Automotive Pneumatic Actuator Market Report Overview

Get Your Sample Report Here: https://www.redlinepulse.com/report/automotive-pneumatic-actuator-market/request-sample

The automotive pneumatic actuator market is expanding steadily due to rising adoption in commercial vehicles, engine systems, HVAC control, and emission management applications. These actuators convert compressed air into mechanical motion and are widely used for reliable and cost-efficient automotive system operations.

Market Size

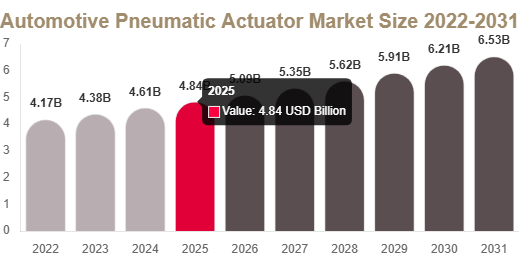

The automotive pneumatic actuator market size was valued at USD 4.82 billion in 2025 and is projected to reach USD 5.09 billion in 2026.

The market is expected to grow to USD 7.96 billion by 2034, registering a CAGR of 5.1% from 2025 to 2034.

According to Redline Pulse analysis, growth is strongly supported by commercial vehicle demand and continued reliance on pneumatic systems in global fleet operations.

Market Trends

Integration with Electronic Control Systems

A major trend is the integration of pneumatic actuators with electronic control systems. Modern vehicles are increasingly using sensors and solenoid-based controls to improve precision and responsiveness in applications such as HVAC systems, turbocharger control, and emission systems.

Compact and Lightweight Designs

Another trend is the demand for compact and lightweight actuator systems. Automakers are focusing on space-efficient designs using advanced sealing materials, corrosion-resistant housings, and miniaturized actuator structures for modern vehicle platforms.

Market Drivers

Strong Demand from Commercial Vehicles

Commercial vehicles are the primary driver of the market. Pneumatic actuators are widely used in braking systems, suspension control, door operations, and air management systems in trucks, buses, and logistics fleets.

Engine and Turbocharger Applications

Pneumatic actuators continue to play an important role in engine control, turbocharger wastegate systems, HVAC airflow regulation, and emission control applications, especially in hybrid and internal combustion vehicles.

Market Challenges and Restraints

Shift Toward Electric Actuation Systems

One of the key restraints is the increasing shift toward electric and electromechanical actuators in passenger vehicles. Electric systems offer higher precision, better integration, and reduced dependency on compressed air systems.

Reduced Use in Modern Vehicle Architectures

Modern vehicle platforms are increasingly integrated and software-driven, reducing the need for pneumatic systems in non-essential applications. This limits long-term growth in some passenger vehicle segments.

Segment Analysis

By Type

Linear Pneumatic Actuators dominate with 57.3% share in 2024 due to wide usage in braking, HVAC systems, seat adjustment, and air suspension applications.

Rotary Pneumatic Actuators are expected to grow at a CAGR of 5.8%, driven by demand for compact motion control in turbochargers and airflow systems.

By Application

Braking Systems hold the largest share at 31.8%, driven by heavy use in commercial vehicles requiring high safety and reliability.

HVAC and Thermal Management Systems are expected to grow fastest at a CAGR of 6.1%, supported by increasing demand for advanced cabin comfort and airflow control.

By Vehicle Type

Commercial Vehicles dominate with 52.4% share due to strong dependency on pneumatic braking and control systems in fleet operations.

Hybrid and Advanced Passenger Vehicles are expected to grow at 5.9% CAGR due to continued use in turbocharged and hybrid vehicle platforms.

Regional Analysis

Asia Pacific

Asia Pacific leads with 35.6% share and is expected to grow at 6.2% CAGR due to strong commercial vehicle production and logistics expansion.

Europe

Europe holds 27.5% share supported by strong truck manufacturing and advanced pneumatic system adoption in Germany and other countries.

North America

North America accounts for 24.3% share driven by heavy-duty trucking fleets and strong aftermarket demand in the United States.

Latin America and Middle East & Africa

These regions show steady growth due to expanding logistics, construction, and commercial transport activities.

Competitive Landscape and Key Players

The market is moderately competitive with a focus on durability, precision control, and integration with electronic systems. Companies are investing in advanced actuator designs for commercial and industrial applications.

- WABCO Holdings Inc. – Leading provider of pneumatic braking and control systems for commercial vehicles.

- Continental AG – Focuses on integrated braking and vehicle motion systems.

- Knorr-Bremse AG – Global leader in braking systems for trucks and buses.

- Robert Bosch GmbH – Offers advanced actuator technologies integrated with engine systems.

- Festo SE & Co. KG – Specializes in pneumatic automation and control systems.

- SMC Corporation – Manufactures compact pneumatic components for automotive use.

- Parker Hannifin Corporation – Provides motion and control solutions for automotive systems.

- Emerson Electric Co. – Delivers automation and pneumatic control technologies.

- NORGREN (IMI plc) – Focuses on precision pneumatic systems for vehicles.

- ZF Friedrichshafen AG – Develops advanced mobility and actuation technologies.

Conclusion

The automotive pneumatic actuator market is expected to grow steadily due to increasing commercial vehicle demand, continued use in engine systems, and integration with modern control technologies. Despite challenges from electrification trends, pneumatic actuators remain essential in heavy-duty automotive applications.