Pantograph Bus Charger Market Overview

The pantograph bus charger market is witnessing strong expansion due to rapid electrification of public transportation systems and increasing government initiatives to reduce urban emissions. These systems are becoming a backbone of modern electric bus infrastructure because they enable automated, high-power, and fast charging for large fleets operating under strict schedules. According to Redline Pulse, the growing adoption of electric buses and smart city projects is accelerating demand for standardized and efficient charging systems.

Get Your Sample Report Here: https://www.redlinepulse.com/report/pantograph-bus-charger-market/request-sample

Pantograph Bus Charger Market Size

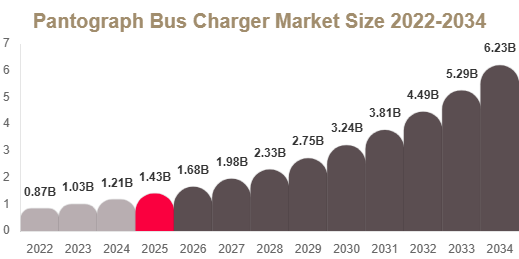

Market Size in 2025: USD 1.42 Billion

Market Size in 2026: USD 1.68 Billion

CAGR (2025–2034): 17.8%

Market Size in 2034: USD 6.35 Billion

The market is expanding rapidly due to large-scale electric bus deployment, increasing investments in fast-charging infrastructure, and government-led decarbonization programs.

Key Market Insights

Europe dominated the market with 38.92% share in 2025.

Asia Pacific is expected to be the fastest-growing region with a CAGR of 19.4%.

Automated inverted pantograph systems held 57.16% share in 2025.

Depot charging segment dominated with 62.48% share in 2025.

Bus fleet operators accounted for 68.25% share in 2025.

High-power charging systems (>300 kW) held 49.37% share in 2025.

The U.S. market was valued at USD 0.46 billion in 2025 and reached USD 0.58 billion in 2026.

Market Trends

Expansion of High-Power Automated Charging Infrastructure

A major trend is the rapid deployment of high-power pantograph charging systems across urban transit networks. These systems allow electric buses to charge quickly during short stops or depot operations, significantly reducing downtime and improving fleet efficiency. Cities are adopting route-based charging models to optimize energy usage and operational schedules.

Integration of Smart Grid and Digital Monitoring Systems

Another key trend is the integration of pantograph chargers with smart grid infrastructure and IoT-enabled monitoring systems. These systems enable real-time energy tracking, predictive maintenance, and load balancing. This improves efficiency while reducing operational costs for transit authorities and fleet operators.

Market Drivers

Government-Led Electrification of Public Transport

A major driver of the pantograph bus charger market is strong government support for electrifying public transportation fleets. Policies aimed at reducing emissions and phasing out diesel buses are accelerating adoption. Subsidies and infrastructure funding are encouraging transit operators to invest in electric bus ecosystems supported by pantograph charging systems.

Rising Demand for Fast and Automated Charging Systems

The need for fast and efficient charging solutions is increasing as urban transit systems operate on strict schedules. Pantograph chargers enable automated high-speed charging, reducing operational delays and improving fleet productivity. This makes them highly suitable for large-scale bus operations.

Market Restraints

High Installation and Infrastructure Costs

A key restraint is the high cost associated with installing pantograph charging infrastructure. These systems require significant investment in overhead structures, grid upgrades, and power distribution systems.

Additionally, compatibility issues between bus models and charging standards increase implementation complexity. These factors slow adoption, especially in developing economies with limited public transport budgets.

Market Opportunities

Expansion of Electric Bus Fleets in Emerging Economies

Emerging economies present strong growth opportunities due to increasing investments in electric bus deployment. Governments in Asia Pacific, Latin America, and Africa are expanding public transport electrification programs to reduce pollution and improve urban mobility. Pantograph systems are well-suited for large-scale fleet operations, making them a preferred choice for centralized charging infrastructure.

Development of Ultra-Fast and Wireless Pantograph Systems

Technological advancements in ultra-fast and semi-wireless pantograph charging systems are creating new opportunities. Innovations in automated alignment and higher power transfer efficiency are improving performance and reducing mechanical wear. These developments are expected to make pantograph systems more scalable and cost-effective.

