Electric Vehicle Battery Market Report Overview

Get Your Sample Report Here: https://www.redlinepulse.com/report/electric-vehicle-battery-market/request-sample

The electric vehicle battery market is a core pillar of global automotive electrification, driven by rising EV production, expanding charging infrastructure, and strong policy support for zero-emission mobility. These batteries are essential for vehicle range, performance, thermal stability, and cost structure.

Market Size

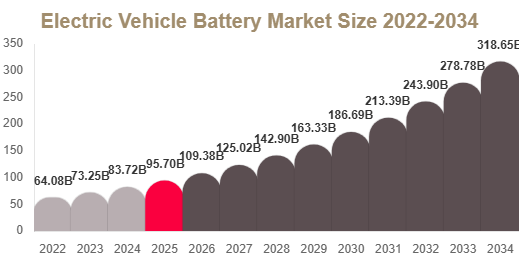

The electric vehicle battery market size was valued at USD 92.64 billion in 2025 and is projected to reach USD 109.38 billion in 2026.

The market is expected to expand to USD 318.57 billion by 2034, registering a CAGR of 14.3% from 2025 to 2034.

According to Redline Pulse analysis, rapid EV adoption and gigafactory expansion are accelerating global battery demand.

Market Trends

Shift Toward Advanced Battery Chemistries

Manufacturers are optimizing lithium-ion chemistries such as LFP, NMC, and LMFP to balance cost, energy density, and performance across mass-market and premium EVs.

Expansion of Local Gigafactories

Battery production is rapidly localizing in North America and Europe to reduce supply chain risk and improve regional manufacturing independence.

Market Drivers

Rapid EV Adoption

Growing global adoption of electric vehicles is the strongest driver of battery demand across passenger cars, buses, and commercial fleets.

Government Policies and Incentives

Strong emission regulations, subsidies, and industrial policies are accelerating EV adoption and battery manufacturing investments worldwide.

Market Challenges and Restraints

Raw Material Price Volatility

Lithium, nickel, cobalt, and graphite price fluctuations significantly impact battery production costs and EV pricing stability.

Supply Chain Dependency

Dependence on critical mineral supply chains creates risks for long-term production scalability and cost control.

Market Opportunities

Battery Recycling and Second-Life Applications

Growing EV adoption creates opportunities for recycling battery materials and repurposing used batteries for energy storage systems.

Electrification of Commercial Fleets

Electric buses, delivery vans, and logistics fleets are creating new demand for durable, high-cycle battery systems.

Segment Analysis

By Battery Chemistry

Lithium-ion batteries dominate with 82.9% share due to high energy density, reliability, and widespread OEM adoption.

Solid-state and next-generation batteries are expected to grow fastest at 21.6% CAGR due to safety and performance advantages.

By Vehicle Type

Battery Electric Vehicles (BEVs) hold 71.3% share, making them the largest demand driver for EV batteries globally.

Electric commercial vehicles are expected to grow fastest at 17.1% CAGR due to fleet electrification trends.

By Battery Form

Prismatic cells dominate with 38.7% share due to efficient packaging and structural integration benefits.

Cell-to-pack and pouch systems are growing fastest at 16.4% CAGR due to improved energy density and lightweight design.

Regional Analysis

Asia Pacific

Asia Pacific leads with 47.6% share and 15.8% CAGR due to strong EV manufacturing and battery supply chain dominance.

North America

North America holds 18.9% share driven by gigafactory expansion and EV production growth in the United States.

Europe

Europe accounts for 24.7% share supported by strong EV adoption and battery manufacturing investments.

Latin America and MEA

These regions are emerging with growing EV adoption, fleet electrification, and early-stage battery infrastructure development.

Competitive Landscape and Key Players

The market is highly competitive with a focus on scale production, chemistry innovation, and supply chain localization. Companies are investing heavily in solid-state research, recycling, and fast-charging technologies.

- Contemporary Amperex Technology Co., Limited (CATL) – Global leader in EV battery manufacturing and chemistry innovation.

- LG Energy Solution – Strong global supplier with advanced lithium-ion battery technologies.

- Panasonic Holdings Corporation – Major supplier focused on high-performance EV battery cells.

- Samsung SDI Co., Ltd. – Known for premium battery solutions and R&D strength.

- BYD Company Ltd. – Integrated EV and battery manufacturer with strong vertical supply chain.

- SK On Co., Ltd. – Expanding global battery production capacity and EV partnerships.

- CALB Group Co., Ltd. – Key Chinese battery manufacturer focusing on scalable EV solutions.

- Gotion High-Tech Co., Ltd. – Emerging leader in lithium-ion battery technologies.

- EVE Energy Co., Ltd. – Strong player in cylindrical and prismatic battery segments.

- Northvolt AB – European battery manufacturer focused on sustainable production.

Conclusion

The electric vehicle battery market is expected to grow significantly due to rising EV adoption, policy support, and rapid advancements in battery technology. Despite raw material challenges, long-term demand remains strong across passenger and commercial electric mobility.