The ECU Software Market represents a critical segment of the automotive electronics ecosystem, driven by increasing vehicle electrification, rising adoption of ADAS systems, and the shift toward software-defined vehicles. Modern vehicles rely heavily on electronic control units (ECUs), and the software layer inside these systems is becoming increasingly complex and essential for vehicle performance, safety, and connectivity.

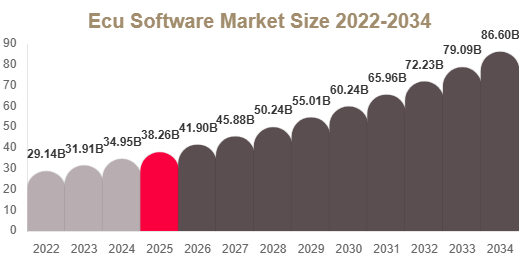

The ECU Software Market was valued at USD 44.01 Billion in 2025 and is projected to reach USD 87.29 Billion by 2034, expanding at a CAGR of 7.91% during the forecast period.

Get Your Sample Report Here: https://www.redlinepulse.com/report/ecu-software-market/request-sample

The expansion is primarily driven by growing integration of advanced driver-assistance systems, infotainment platforms, and powertrain control systems across passenger and commercial vehicles.

Market Drivers

Rising adoption of ADAS and safety systems

The growing focus on road safety regulations and consumer demand for advanced safety features is accelerating ECU software deployment. ADAS applications such as collision avoidance, lane assist, and adaptive cruise control require highly reliable ECU software integration.

Growth of electric and hybrid vehicles

The transition toward electric mobility is increasing the number of ECUs per vehicle, particularly for battery management, motor control, and energy optimization systems. This is significantly boosting demand for advanced ECU software platforms.

Shift toward centralized and software-defined vehicles

Automakers are transitioning from distributed ECU architectures to centralized computing systems. This shift is increasing reliance on middleware and virtualization layers to manage multiple vehicle functions efficiently.

Expansion of connected and infotainment systems

Consumer demand for connected car experiences, infotainment systems, and over-the-air updates is driving continuous ECU software upgrades and lifecycle management solutions.

Market Challenges

High complexity in software integration

ECU software must interact across multiple vehicle systems such as powertrain, chassis, and infotainment. This cross-domain integration increases development complexity and testing requirements.

Long validation and compliance cycles

Safety-critical systems require extensive validation under standards like ISO 26262. This increases development timelines and slows down product deployment.

Cybersecurity and regulatory pressure

Increasing cybersecurity threats and regulatory frameworks require continuous monitoring, secure coding practices, and compliance management, adding to development costs.

Fragmentation across OEM and supplier ecosystems

Different suppliers use varying software architectures and communication protocols, creating compatibility issues and slowing down standardization across the industry.

Market Segments

By Application

Powertrain Systems

This segment dominates ECU software demand due to its critical role in engine control, fuel efficiency, and emission regulation compliance.

Body Control and Comfort Systems

Includes functions such as lighting, climate control, and door systems, enhancing vehicle comfort and user experience.

Infotainment Communication Systems

Driven by consumer demand for connectivity, navigation, and digital cockpit experiences.

ADAS Safety Systems

The fastest-growing segment, supported by increasing demand for autonomous and semi-autonomous driving features.

By Deployment Type

On-Premise ECU Software

Traditionally used for embedded vehicle systems requiring high reliability and real-time control.

Cloud-Based ECU Software

Rapidly expanding due to OTA updates, remote diagnostics, and vehicle data analytics capabilities.

By Vehicle Type

Passenger Vehicles

Largest segment due to high production volumes and increasing adoption of connected features.

Commercial Vehicles

Driven by fleet management, logistics optimization, and regulatory compliance requirements.

Electric Vehicles

Fastest-growing segment due to high ECU density and advanced software requirements.

Top Players Analysis

1. Robert Bosch GmbH

A global leader in automotive electronics, Bosch provides advanced ECU software solutions integrated with ADAS, powertrain, and safety systems. The company focuses heavily on centralized vehicle architecture and software platforms.

2. Continental AG

Continental develops ECU software solutions for braking systems, powertrain control, and automated driving technologies. The company is strongly invested in modular software platforms and cybersecurity solutions.

3. Denso Corporation

Denso specializes in ECU software for engine management, hybrid systems, and vehicle control systems. It plays a key role in electrification-focused ECU software development.

4. Aptiv PLC

Aptiv focuses on software-defined vehicle architecture, offering scalable ECU software platforms for autonomous driving and connected mobility systems.

5. NXP Semiconductors

NXP provides embedded ECU software solutions with strong focus on secure connectivity, vehicle networking, and automotive microcontrollers.

6. Infineon Technologies AG

Infineon delivers ECU software supporting powertrain efficiency, EV control systems, and automotive cybersecurity integration.

7. Renesas Electronics Corporation

Renesas specializes in ECU software platforms optimized for hybrid vehicles, infotainment systems, and advanced control units.

8. Harman International

Harman focuses on infotainment ECU software, connected vehicle platforms, and digital cockpit solutions integrated with AI-based services.

9. Magna International Inc.

Magna develops ECU software for vehicle control systems, autonomous driving modules, and integrated mobility solutions.

10. Autoliv Inc.

Autoliv provides ECU software solutions for safety-critical systems including airbags, collision avoidance, and crash detection technologies.

Conclusion

The ECU Software Market is undergoing a major transformation driven by electrification, connectivity, and autonomous driving technologies. As vehicles become more software-dependent, ECU software will play a central role in enabling performance, safety, and intelligence in modern automotive systems. Increasing adoption of ADAS, EV platforms, and centralized architectures will continue to accelerate market expansion through 2034.