Market Overview

The Automotive Intelligent Headlight System Market is expanding steadily due to increasing adoption of advanced automotive lighting technologies aimed at improving road safety, driving comfort, and vehicle aesthetics. According to Redline Pulse, growth is strongly driven by ADAS integration, autonomous driving development, and rising demand for premium vehicle features.

Get Your Sample Report Here: https://www.redlinepulse.com/report/automotive-intelligent-headlight-system-market

Automakers are increasingly adopting adaptive and intelligent lighting systems such as matrix LED and laser headlights to enhance visibility while reducing glare for oncoming traffic.

Market Size and Forecast (2025–2034)

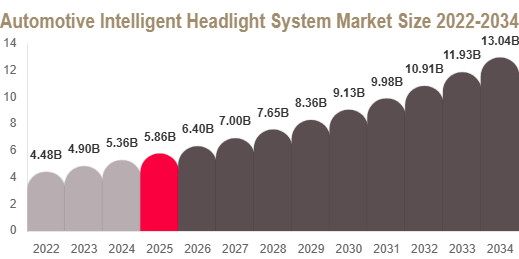

Automotive Intelligent Headlight System Market Size (2025–2034)

As per Redline Pulse, the market was valued at USD 5.9 billion in 2025 and is projected to reach USD 6.4 billion in 2026.

The market is expected to reach around USD 13.2 billion by 2034, registering a CAGR of 9.3% during 2025–2034.

Get Complete Market Insights Here: https://www.redlinepulse.com/report/automotive-intelligent-headlight-system-market

Growth is driven by increasing vehicle safety regulations, rising EV adoption, and integration of smart lighting with connected vehicle systems.

Market Drivers

Rising Adoption of ADAS Technologies

Advanced Driver Assistance Systems are increasing demand for intelligent headlights that adjust beam direction and intensity based on speed, steering, and road conditions.

Increasing Focus on Road Safety

Governments worldwide are enforcing stricter lighting and safety standards, encouraging adoption of adaptive and glare-free headlight systems.

Growth of Electric and Autonomous Vehicles

EVs and autonomous vehicles require intelligent lighting for energy efficiency, communication, and enhanced sensor integration.

Consumer Demand for Premium Vehicle Features

Consumers increasingly prefer vehicles with advanced lighting systems such as matrix LED and laser headlights for improved visibility and aesthetics.

Market Challenges

High Cost of Advanced Lighting Systems

Matrix LED and laser headlights require complex sensors and electronics, making them expensive and limiting adoption in low-cost vehicles.

Limited Penetration in Emerging Markets

Cost sensitivity in developing regions restricts adoption of advanced intelligent lighting systems.

Technical Integration Complexity

Integration with ADAS and vehicle electronics increases system complexity and development costs.

Market Segmentation (Detailed Analysis)

According to Redline Pulse, the market is segmented by technology type, vehicle type, and application type.

By Technology Type

LED Adaptive Headlights

Laser Headlights

Halogen Adaptive Systems

Matrix Lighting Systems

LED adaptive headlights dominate due to energy efficiency and versatility, while laser headlights are the fastest-growing segment due to superior brightness and range.

By Vehicle Type

Passenger Vehicles

Commercial Vehicles

Electric Vehicles

Passenger vehicles dominate due to high adoption of safety features, while EVs are the fastest-growing segment due to efficiency and smart integration needs.

By Application Type

Adaptive Front Lighting System

Adaptive High Beam System

Cornering Light System

Glare-Free High Beam System

Adaptive front lighting systems dominate, while adaptive high beam systems are growing fastest due to safety regulations and night driving improvements.

Regional Analysis

North America leads the market with strong adoption of ADAS and premium vehicles. Europe follows due to strict safety regulations and strong automotive engineering base. Asia Pacific is the fastest-growing region with a CAGR of 10.2%, driven by rapid EV adoption and vehicle production growth in China and India. The Middle East & Africa region is expanding due to demand for luxury vehicles and harsh driving conditions requiring advanced lighting systems. Latin America shows steady growth supported by increasing safety awareness and automotive modernization.

Top Players Analysis

1. HELLA GmbH & Co. KGaA

A leading innovator in matrix LED and adaptive lighting systems for modern vehicles.

2. Koito Manufacturing Co., Ltd.

Specializes in automotive lighting solutions with strong global OEM partnerships.

3. Valeo SA

Focuses on advanced lighting systems integrated with ADAS technologies.

4. Stanley Electric Co., Ltd.

Provides high-performance automotive lighting systems for global markets.

5. Osram Continental GmbH

Develops intelligent lighting systems combining electronics and lighting innovation.

6. Denso Corporation

Offers integrated automotive electronics and smart lighting solutions.

7. Hyundai Mobis Co., Ltd.

Focuses on next-generation mobility lighting systems for EVs and autonomous vehicles.

8. ZKW Group

Specializes in premium LED and laser headlight systems.

9. Robert Bosch GmbH

Develops sensor-integrated intelligent lighting and automotive electronics.

10. Lumileds Holding B.V.

Known for LED innovation and high-efficiency automotive lighting solutions.

Conclusion

The Automotive Intelligent Headlight System Market is set for strong growth through 2034, driven by ADAS expansion, EV adoption, and increasing demand for safety-focused automotive technologies. With a projected CAGR of 9.3%, intelligent lighting systems are becoming a core component of modern vehicle design and safety architecture.