Automotive Alternator Market Overview

The automotive alternator market is an essential part of modern vehicle electrical architecture, responsible for converting mechanical energy into electrical energy to power onboard systems and recharge batteries. With increasing vehicle electrification and rising demand for advanced electronic features, alternators have become more critical than ever in maintaining stable power supply across automotive platforms. According to Redline Pulse, the growing complexity of vehicle electrical systems is directly influencing demand for high-output and smart alternator solutions.

Get Your Sample Report Here: https://www.redlinepulse.com/report/automotive-alternator-market/request-sample

Automotive Alternator Market Size

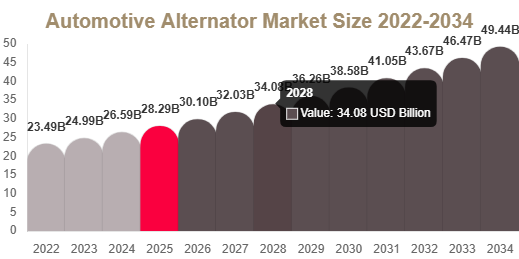

Market Size in 2025: USD 28.4 Billion

Market Size in 2026: USD 30.1 Billion

CAGR (2025–2034): 6.4%

Market Size in 2034: USD 49.6 Billion

The market expansion is driven by rising global vehicle production, increasing adoption of electronic systems, and growing demand for efficient power generation solutions in modern vehicles.

Key Market Insights

Asia Pacific dominated the market with 44.12% share in 2025.

Europe is expected to be the fastest-growing region with a CAGR of 6.9%.

Passenger vehicles accounted for 58.36% share in 2025.

Belt-driven alternators held 71.48% share in 2025.

OEM segment dominated with 78.25% share in 2025.

12V alternators contributed 64.91% share in 2025.

The U.S. market was valued at USD 8.9 billion in 2025 and reached USD 9.5 billion in 2026.

Market Trends

Increasing Adoption of High-Efficiency and Smart Alternators

A key trend in the automotive alternator market is the shift toward high-efficiency and smart alternators designed to manage increasing electrical loads in modern vehicles. These alternators improve energy efficiency, reduce fuel consumption, and support advanced electronic systems such as ADAS, infotainment, and connectivity modules. Smart alternators with voltage regulation capabilities are increasingly used in start-stop vehicles to optimize battery charging based on real-time operating conditions.

Shift Toward Electrification-Compatible Alternator Systems

Another major trend is the development of alternators compatible with hybrid and mild-hybrid vehicles. These systems include integrated starter-generator technologies that combine alternator and starter functions. This improves fuel efficiency and enables regenerative energy recovery, making them essential for electrified powertrain architectures.

Market Drivers

Rising Vehicle Production and Electrification of Automotive Systems

The growth in global vehicle production is a major driver of the alternator market. Increasing demand for passenger and commercial vehicles is boosting alternator installations worldwide. Modern vehicles require higher electrical output due to the integration of infotainment systems, ADAS, and electronic control units, increasing reliance on efficient alternators.

Increasing Adoption of Start-Stop and Hybrid Technologies

The rising adoption of start-stop systems and hybrid vehicles is significantly driving demand for advanced alternators. Start-stop systems require alternators capable of frequent engine restarts, while hybrid vehicles need high-output systems to manage dual power sources efficiently. Regulatory pressure on emissions is further accelerating this trend.

Market Restraints

Rising Shift Toward Fully Electric Vehicles

A key restraint is the growing adoption of fully electric vehicles, which do not require traditional alternators. EVs rely on battery packs and power electronics for energy management, reducing dependency on mechanical energy conversion systems.

This transition is creating long-term challenges for alternator manufacturers, pushing them to invest in EV-compatible technologies such as electric motor generators and advanced power electronics. However, this shift requires significant R&D investment and production restructuring.

Market Opportunities

Development of Smart Charging Alternators

A major opportunity lies in smart charging alternators that dynamically adjust output based on vehicle load conditions. These systems improve fuel efficiency, extend battery life, and enhance energy management in connected and autonomous vehicles.

Manufacturers investing in intelligent alternator systems are likely to benefit from strong OEM partnerships, especially in premium and mid-range vehicle segments where efficiency and performance are key priorities.

