The rotorcraft industry is currently navigating a pivotal era where performance meets precision engineering. As we look toward the next decade, the tail rotor gearbox remains a cornerstone of helicopter stability and safety. This Aircraft Tail Rotor Gearbox Market Analysis explores the technological shifts and economic tailwinds that are steering the industry toward unprecedented growth.

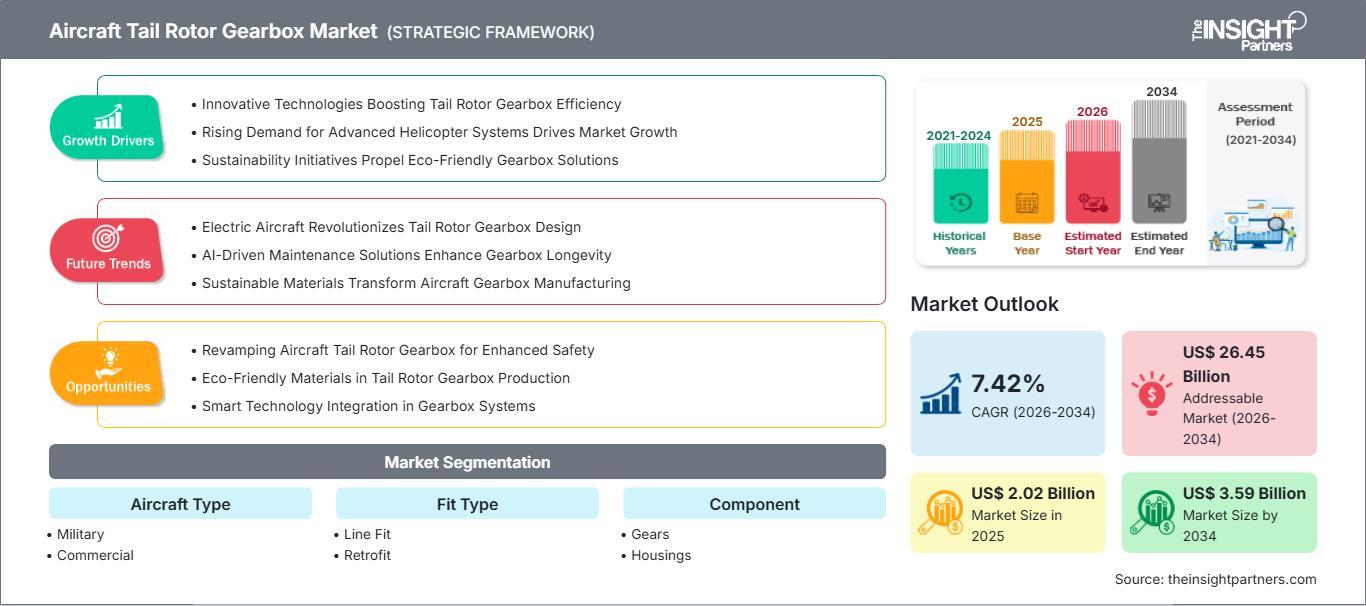

The global Aircraft Tail Rotor Gearbox Market size is projected to reach US$ 3.59 billion by 2034 from US$ 2.02 billion in 2025. The market is anticipated to register a CAGR of 7.42% during the forecast period 2026-2034. This steady climb reflects a broader global commitment to enhancing aerial capabilities in both defense and civil sectors.

Download Sample Report –

https://www.theinsightpartners.com/Sample/TIPRE00019081

Core Drivers of the Market

Several critical factors are propelling the demand for advanced tail rotor gearboxes. Understanding these drivers is essential for stakeholders looking to capitalize on upcoming opportunities:

- Modernization of Military Fleets: Defense agencies are increasingly focused on replacing "legacy" platforms with high-speed, high-maneuverability rotorcraft. These new designs require gearboxes that can manage higher torque and thermal loads while maintaining a compact footprint.

- Expansion of Urban Air Mobility (UAM): The rise of eVTOL (electric Vertical Take-off and Landing) aircraft is introducing new requirements for propulsion systems. While many are distributed, those utilizing traditional anti-torque mechanisms are driving innovation in electric and hybrid gearbox configurations.

- Material Science Breakthroughs: The integration of lightweight alloys and composite housings is no longer a luxury but a necessity. By reducing the overall weight of the gearbox, manufacturers help operators achieve better fuel efficiency and higher payload capacities.

- Predictive Maintenance (HUMS): Health and Usage Monitoring Systems (HUMS) are being integrated directly into gearbox designs. This allow for real-time vibration and temperature analysis, shifting the industry from scheduled maintenance to a more cost-effective condition-based approach.

Top Market Players

The competitive landscape is defined by long-standing aerospace leaders and specialized precision engineering firms:

- Airbus Helicopters

- Leonardo S.p.A.

- Bell Textron Inc.

- Sikorsky (Lockheed Martin)

- Safran S.A.

- Triumph Group

- ZF Luftfahrttechnik

- The Boeing Company

Regional Strategic Shifts

While North America continues to lead in terms of military expenditure and fleet size, the Asia-Pacific region is emerging as the fastest-growing market. Rapid investment in healthcare infrastructure is fueling a surge in Air Ambulance and Emergency Medical Services (EMS), all of which rely on the high-frequency reliability of modern tail rotor systems.

Industry Note: The transition toward "dry-run" capable gearboxes is becoming a major procurement standard for naval and combat helicopters, ensuring that aircraft can remain airborne for at least 30 minutes following a total loss of lubrication.

As we move deeper into the 2030s, the focus on sustainability and noise reduction will likely lead to further refinements in gear tooth geometry and lubrication chemistry. For manufacturers and investors, the tail rotor gearbox market represents a high-stakes arena where reliability is the ultimate currency.

Contact Information -

Email: sales@theinsightpartners.com

Phone: +1-646-491-9876

Also Available in :