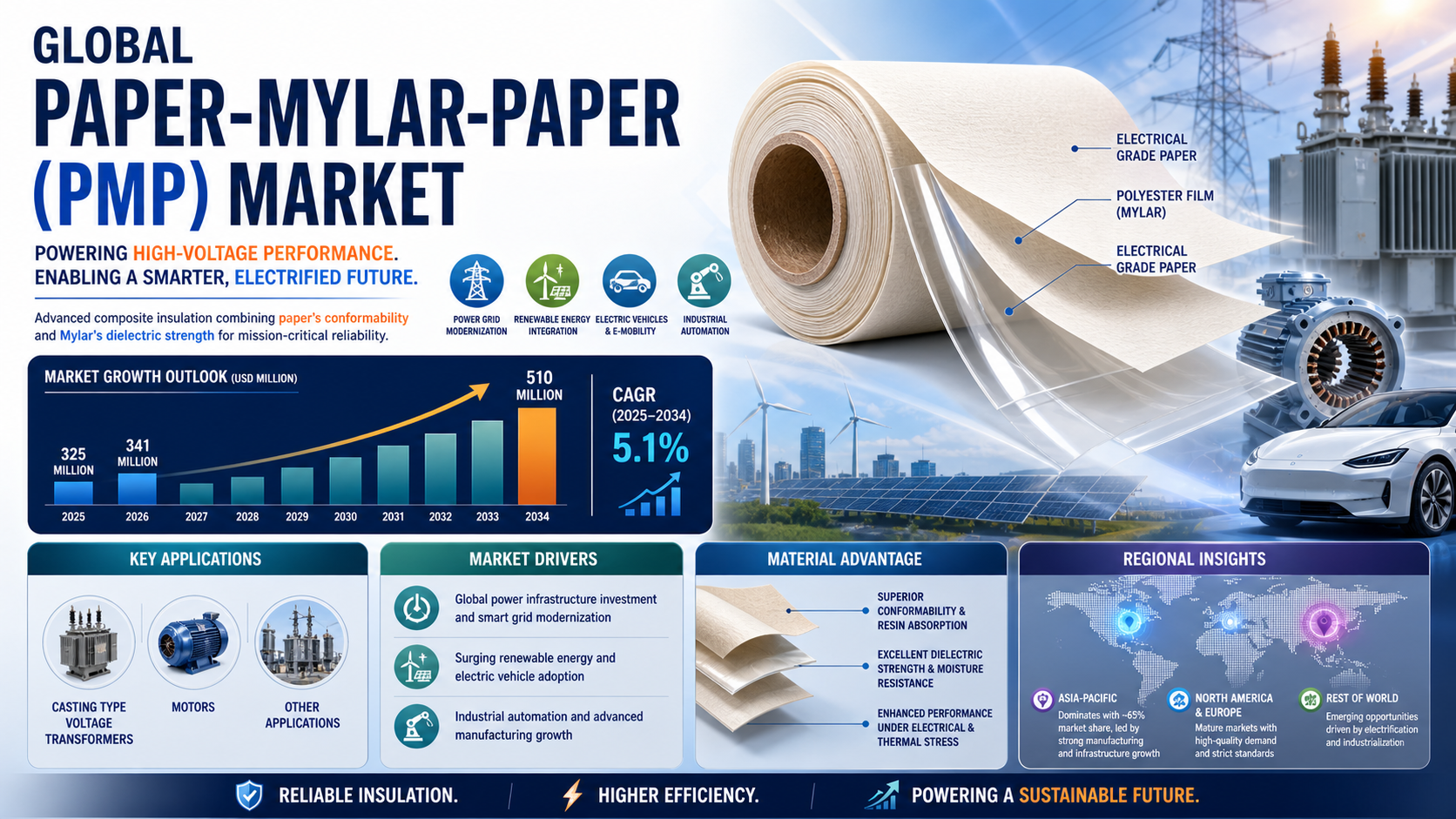

Global Paper-Mylar-Paper (PMP) market was valued at USD 325 million in 2025 and is projected to reach USD 510 million by 2034, exhibiting a steady CAGR of 5.1% during the forecast period.

Paper-Mylar-Paper (PMP), a composite electrical insulation material consisting of polyester film (Mylar) laminated between two layers of electrical grade paper, has become indispensable in high-voltage applications. This structure ingeniously combines Mylar's excellent dielectric strength and moisture resistance with paper's superior conformability and resin absorption properties. PMP serves primarily as barrier insulation, slot liners, and phase insulation in critical components like casting type voltage transformers and motors, where reliability under electrical and thermal stress is non-negotiable.

