Digital Cockpit Market Report

Get Your Sample Report Here: https://www.redlinepulse.com/report/digital-cockpit-market/request-sample

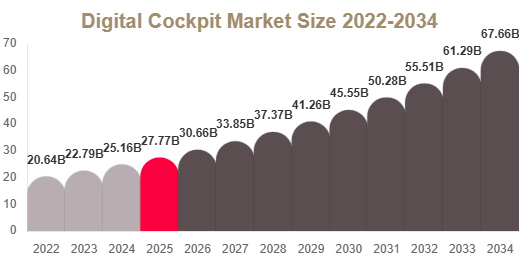

Digital Cockpit Market Size

The global digital cockpit market size was valued at USD 27.84 billion in 2025 and is projected to reach USD 30.66 billion in 2026.

The market is expected to reach USD 67.92 billion by 2034, expanding at a CAGR of 10.4% from 2025 to 2034.

This growth is driven by the increasing shift toward software-defined vehicle interiors and integrated digital cabin systems across passenger and electric vehicles.

Market Overview

Digital cockpits are transforming vehicle interiors by integrating instrument clusters, infotainment systems, head-up displays, and AI-based interfaces into a unified digital ecosystem. Automakers are rapidly replacing traditional analog dashboards with smart, connected, and highly interactive cockpit platforms.

The evolution of connected vehicles and increasing consumer demand for digital experiences are accelerating adoption across both premium and mass-market segments.

Market Drivers

Rising Demand for Connected In-Vehicle Experience

Consumers now expect vehicles to function like smart devices with seamless connectivity, large displays, and intuitive interfaces. This demand is pushing OEMs to integrate advanced digital cockpit systems across multiple vehicle categories.

Expansion of ADAS Integration

The integration of advanced driver assistance systems is increasing the need for real-time visualization of alerts, navigation, and safety data. Digital cockpits serve as the central interface for delivering this critical information.

Growth of Electric and Software-Defined Vehicles

Electric vehicles are accelerating cockpit innovation due to their digital-first architecture, enabling more advanced displays, AI interfaces, and connected services.

Market Challenges

High System Integration Cost

Digital cockpit systems require multiple advanced components such as processors, displays, sensors, and software stacks, which significantly increase production costs for OEMs.

Software Complexity and Validation

Ensuring cybersecurity, system stability, and seamless performance across multiple vehicle platforms increases development time and validation complexity for manufacturers.

Market Opportunities

Software-Defined Vehicle Ecosystem

The shift toward software-defined vehicles is creating new revenue opportunities through over-the-air updates, subscription-based features, and digital services integrated into cockpit systems.

Mass-Market Penetration of Digital Cockpits

Declining display costs and scalable architectures are enabling adoption of digital cockpit technologies in mid-range and economy vehicles, expanding the total addressable market.

Segmental Analysis

By Component Type

The digital instrument cluster segment dominates the market due to its wide adoption in modern vehicles for displaying navigation, speed, and vehicle diagnostics in real time.

Head-up displays are emerging as the fastest-growing segment, improving driver safety by projecting essential information directly into the driver’s line of sight.

By Vehicle Type

Passenger cars hold the largest share due to high production volume and increasing integration of connected infotainment and digital interface systems.

Electric vehicles are growing rapidly as they adopt fully digital and software-defined cockpit architectures.

By Display Technology

TFT-LCD displays dominate due to cost efficiency and widespread adoption across mainstream vehicles.

OLED displays are gaining traction in premium vehicles due to superior image quality and design flexibility.

Regional Analysis

North America

North America leads due to strong adoption of connected vehicles and increasing integration of digital infotainment systems in SUVs and passenger cars.

Europe

Europe shows strong demand driven by premium vehicle manufacturing and advanced automotive engineering capabilities.

Asia Pacific

Asia Pacific is the fastest-growing region due to rising vehicle production, EV adoption, and increasing demand for smart cockpit systems.

Middle East & Africa

The region is growing steadily with increasing demand for luxury and technology-rich vehicles in urban markets.

Latin America

Latin America is witnessing gradual adoption supported by rising consumer awareness of digital infotainment systems in passenger vehicles.

Competitive Landscape

The digital cockpit market is highly competitive with global automotive suppliers and electronics companies focusing on integrated cabin platforms, AI-based interfaces, and advanced display systems.

- Continental AG leads with strong cockpit integration solutions and OEM partnerships across global markets.

- Robert Bosch GmbH focuses on advanced driver interface systems and connected mobility solutions.

- Visteon Corporation specializes in digital cluster and infotainment system development for global OEMs.

- DENSO Corporation provides integrated cockpit electronics and automotive software platforms.

- Panasonic Automotive Systems focuses on advanced display technologies and connected cockpit solutions.

Key Players List

Continental AG, Robert Bosch GmbH, Visteon Corporation, DENSO Corporation, Panasonic Automotive Systems, Hyundai Mobis, Harman International, Marelli Holdings Co., Ltd., Aptiv PLC, LG Electronics Vehicle Component Solutions, Nippon Seiki Co., Ltd., Qualcomm Technologies, Inc., Samsung Display Co., Ltd., Pioneer Corporation, Valeo SA, Forvia, Garmin Ltd., JVCKENWOOD Corporation