Automotive Engine Market Research Report

Get Your Sample Report Here: https://www.redlinepulse.com/report/automotive-engine-market/request-sample

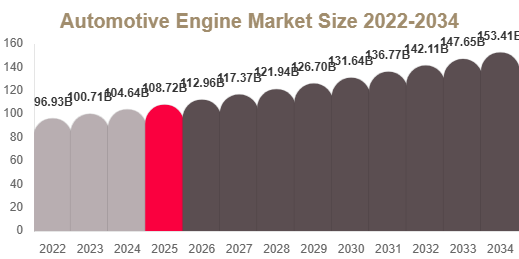

Market Size

The global automotive engine market size was valued at USD 108.42 billion in 2025 and is estimated to reach USD 112.96 billion in 2026.

The market is projected to grow to USD 152.84 billion by 2034, registering a CAGR of 3.9% from 2025 to 2034.

The market continues to expand due to sustained internal combustion engine demand, hybrid vehicle integration, and rising focus on fuel-efficient engine technologies across global automotive production systems.

Market Overview

The automotive engine market remains a foundational pillar of the global automotive industry despite rapid electrification trends. Internal combustion engines continue to power a large share of passenger and commercial vehicles, supported by strong hybrid adoption and ongoing technological improvements in engine efficiency. Manufacturers are focusing on balancing performance, emissions compliance, and cost efficiency to extend the lifecycle of combustion engines in a transitioning mobility ecosystem.

Market Drivers

Continued Demand for Internal Combustion and Hybrid Vehicles

The automotive engine market is strongly supported by the continued global reliance on gasoline and diesel vehicles, especially in regions with limited EV infrastructure. Hybrid vehicles are also contributing significantly as they still depend on advanced combustion engines for efficient operation. According to Redline Pulse analysis, this dual demand structure is sustaining long-term engine production volumes and innovation cycles across OEMs and suppliers.

Increasing Focus on Fuel Efficiency and Emissions Reduction

Strict global emissions regulations are pushing automakers to develop more efficient engines using turbocharging, direct injection, and advanced combustion systems. These innovations help reduce fuel consumption while maintaining performance. Engine optimization technologies are becoming essential to comply with environmental standards without fully replacing internal combustion systems.

Market Challenges

Shift Toward Electric Mobility

The increasing shift toward battery electric vehicles presents a structural challenge for the automotive engine market. Government policies promoting zero-emission transportation are reducing long-term demand for traditional engines, especially in developed regions. This shift is forcing manufacturers to reallocate investments toward electrified powertrain systems and reduce dependency on standalone engine development.

High Development Pressure on Engine Manufacturers

Engine manufacturers face rising pressure to meet evolving emission standards, efficiency targets, and cost constraints. This increases R&D complexity and limits flexibility in designing new combustion platforms. Integration of hybrid systems further increases engineering requirements across multiple engine architectures.

Market Segmentation Analysis

By Fuel Type

Gasoline engines dominate the market with a share of 48.7% in 2024 due to their wide application in passenger vehicles and hybrid systems. These engines are preferred for their smoother performance and lower cost. Hybrid-compatible gasoline engines are emerging as the fastest-growing segment, driven by increasing hybrid vehicle adoption and regulatory pressure to reduce emissions.

By Engine Capacity

The 1.5L to 3.0L engine category leads the market with a 44.2% share due to its balanced performance and efficiency across multiple vehicle types. Below 1.5L engines are witnessing strong growth as automakers focus on compact, fuel-efficient designs for urban mobility and cost-sensitive markets.

By Vehicle Type

Passenger vehicles account for 67.9% of the market, making them the largest segment due to high global production volumes. Light commercial vehicles are expected to grow faster, driven by logistics expansion, e-commerce growth, and fleet modernization trends.

Regional Analysis

Asia Pacific leads the automotive engine market with a 42.8% share and is also the fastest-growing region with a CAGR of 4.6%. China remains the key contributor due to large-scale automotive production and hybrid engine expansion. North America and Europe continue to focus on engine efficiency improvements, while emerging regions such as Latin America and Middle East & Africa maintain steady demand for combustion-based vehicles.

Competitive Landscape

The automotive engine market is highly competitive, with global OEMs and tier-1 suppliers focusing on efficiency improvements, hybrid integration, and emissions reduction technologies. Companies are investing heavily in next-generation combustion systems and hybrid-ready engine platforms to maintain competitiveness in a shifting mobility landscape.

Top Players Analysis

- Toyota Motor Corporation – Leading global hybrid engine and fuel-efficient combustion system developer with strong integration across passenger vehicle platforms.

- Volkswagen AG – Focused on advanced engine optimization technologies and hybrid-compatible combustion systems across global vehicle segments.

- Hyundai Motor Company – Expanding engine efficiency technologies with strong focus on hybrid and gasoline engine innovation.

- General Motors Company – Developing high-performance combustion engines and hybrid-compatible platforms for SUVs and trucks.

- Ford Motor Company – Strong presence in engine manufacturing for pickup trucks and utility vehicles with advanced fuel efficiency systems.

- Honda Motor Co., Ltd. – Focused on compact, efficient engines with hybrid integration and low-emission technologies.

- Nissan Motor Co., Ltd. – Investing in hybrid engine systems and advanced combustion efficiency solutions.

- Stellantis N.V. – Diversified engine portfolio across European and American markets with focus on hybrid-ready architectures.

- BMW AG – Premium engine systems focused on performance and efficiency optimization technologies.

- Mercedes-Benz Group AG – Advanced engine development for luxury vehicles with strong hybrid and emissions control technologies.

Conclusion

The automotive engine market is undergoing a transitional phase where internal combustion engines remain essential while adapting to hybridization and stricter environmental standards. Although electrification is reshaping long-term demand, engine innovation continues to play a critical role in global mobility. Manufacturers focusing on efficiency, hybrid compatibility, and flexible fuel technologies are expected to maintain strong relevance throughout the forecast period.