Get Full Report Here: https://www.24chemicalresearch.com/reports/304457/papermylarpaper-market

Market Dynamics:

The market's trajectory is shaped by a complex interplay of powerful growth drivers, significant restraints that are being actively addressed, and vast, untapped opportunities.

Powerful Market Drivers Propelling Expansion

- Global Power Infrastructure Modernization: The relentless expansion and upgrading of power grids worldwide represent the most significant growth vector. With countries investing heavily in smart grid technologies and replacing aging infrastructure, demand for reliable insulation materials like PMP has surged. The global push toward electrification, particularly in emerging economies, requires robust components that can withstand higher operational voltages and environmental challenges, positioning PMP as a critical enabler of grid resilience and efficiency.

- Renewable Energy Integration and Electric Vehicle Revolution: The renewable energy sector's explosive growth, particularly in solar and wind power, demands specialized electrical components where PMP excels. Solar inverters and wind turbine converters require insulation materials that can handle variable loads and harsh operating conditions. Simultaneously, the electric vehicle revolution has created unprecedented demand for efficient motors and power distribution systems. PMP's thermal stability and dielectric properties make it essential in EV motor insulation, with demand from this sector projected to double over the next five years.

- Industrial Automation and Technological Advancements: The ongoing industrial automation wave across manufacturing sectors requires motors and control systems that operate with greater efficiency and reliability. PMP's ability to enhance motor performance while providing consistent insulation has made it the material of choice for industrial applications. Furthermore, advancements in manufacturing processes have improved PMP's quality and consistency, enabling its use in more demanding applications while maintaining cost-effectiveness.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/304457/papermylarpaper-market

Significant Market Restraints Challenging Adoption

Despite its critical importance, the market faces hurdles that must be overcome to achieve broader adoption.

- High Production Costs and Manufacturing Complexity: Producing high-quality PMP involves sophisticated lamination processes under controlled conditions, requiring significant capital investment. The precise treatment of paper layers and exacting lamination standards elevate production costs approximately 25-35% above conventional insulation materials. Achieving consistent thickness tolerances and dielectric properties across production batches remains challenging, with quality variations affecting nearly 20% of output, creating barriers for price-sensitive applications.

- Raw Material Price Volatility and Supply Chain Constraints: The PMP market faces significant pressure from fluctuating prices of key raw materials, including specialty electrical grades of paper and polyester films. Petroleum price volatility directly impacts polyester production costs, while paper pulp prices fluctuate based on agricultural and forestry market conditions. These cost variations, combined with complex global supply chains, create pricing instability that can deter potential users from committing to long-term adoption strategies.

Critical Market Challenges Requiring Innovation

The transition from established laboratory formulations to industrial-scale production presents unique challenges that demand continuous innovation.

Maintaining material consistency at commercial production volumes proves particularly difficult, with current manufacturing processes achieving only 70-80% yield of specification-grade material. The precision required in layer thickness and bonding integrity means that even minor deviations can render entire production runs unsuitable for high-voltage applications. Furthermore, ensuring long-term performance stability under varying environmental conditions requires extensive testing and quality control measures that add significantly to overall costs.

Additionally, the market contends with increasingly stringent international standards and certification requirements. Compliance with standards such as IEC, UL, and other regional specifications requires substantial investment in testing and quality assurance systems. These regulatory hurdles, while necessary for ensuring safety and performance, can delay product introductions and increase development costs, particularly for smaller manufacturers seeking to enter new geographic markets.

Vast Market Opportunities on the Horizon

- Emerging Applications in High-Frequency Electronics: While traditionally used in power applications, PMP is finding new opportunities in high-frequency electronics. The material's consistent dielectric properties make it suitable for certain radio frequency applications, particularly where traditional materials face limitations. This expansion into new technological areas represents a significant growth frontier beyond its traditional power applications.

- Advanced Composite Development: Research into enhanced PMP variants with improved thermal performance and flame retardancy opens new possibilities in extreme environment applications. Developments in nano-coated papers and advanced polyester films are creating PMP grades that can operate at temperatures 20-30°C higher than standard versions, making them suitable for next-generation power equipment and aerospace applications.

- Strategic Partnerships and Vertical Integration: The market is witnessing increased collaboration between PMP manufacturers and end-users to develop application-specific solutions. These partnerships are crucial for bridging the gap between material capabilities and application requirements, effectively reducing development time and ensuring that new PMP formulations meet exact customer needs. Such collaborations also help stabilize supply chains and create more predictable demand patterns.

