repair capabilities.

Lack of Skilled EV Technicians

EV servicing requires specialized training in high-voltage systems and battery technologies, and shortage of skilled technicians can affect service quality.

Safety Risks in High-Voltage Systems

Improper handling of EV battery systems can lead to safety hazards, increasing operational risks for non OEM workshops.

Market Segmentation

By Service Type

Maintenance Services

This segment dominates with a 44.7% share in 2025 due to regular inspection needs such as battery health checks, cooling system servicing, and software updates.

Repair Services

Expected to grow at the fastest rate due to increasing EV aging fleets requiring component-level repairs like batteries and inverters.

Diagnostics Services

This segment is expanding with adoption of AI-based tools for real-time vehicle performance analysis.

Software & System Updates

Growing importance of EV software upgrades is driving demand for independent update services.

By Vehicle Type

Passenger EVs

This segment leads with a 58.5% share in 2025 due to high private EV ownership and post-warranty servicing needs.

Commercial EVs

Expected to grow fastest due to rising electric fleets in logistics, transport, and mobility services.

Two-Wheel Electric Vehicles

Growing rapidly in urban areas due to increasing adoption of electric scooters and bikes.

Electric Fleet Vehicles

Expanding steadily with fleet electrification in delivery and ride-hailing services.

By Component Type

Battery Systems

This is the dominant segment with a 39.6% share due to high replacement and maintenance demand.

Power Electronics

Expected to grow fastest due to increasing complexity of EV electronic systems like inverters and converters.

Thermal Management Systems

Important for maintaining battery efficiency and vehicle performance.

Electric Drivetrain Components

Includes motors and transmission systems requiring periodic servicing.

Key Players Analysis

Bosch

Bosch is a leading player with strong global service networks and advanced EV diagnostic solutions supporting independent workshops.

Mahle GmbH

Mahle focuses on thermal systems and EV component servicing solutions.

Denso Corporation

Denso provides advanced automotive aftermarket solutions including EV maintenance technologies.

LKQ Corporation

LKQ is a major aftermarket supplier offering replacement parts and repair services for EVs.

Valeo

Valeo specializes in EV systems and aftermarket service solutions with strong global presence.

ZF Aftermarket

ZF provides transmission and EV drivetrain servicing solutions for independent workshops.

Continental AG

Continental develops diagnostic and digital service tools for EV maintenance.

BorgWarner

BorgWarner supports EV drivetrain and power electronics servicing solutions.

Hitachi Astemo

Hitachi focuses on EV components and aftermarket service technologies.

Schaeffler AG

Schaeffler offers EV drivetrain and motion system maintenance solutions.

Regional Analysis

North America

North America holds a 36.2% share in 2025 due to mature EV adoption, strong aftermarket ecosystem, and rising right-to-repair initiatives supporting independent service providers.

Europe

Europe accounts for 27.5% share driven by strong EV penetration, regulatory support, and advanced automotive service infrastructure.

Asia Pacific

Asia Pacific is the fastest-growing region with a CAGR of 12.8% due to rapid EV adoption, expanding urban mobility, and strong independent service network growth.

Middle East & Africa

Growth is supported by increasing EV adoption and development of supporting service infrastructure in urban areas.

Latin America

Market growth is driven by rising EV adoption and expansion of cost-effective aftermarket service networks.

Conclusion

The Non OEM EV MRO Market is expected to grow significantly through 2034, driven by increasing EV penetration, rising maintenance demand, and expansion of independent service ecosystems. While challenges such as limited OEM access and technical skill gaps exist, growing regulatory support and cost advantages are expected to accelerate market expansion.

Get Your Sample Report Here: https://www.redlinepulse.com/report/non-oem-ev-mro-market/request-sample