Segmental Analysis

By Charging Type

Inverted Pantograph Systems

Inverted pantograph systems dominated with 57.16% share in 2024. These systems are widely used in depot charging due to their high reliability and efficient energy transfer capabilities.

Reversible Pantograph Systems

Reversible pantograph systems are expected to grow at a CAGR of 18.6%. Their flexibility and compatibility with multiple bus models make them ideal for evolving smart city infrastructure.

By Application

Depot Charging

Depot charging held 62.48% share in 2024 due to centralized overnight charging efficiency and better energy management.

Opportunity Charging

Opportunity charging is expected to grow at a CAGR of 19.2% due to increasing installation of in-route charging stations.

By End User

Bus Fleet Operators

Bus fleet operators dominated with 68.25% share in 2024 due to large-scale deployment of electric buses in public transport systems.

Municipal Transport Authorities

Municipal transport authorities are expected to grow at a CAGR of 18.9% due to government-led electrification initiatives.

Regional Analysis

North America

North America accounted for 21.34% share in 2025 and is projected to grow at a CAGR of 15.9%. The region is investing heavily in electric public transport infrastructure. The U.S. leads due to federal funding programs supporting zero-emission bus adoption.

Europe

Europe held 38.92% share in 2025 and is expected to grow at a CAGR of 16.8%. Strict emission regulations and strong government support make it the global leader in pantograph charging adoption. Germany leads due to advanced transit infrastructure.

Asia Pacific

Asia Pacific accounted for 29.47% share in 2025 and is expected to grow at the fastest CAGR of 19.4%. China dominates due to large-scale electric bus deployment and strong government investment in smart transportation systems.

Middle East & Africa

The region held 5.12% share in 2025 and is expected to grow at a CAGR of 14.6%. Growth is driven by smart city initiatives and investment in clean transport systems, with the UAE leading adoption.

Latin America

Latin America accounted for 5.15% share in 2025 and is projected to grow at a CAGR of 15.2%. Brazil leads due to rising investment in electric bus pilot programs and urban mobility projects.

Competitive Landscape

The pantograph bus charger market is moderately consolidated, with companies focusing on high-power charging systems, smart grid integration, and global expansion. ABB is a leading player offering advanced automated charging systems for electric bus fleets. The company continues to innovate in ultra-fast charging solutions for urban transit networks.

Top Players Analysis

- ABB

A global leader in electric mobility charging solutions, focusing on automated pantograph systems for high-speed bus charging. - Siemens AG

Provides integrated charging infrastructure and smart energy management systems for electric transport networks. - Alstom SA

Specializes in sustainable mobility solutions, including electrified public transport charging systems. - Siemens Mobility

Focuses on advanced transit charging infrastructure and digital mobility solutions. - Heliox

Develops fast-charging systems designed specifically for electric bus fleets. - Schunk Group

Provides pantograph contact systems and charging interface technologies. - Hitachi Energy

Offers grid integration and high-power charging solutions for public transport systems. - Tritium Charging

Specializes in fast-charging technology for electric mobility applications. - Proterra Inc.

Focuses on electric bus systems and integrated charging infrastructure solutions. - ABB E-Mobility

Dedicated division for advanced EV charging technologies including pantograph systems. - ChargePoint Holdings

Provides large-scale EV charging network solutions. - EVBox Group

Offers scalable charging infrastructure for electric mobility ecosystems. - Delta Electronics

Focuses on power electronics and EV charging systems. - Yutong Bus Co.

Major electric bus manufacturer supporting integrated charging ecosystem development. - BYD Company Ltd.

Leading EV manufacturer with strong presence in electric bus and charging infrastructure integration.

Conclusion

The pantograph bus charger market is set for rapid expansion driven by global electrification of public transport, smart city initiatives, and rising demand for high-speed automated charging systems. While high infrastructure costs remain a challenge, technological advancements and government support are expected to significantly accelerate adoption over the forecast period.

Get More Details: https://www.redlinepulse.com/report/pantograph-bus-charger-market

Buy Now: https://www.redlinepulse.com/report/pantograph-bus-charger-market/buy-now