Expansion of Hybrid and Mild-Hybrid Platforms

The rapid expansion of hybrid and mild-hybrid vehicles presents a strong growth opportunity. These vehicles still rely on alternators for auxiliary power functions, making them a critical component in electrified powertrains.

Demand is particularly strong in Europe and Asia Pacific, where strict emission regulations are accelerating hybrid adoption. Compact, high-output alternators are increasingly being integrated into modern hybrid architectures.

Segmental Analysis

By Voltage Type

12V Alternators

12V alternators dominated with 64.91% share in 2024 due to their widespread use in passenger vehicles and compatibility with conventional automotive systems.

48V Alternators

48V alternators are expected to grow at a CAGR of 7.8% due to increasing adoption in mild-hybrid vehicles, offering improved efficiency and higher electrical load capacity.

By Vehicle Type

Passenger Vehicles

Passenger vehicles held 58.36% share in 2024 due to high production volumes and strong consumer demand for electronic features.

Commercial Vehicles

Commercial vehicles are expected to grow at a CAGR of 6.7% driven by logistics expansion and fleet electrification.

By Technology

Belt-Driven Alternators

Belt-driven alternators dominated with 71.48% share in 2024 due to cost efficiency and widespread use in conventional vehicles.

Integrated Starter Generators

Integrated starter generators are expected to grow at a CAGR of 8.3% due to increasing hybrid vehicle adoption and efficiency improvements.

Regional Analysis

North America

North America held 21.36% share in 2025 and is projected to grow at a CAGR of 6.1%. Strong automotive production and rising adoption of start-stop systems support growth. The U.S. leads due to high demand for SUVs and light trucks.

Europe

Europe accounted for 26.48% share in 2025 and is expected to grow at a CAGR of 6.9%. Strict emission regulations and strong hybrid vehicle adoption are key drivers. Germany leads due to its advanced automotive engineering ecosystem.

Asia Pacific

Asia Pacific dominated with 44.12% share in 2025 and is expected to grow at a CAGR of 6.6%. China leads due to large-scale automotive production and rising demand for cost-efficient vehicles.

Middle East & Africa

The region held 4.2% share in 2025 and is projected to grow at a CAGR of 5.8%. Infrastructure development and increasing vehicle imports are supporting growth.

Latin America

Latin America accounted for 3.8% share in 2025 and is expected to grow at a CAGR of 6.0%. Brazil leads due to strong automotive assembly and increasing passenger vehicle demand.

Competitive Landscape

The automotive alternator market is moderately consolidated, with companies focusing on efficiency improvements, lightweight designs, and hybrid-compatible solutions. Bosch is a leading player, offering advanced alternator systems for conventional and start-stop vehicles and expanding its high-efficiency product portfolio.

Top Players Analysis

- Bosch

A global leader in automotive electrical systems, focusing on high-efficiency alternators and start-stop compatible technologies. - Denso Corporation

Specializes in advanced alternator systems designed for fuel efficiency and hybrid vehicle applications. - Valeo

Focuses on smart alternators and electrification-ready automotive components. - Mitsubishi Electric Corporation

Develops high-performance alternators and integrated automotive electrical systems. - Hitachi Astemo

Provides advanced powertrain and alternator solutions for modern vehicles. - Delphi Technologies

Focuses on efficient alternator systems and electrified mobility components. - Mahle GmbH

Specializes in engine and electrical system components for automotive applications. - Hella GmbH

Develops intelligent energy management and alternator solutions. - Robert Bosch Automotive Steering

Expands integrated vehicle electrical and steering systems. - Lucas Electrical

Known for durable alternator solutions across vehicle segments. - Prestolite Electric

Provides heavy-duty alternators for commercial vehicles. - Nidec Corporation

Focuses on high-efficiency electric motor and alternator systems. - Remy International

Specializes in remanufactured and OEM alternator solutions. - Motorcraft

Offers reliable automotive electrical components and alternators. - Hengst SE

Provides filtration and automotive system components supporting electrical efficiency.

Conclusion

The automotive alternator market is set for steady long-term growth driven by rising vehicle production, increasing electronic load requirements, and the expansion of hybrid vehicle platforms. While the shift toward full electrification poses a structural challenge, innovation in smart alternators and hybrid-compatible systems is expected to sustain market relevance and growth.

Get More Details: https://www.redlinepulse.com/report/automotive-alternator-market

Buy Now: https://www.redlinepulse.com/report/automotive-alternator-market/buy-now