Cylinder Deactivation System Market Research Report

Get Your Sample Report Here: https://www.redlinepulse.com/report/cylinder-deactivation-system-market/request-sample

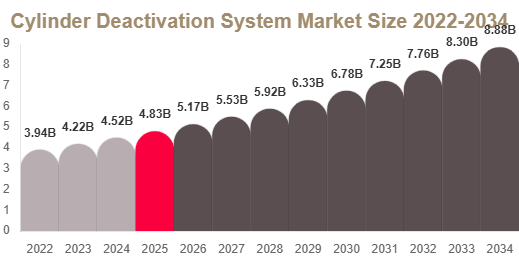

Market Size

The global cylinder deactivation system market size was valued at USD 4.82 billion in 2025 and is estimated to reach USD 5.17 billion in 2026. The market is projected to expand to USD 8.86 billion by 2034, registering a CAGR of 7.0% from 2025 to 2034.

This growth is driven by continued demand for fuel-efficient internal combustion engines, emissions compliance pressure, and optimization of gasoline engine architectures in passenger and commercial vehicles.

Market Overview

Cylinder deactivation technology is becoming an important efficiency solution in modern combustion engines. It allows engines to shut down selected cylinders during low-load conditions, improving fuel economy without compromising performance. This technology is widely adopted in SUVs, sedans, and light commercial vehicles where both power and efficiency are required.

Market Trends

Integration with Hybrid Powertrains

Cylinder deactivation is increasingly integrated with 48V mild hybrid systems, regenerative braking, and advanced transmission controls. This combination improves real-world fuel efficiency and supports smoother driving performance in modern vehicles.

Advancements in Engine Control Systems

Modern systems are supported by advanced software, NVH reduction technologies, and real-time engine calibration. These improvements have reduced vibration and improved customer acceptance across broader vehicle categories.

Market Drivers

Fuel Efficiency Regulations

Increasing global fuel economy standards are pushing automakers to adopt cylinder deactivation systems to reduce fuel consumption in gasoline-powered vehicles, especially in highway driving conditions.

Demand for SUVs and Larger Vehicles

Rising demand for SUVs and pickup trucks is creating strong adoption opportunities. These vehicles benefit significantly from cylinder deactivation as it reduces fuel usage during low-load driving.

Market Challenges

Limited Applicability in Small Engines

Cylinder deactivation is less effective in small displacement engines, limiting adoption in compact vehicle segments. The added system complexity may not justify cost benefits in low-cylinder configurations.

High System Integration Costs

Engineering complexity, calibration requirements, and component integration increase development costs, making it less attractive for low-cost vehicle platforms.

Market Opportunities

Expansion in Four-Cylinder Engines

Advancements in engine control systems are enabling adoption in turbocharged four-cylinder engines, expanding market penetration into high-volume passenger vehicle segments.

Hybrid Powertrain Optimization

Cylinder deactivation is increasingly used in hybrid systems to improve combustion efficiency when electric assistance is inactive, improving overall vehicle efficiency.

Segmental Analysis

By Component

Electronic control units and control software dominate the market due to their role in managing cylinder shutdown logic, fuel injection timing, and real-time engine optimization. Valve actuation systems are growing rapidly due to increasing demand for precision mechanical control.

By Engine Type

V6 engines dominate the market as they provide an optimal balance between performance and efficiency. Inline four-cylinder engines are the fastest-growing segment due to rising turbocharged engine adoption.

By Vehicle Type

Passenger vehicles lead the market due to high production volumes and widespread adoption in SUVs and sedans. Light commercial vehicles are growing due to fleet efficiency requirements.

Regional Analysis

North America

North America dominates due to strong demand for large vehicles such as SUVs and pickup trucks. The U.S. leads adoption driven by fuel efficiency requirements in high-displacement engines.

Europe

Europe shows steady growth supported by emissions regulations and premium vehicle production, with Germany leading adoption in performance-oriented vehicles.

Asia Pacific

Asia Pacific is the fastest-growing region due to high vehicle production, strong automotive manufacturing base, and increasing demand for fuel-efficient vehicles.

Middle East & Africa

Growth is supported by demand for premium SUVs and high-performance vehicles, especially in the UAE and Saudi Arabia.

Latin America

Brazil leads the region with increasing adoption of fuel-efficient technologies in passenger and utility vehicles.

Competitive Landscape

The market is moderately consolidated with strong competition among global automotive suppliers and engine technology providers. Companies are focusing on improving efficiency, reducing emissions, and enhancing engine control precision.

Top Players Analysis

- Schaeffler AG leads with strong valvetrain and engine actuation technologies supporting advanced combustion optimization systems.

- BorgWarner Inc. focuses on advanced powertrain solutions and efficiency-enhancing engine technologies for global OEMs.

- Eaton Corporation specializes in valvetrain systems and fuel-saving engine technologies for passenger and commercial vehicles.

- Continental AG contributes advanced electronic control systems and engine management software for cylinder deactivation platforms.

- Delphi Technologies provides integrated engine control solutions and fuel efficiency technologies for modern automotive platforms.

- Bosch Mobility plays a key role in engine control systems and electronic fuel optimization technologies.

- Denso Corporation develops advanced automotive engine control systems and efficiency optimization components.

Key Players List

Schaeffler AG, BorgWarner Inc., Eaton Corporation plc, Continental AG, Delphi Technologies, Bosch Mobility, Denso Corporation, Hitachi Astemo, Aisin Corporation, Mahle GmbH, Marelli Holdings Co., Ltd., Valeo S.A., Infineon Technologies AG