Market Overview

The Automotive Fuel Level Sensor Market plays a critical role in modern vehicle systems by enabling accurate monitoring of fuel levels, improving driving efficiency, and supporting better fuel management. As per Redline Pulse, the market is driven by rising vehicle production, increasing adoption of advanced automotive electronics, and growing demand for connected vehicle systems across passenger and commercial segments.

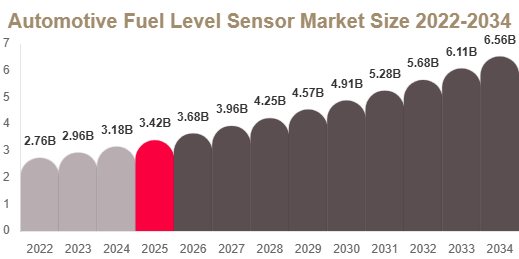

Automotive Fuel Level Sensor Market Size

Market Size 2025

The Automotive Fuel Level Sensor market size is estimated at USD 3.45 billion in 2025, driven by steady vehicle production and increasing integration of electronic sensing technologies.

Market Size 2034

By 2034, the market is projected to reach USD 6.92 billion, supported by continuous adoption of advanced fuel monitoring systems across global automotive production.

CAGR (2025–2034)

The market is expected to grow at a CAGR of 7.5% during 2025–2034, reflecting stable demand growth across OEM and aftermarket channels.

Market Drivers

Rising Vehicle Production and Electronic Integration

Increasing global vehicle production, especially in emerging economies, is driving demand for fuel level sensors. Modern vehicles increasingly rely on electronic systems, making accurate fuel monitoring essential for performance and efficiency.

Strict Fuel Efficiency and Emission Regulations

Governments worldwide are enforcing stricter emission and fuel economy standards. This is pushing manufacturers to adopt precise fuel monitoring systems that help optimize engine performance and reduce fuel wastage.

Growth of Connected Vehicles

The rise of connected and smart vehicles is increasing the need for real-time sensor data. Fuel level sensors are becoming an important part of telematics systems and digital dashboards.

Market Challenges

Sensor Inaccuracy Under Dynamic Conditions

Fuel sloshing, temperature variation, and tank design complexity can impact sensor accuracy, especially in traditional systems, leading to inconsistent readings.

High Cost of Advanced Sensors

Advanced technologies like capacitive and ultrasonic sensors are more expensive, increasing vehicle production costs and limiting adoption in low-cost vehicle segments.

Preference for Basic Sensor Systems

In price-sensitive markets, manufacturers often prefer simpler sensor technologies, slowing down adoption of advanced digital fuel level sensing solutions.

Market Segmentation

By Product Type

Capacitive Sensors

This segment dominates the market with a 44.2% share in 2025 due to high accuracy, durability, and stable performance across different fuel conditions.

Ultrasonic Sensors

Expected to grow at the fastest rate due to non-contact measurement technology and improved accuracy in modern vehicle systems.

Resistive Sensors

These remain widely used in entry-level and cost-sensitive vehicle segments due to low cost and simple design.

By Application

Passenger Cars

This segment dominates with a 61.5% share in 2025 due to high production volumes and widespread adoption of advanced electronics.

Commercial Vehicles

Expected to grow steadily due to rising demand for fleet monitoring and fuel optimization systems.

By Distribution Channel

OEM

OEM segment leads with a 58.3% share in 2025 due to direct integration of sensors in new vehicles during manufacturing.

Aftermarket

Expected to grow steadily due to increasing replacement demand from aging vehicle fleets.

Key Players Analysis

Bosch

Bosch is a leading global player offering advanced fuel level sensor technologies with high precision and durability for modern vehicles.

Continental AG

Continental focuses on innovative automotive electronics and integrated sensor solutions for fuel monitoring systems.

Denso Corporation

Denso develops high-performance sensors designed for improved accuracy and reliability in automotive applications.

Delphi Technologies

Delphi provides advanced sensing solutions focusing on fuel efficiency and vehicle performance optimization.

TE Connectivity

TE Connectivity specializes in sensor and connectivity solutions for automotive fuel monitoring systems.

Sensata Technologies

Sensata develops durable sensing solutions designed for harsh automotive environments and high reliability.

NXP Semiconductors

NXP focuses on semiconductor-based sensor technologies enabling smart and connected vehicle systems.

Infineon Technologies

Infineon provides advanced electronic components supporting next-generation automotive sensing systems.

Valeo

Valeo offers integrated automotive sensor solutions with a focus on efficiency and system reliability.

Hitachi Astemo

Hitachi Astemo develops advanced mobility solutions including fuel monitoring and sensor technologies.

Regional Analysis

North America

North America holds a 36.9% share in 2025, driven by strong automotive production and high adoption of advanced electronic systems. Integration of fuel sensors with telematics and digital dashboards is a key growth factor.

Europe

Europe accounts for 26.8% share, supported by strict emission standards and strong focus on fuel efficiency and automotive innovation.

Asia Pacific

Asia Pacific is the fastest-growing region with a CAGR of 8.6%, driven by rising vehicle production, urbanization, and increasing adoption of smart automotive technologies.

Middle East & Africa

Growth is supported by rising vehicle demand and increasing adoption of modern automotive systems in harsh environmental conditions.

Latin America

Gradual growth is driven by expanding automotive production and increasing aftermarket demand, especially in Brazil and Mexico.

Conclusion

The Automotive Fuel Level Sensor Market is expected to grow steadily through 2034, supported by rising vehicle production, regulatory pressure, and increasing demand for connected vehicle systems. While challenges such as sensor inaccuracy and cost constraints exist, ongoing technological advancements and aftermarket expansion are expected to drive long-term market growth.

Get Your Sample Report Here: https://www.redlinepulse.com/report/automotive-fuel-level-sensor-market/request-sample