Market Overview

The Driveline Systems for Electric Vehicle Market is witnessing strong expansion driven by rapid electrification of transportation and increasing demand for high-efficiency power transmission systems. According to Redline Pulse, the market is evolving due to continuous innovation in EV architecture and the shift from internal combustion engines to electric mobility platforms.

Get Your Sample Report Here: https://www.redlinepulse.com/report/driveline-systems-for-electric-vehicle-market

The market is strongly influenced by advancements in electric drivetrains, including e-axles, electric transmissions, and integrated motor-drive systems that enhance performance and energy efficiency.

Market Size and Forecast (2025–2034)

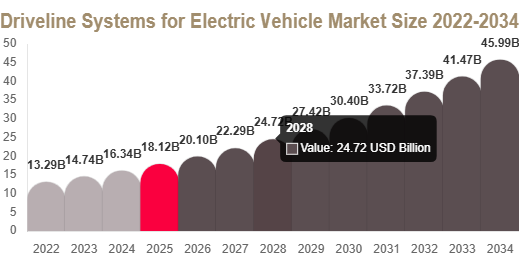

Driveline Systems for Electric Vehicle Market Size (2025–2034)

As per Redline Pulse, the market is valued at USD 18.5 billion in 2025 and is projected to reach USD 20.1 billion in 2026.

The market is expected to grow significantly and reach approximately USD 45.8 billion by 2034, registering a CAGR of 10.9% during 2025–2034.

Get Complete Market Insights Here: https://www.redlinepulse.com/report/driveline-systems-for-electric-vehicle-market

This growth is driven by rising EV production, technological advancements in driveline systems, and increasing focus on vehicle efficiency and performance optimization.

Market Drivers

Rapid Expansion of Electric Vehicle Production

The global shift toward electric vehicles is significantly increasing demand for advanced driveline systems, including e-transmissions and integrated motor units.

Advancements in Power Electronics

Innovations in silicon carbide, motor design, and inverter efficiency are improving energy conversion and reducing losses, boosting driveline performance.

Government Support for EV Adoption

Incentives, subsidies, and emission regulations are accelerating EV adoption, directly increasing demand for driveline technologies.

Focus on Vehicle Performance Optimization

Automakers are prioritizing acceleration, torque control, and energy efficiency, driving adoption of integrated driveline architectures.

Market Challenges

High Development and Integration Costs

Advanced driveline systems require complex engineering and expensive components, increasing overall production costs.

Price Sensitivity in Entry-Level EVs

Manufacturers often limit advanced driveline integration in low-cost EVs to maintain affordability.

Technical Complexity

Integration of motor, gearbox, and power electronics requires high precision manufacturing and engineering expertise.

Market Segmentation (Detailed Analysis)

According to Redline Pulse, the market is segmented by component type, vehicle type, and propulsion type.

By Component Type

Electric Transmission Systems

Electric Axle Systems

Driveshaft Systems

Electric transmission systems dominate due to their role in torque delivery, while electric axle systems are the fastest-growing due to compact integrated design.

By Vehicle Type

Passenger Electric Vehicles

Commercial Electric Vehicles

Performance Electric Vehicles

Passenger EVs dominate the market, while commercial EVs are the fastest-growing segment due to fleet electrification.

By Propulsion Type

Battery Electric Vehicles

Hybrid Electric Vehicles

Plug-in Hybrid Electric Vehicles

Battery electric vehicles hold the largest share, while hybrids are growing due to transitional electrification strategies.

Regional Analysis

North America leads the market with 32.6% share due to strong EV adoption and advanced manufacturing capabilities. Europe follows with strict emission regulations and strong premium EV production. Asia Pacific is the fastest-growing region with a CAGR of 12.1%, driven by large-scale EV manufacturing in China and rising adoption in India and Japan. Middle East & Africa is gradually expanding due to smart mobility initiatives, while Latin America shows steady growth driven by rising electrification awareness and automotive development.

Top Players Analysis

1. Robert Bosch GmbH

Leading innovator in EV driveline systems with strong e-axle development capabilities.

2. ZF Friedrichshafen AG

Specializes in integrated electric driveline and transmission technologies.

3. GKN Automotive

Focuses on advanced e-drive systems and electric axle solutions.

4. BorgWarner Inc.

Provides high-efficiency electric propulsion and driveline systems.

5. Magna International Inc.

Develops integrated EV drivetrain architectures and systems.

6. Dana Incorporated

Known for electric axle and propulsion system innovation.

7. Schaeffler AG

Focuses on high-performance EV drivetrain components.

8. Continental AG

Develops integrated mobility and electric driveline technologies.

9. Hitachi Astemo

Specializes in electric powertrain and drivetrain solutions.

10. Hyundai Mobis

Key supplier of EV driveline systems with strong OEM integration.

Conclusion

The Driveline Systems for Electric Vehicle Market is set for strong growth through 2034, driven by rapid EV adoption, technological advancements in power electronics, and increasing demand for high-efficiency drivetrains. With a projected CAGR of 10.9%, the market will continue expanding as electric mobility becomes the global standard.