In-Depth Segment Analysis: Where is the Growth Concentrated?

By Type:

The market is segmented primarily by thickness, with Thickness > 0.08 mm and Thickness ≤ 0.08 mm being the main categories. The thicker variant currently dominates the market, favored for its superior dielectric strength and mechanical durability in high-voltage applications. This segment's growth is particularly strong in power transmission and distribution equipment where insulation performance is critical. The thinner segment finds its niche in applications where space constraints are paramount, though it requires more precise manufacturing processes.

By Application:

Application segments include Casting Type Voltage Transformers, Motors, and Other applications. The Motor application segment represents the largest and most consistent demand driver, leveraging PMP's excellent thermal stability and electrical tracking resistance for motor winding insulation. The ongoing global expansion of industrial automation and electric vehicle production continues to fuel growth in this segment. The Casting Type Voltage Transformer segment follows closely, driven by grid modernization projects worldwide.

By End-User Industry:

The end-user landscape encompasses Electrical Equipment Manufacturing, Automotive, Power Generation, and other industrial sectors. Electrical Equipment Manufacturers constitute the core consumer base, utilizing PMP in transformers, generators, and switchgear. The automotive sector, particularly electric vehicle manufacturing, is emerging as a significant growth area, while power generation utilities represent steady demand for maintenance and expansion projects.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/304457/papermylarpaper-market

Competitive Landscape:

The global Paper-Mylar-Paper market is characterized by a fragmented competitive landscape with several specialized manufacturers, predominantly based in China. The market features moderate concentration, with the top five players holding a significant portion of market share. Competition primarily revolves around product quality, technical specifications, and price competitiveness, with manufacturers continuously investing in R&D to improve material performance and production efficiency.

List of Key Paper-Mylar-Paper Companies Profiled:

- Nantong Zhongling Electric Power Technology (China)

- Xujue Electrical (China)

- Henan Yuguan Electrical Material (China)

- Taizhou Zhengda Insulation Materials (China)

- Xuchang Xinda Insulation Materials (China)

- Shenyang Youda Insulation Materials (China)

- Henan Ya'an Electric Insulation (China)

- Xuchang Zhongjue Insulation Material (China)

- Mianyang Guoshun Electrical (China)

- Taizhou Jiangyan Guanghua Electrical Materials (China)

The competitive strategy focuses heavily on technological innovation, with companies investing in advanced lamination technologies and quality control systems. Additionally, forming strategic partnerships with end-users has become crucial for developing application-specific solutions and securing long-term supply agreements. Chinese manufacturers particularly benefit from locally integrated supply chains and government support for electrical materials manufacturing.

Regional Analysis: A Global Footprint with Distinct Leaders

- Asia-Pacific: Dominates the global market, holding approximately 65% share of total consumption. China stands as both the largest producer and consumer, driven by its massive electrical equipment manufacturing sector and ongoing infrastructure development. The region's advantage stems from integrated supply chains, competitive manufacturing capabilities, and strong government support for electrical infrastructure projects. Other Asian countries, particularly India and Southeast Asian nations, are emerging as significant growth markets as they expand their power infrastructure.

- Europe and North America: Together account for approximately 30% of the global market. These regions represent mature markets characterized by demand for high-quality, specification-grade PMP products. Market growth in these regions is driven primarily by infrastructure modernization, renewable energy projects, and replacement demand. Strict quality standards and certification requirements in these markets create barriers to entry but also opportunities for premium, high-performance products.

- Rest of World: Includes South America, Middle East, and Africa, representing emerging markets with significant growth potential. These regions are characterized by increasing electrification rates and infrastructure development projects. While currently smaller in market size, they present long-term growth opportunities as industrial development accelerates and power infrastructure expands to meet growing demand.

Get Full Report Here: https://www.24chemicalresearch.com/reports/304457/papermylarpaper-market

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/304457/papermylarpaper-market

About 24chemicalresearch

Founded in 2015, 24chemicalresearch has rapidly established itself as a leader in chemical market intelligence, serving clients including over 30 Fortune 500 companies. We provide data-driven insights through rigorous research methodologies, addressing key industry factors such as government policy, emerging technologies, and competitive landscapes.

- Plant-level capacity tracking

- Real-time price monitoring

- Techno-economic feasibility studies

International: +1(332) 2424 294 | Asia: +91 9169162030

Website: https://www.24chemicalresearch.com/