Automotive Lightweight Materials Market: Trends, Drivers, and Competitive Analysis

Market Size

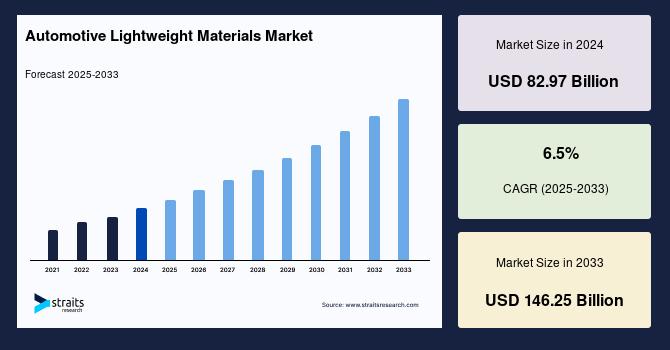

The global automotive lightweight materials market size was valued at USD 82.97 billion in 2024.

It is expected to grow from USD 88.37 billion in 2025 to reach USD 146.25 billion by 2033, growing at a CAGR of 6.5% during the forecast period (2025-2033).

Get Full Report Now: https://straitsresearch.com/report/automotive-lightweight-materials-market

Get Your Sample Report Here: https://straitsresearch.com/report/automotive-lightweight-materials-market/request-sample

Introduction

Automotive lightweight materials are designed to reduce vehicle weight, improve fuel efficiency, and enhance overall vehicle performance. These materials include advanced metals, polymers, composites, and hybrid solutions, which help manufacturers meet stringent emission regulations while improving driving efficiency and safety.

The increasing demand for electric vehicles, fuel-efficient passenger cars, and commercial vehicles is a significant driver for the adoption of lightweight materials. Additionally, automotive OEMs are investing in innovative materials and manufacturing processes to reduce vehicle weight without compromising structural integrity.

Market Drivers

Regulatory Pressure for Fuel Efficiency

Governments worldwide are enforcing stricter fuel efficiency and emission standards. Lightweight materials reduce vehicle mass, improving fuel efficiency and reducing CO2 emissions.

Growth in Electric Vehicle Production

The rise in electric vehicle production is driving the demand for lightweight materials, as reduced weight directly improves battery efficiency and driving range.

Rising Demand for Performance Vehicles

Sports cars, luxury vehicles, and high-performance commercial vehicles increasingly utilize lightweight materials to enhance speed, handling, and efficiency.

Technological Advancements

New lightweight alloys, composite materials, and polymer blends provide superior strength-to-weight ratios, corrosion resistance, and design flexibility, fueling market growth.

Cost Reduction and Sustainability Goals

Automakers are adopting lightweight materials to meet sustainability goals while reducing operational costs related to fuel consumption. Advanced manufacturing processes and recycling methods further support market adoption.

Market Challenges

High Material Costs

Some lightweight materials, especially advanced composites and high-strength alloys, are costlier than traditional steel, which may limit widespread adoption.

Manufacturing Complexities

Integration of lightweight materials into existing manufacturing processes can be complex and may require significant investment in technology and training.

Limited Supplier Base

Certain advanced materials are supplied by a few specialized manufacturers, potentially creating supply chain risks and cost volatility.

Recycling and End-of-Life Concerns

Recycling composite and hybrid materials is challenging, which could impact sustainability targets and regulatory compliance.

Market Segmentation

By Material Type

Aluminum

Aluminum is extensively used due to its excellent strength-to-weight ratio, corrosion resistance, and recyclability. It is primarily applied in body panels, engine components, and chassis parts.

Magnesium

Magnesium alloys are lightweight and offer high structural performance, ideal for engine blocks, transmission cases, and wheels.

Composites

Composites, including carbon fiber-reinforced polymers, are used in high-performance vehicles for weight reduction and structural rigidity.

High-Strength Steel

High-strength steel provides lightweight benefits while maintaining durability and cost efficiency, especially in safety-critical components.

Polymers and Plastics

Polymers are widely applied in interior and exterior components, offering weight reduction, design flexibility, and cost-effectiveness.

By Vehicle Type

Passenger Cars

Passenger vehicles are increasingly adopting lightweight materials to improve fuel efficiency, safety, and driving performance.

Commercial Vehicles

Lightweight materials in trucks and buses reduce fuel consumption and increase payload capacity, addressing operational efficiency.

Electric Vehicles

EV manufacturers are heavily investing in lightweight materials to maximize battery range and performance while complying with emission targets.

By Region

North America

North America leads in lightweight material adoption due to stringent fuel efficiency standards, advanced manufacturing, and EV growth.

Europe

Europe shows strong growth due to emission regulations, automotive innovation, and demand for electric and hybrid vehicles.

Asia-Pacific

Asia-Pacific is the fastest-growing market, driven by automotive production expansion, increasing EV adoption, and government incentives in China, India, and Japan.

Rest of the World

Other regions are gradually adopting lightweight materials, particularly in commercial vehicle and high-performance vehicle segments.

Top Players Analysis

The automotive lightweight materials market is highly competitive, with companies focusing on material innovation, collaborations, and strategic expansions.

- Alcoa Corporation

- Arconic Inc.

- Novelis Inc.

- Norsk Hydro ASA

- UACJ Corporation

- SGL Carbon SE

- Toray Industries Inc.

- BASF SE

- SABIC

- Teijin Limited

These companies invest in R&D for lightweight alloys, composites, and polymers. They also expand production facilities and global distribution networks to meet rising demand.

Conclusion

The automotive lightweight materials market is set to witness strong growth, fueled by the rising adoption of electric vehicles, regulatory pressures, and demand for fuel-efficient and high-performance vehicles.

Despite challenges such as high costs, manufacturing complexity, and recycling issues, innovations in materials, manufacturing techniques, and strategic collaborations among key players will drive market expansion.

FAQs

What are automotive lightweight materials?

Automotive lightweight materials include metals, composites, polymers, and alloys designed to reduce vehicle weight, enhance fuel efficiency, and maintain performance.

What drives the automotive lightweight materials market?

The market is driven by fuel efficiency regulations, EV adoption, performance vehicle demand, technological advancements, and sustainability initiatives.

What are the key challenges in this market?

High costs, manufacturing complexity, limited suppliers, and recycling difficulties pose challenges for market growth.

Which regions are leading the adoption of automotive lightweight materials?

North America and Europe lead due to regulations and automotive innovation, while Asia-Pacific is the fastest-growing region.

Who are the top companies in the automotive lightweight materials market?

Alcoa Corporation, Arconic, Novelis, Norsk Hydro, and Toray Industries are some of the leading players driving innovation and global expansion.

About Us:

Straits Research is a leading research and intelligence organisation, specialising in research, analytics, and advisory services, along with providing business insights & research reports.

Contact Us:

Email: sales@straitsresearch.com

Tel: +1 646 905 0080 (U.S.), +44 203 695 0070 (U.K.)