Market Overview

The Automotive Composite Body Panel Market is experiencing steady expansion driven by increasing demand for lightweight vehicles, stricter emission regulations, and rising adoption of advanced material technologies. According to Redline Pulse, automakers are increasingly shifting from traditional steel and aluminum components toward advanced composite solutions.

Get Your Sample Report Here: https://www.redlinepulse.com/report/automotive-composite-body-panel-market

The market growth is strongly supported by the rise of electric vehicles, where weight reduction plays a crucial role in improving battery efficiency and driving range.

Market Size and Forecast (2025–2034)

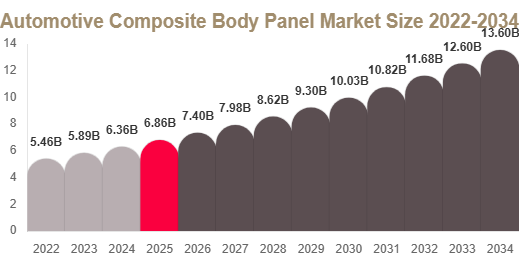

Automotive Composite Body Panel Market Size (2025–2034)

As per Redline Pulse, the market was valued at approximately USD 6.8 billion in 2025 and is projected to reach USD 7.4 billion in 2026.

The market is expected to grow to around USD 13.9 billion by 2034, registering a CAGR of 7.9% during 2025–2034.

Get Complete Market Insights Here: https://www.redlinepulse.com/report/automotive-composite-body-panel-market

This growth is driven by regulatory pressure for emission reduction, rising EV adoption, and advancements in composite manufacturing technologies.

Market Drivers

Strict Emission Regulations

Government policies aimed at reducing carbon emissions are pushing automakers to adopt lightweight composite materials to improve fuel efficiency and meet compliance standards.

Rising Electric Vehicle Adoption

Electric vehicles require lightweight structures to maximize battery efficiency and driving range, significantly increasing demand for composite body panels.

Advancements in Manufacturing Technology

Innovations such as automated fiber placement and resin transfer molding are improving production efficiency and reducing costs.

Growth in Premium and Luxury Vehicles

Luxury and performance vehicles increasingly use composite materials for better aerodynamics, design flexibility, and enhanced aesthetics.

Market Challenges

High Production Costs

Composite manufacturing involves advanced processes that increase production costs compared to traditional metal components.

Recycling Limitations

Difficulty in recycling composite materials remains a key environmental and operational challenge.

Limited Adoption in Low-Cost Vehicles

Due to cost sensitivity, composite materials are still primarily used in premium and high-performance vehicle segments.

Market Segmentation (Detailed Analysis)

According to Redline Pulse, the market is segmented by material type, application, and vehicle type.

By Material Type

Carbon Fiber Reinforced Polymer (CFRP)

Glass Fiber Reinforced Polymer (GFRP)

Hybrid Composites

CFRP dominates due to high strength and lightweight properties, while GFRP is growing fastest due to cost advantages.

By Application

Exterior Body Panels

Interior Components

Structural Components

Exterior body panels dominate due to high usage in doors, hoods, and fenders, while structural components are the fastest-growing segment.

By Vehicle Type

Passenger Vehicles

Commercial Vehicles

Electric Vehicles

Passenger vehicles dominate due to high production volumes, while electric vehicles are the fastest-growing segment due to lightweight requirements.

Regional Analysis

North America leads the market with strong adoption of lightweight materials and EV expansion. Europe follows with strict emission regulations driving composite usage. Asia Pacific is the fastest-growing region with a CAGR of 8.7% due to high vehicle production and EV adoption in China and India. Middle East & Africa shows gradual growth driven by luxury vehicle demand, while Latin America is expanding steadily due to automotive industry development.

Top Players Analysis

1. Toray Industries Inc.

Leading global supplier of carbon fiber composites with strong automotive integration.

2. Teijin Limited

Specializes in advanced carbon fiber and high-performance composite materials.

3. SGL Carbon SE

Major player in carbon-based composite solutions for automotive applications.

4. Mitsubishi Chemical Group Corporation

Focuses on innovative lightweight materials for vehicle manufacturing.

5. Solvay S.A.

Provides advanced polymer and composite solutions for automotive industry.

6. Hexcel Corporation

Specialist in aerospace-grade composites increasingly used in automotive sector.

7. Owens Corning

Leader in glass fiber reinforced materials for automotive applications.

8. BASF SE

Develops advanced polymer solutions for lightweight automotive components.

9. Dow Inc.

Focuses on material science innovation for automotive composites.

10. Magna International Inc.

Provides integrated automotive systems including composite body structures.

Conclusion

The Automotive Composite Body Panel Market is set for strong growth through 2034, driven by EV expansion, emission regulations, and advancements in lightweight material technology. With a CAGR of 7.9%, the market will continue transitioning toward high-performance, fuel-efficient, and sustainable automotive structures.