Market Overview

The Automotive Digital Mirror Market is emerging as a key segment within advanced driver assistance systems, driven by increasing integration of camera-based visibility solutions in modern vehicles. As per Redline Pulse, digital mirrors are replacing conventional side and rear-view mirrors with high-resolution camera and display systems, improving safety, aerodynamics, and driving visibility across passenger and commercial vehicles.

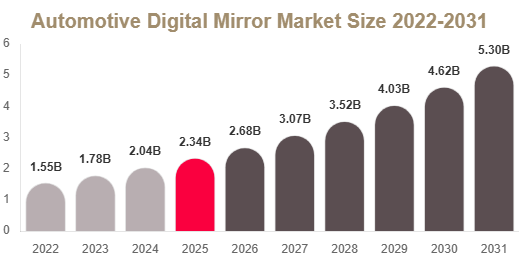

Automotive Digital Mirror Market Size

Market Size 2025

The Automotive Digital Mirror Market size is estimated at USD 2.35 billion in 2025, supported by rising demand for advanced safety technologies and regulatory support for improved visibility systems.

Market Size 2034

The market is projected to reach USD 7.95 billion by 2034, driven by increasing adoption in electric, luxury, and premium vehicle segments.

CAGR (2025–2034)

The market is expected to grow at a CAGR of 14.6% during 2025–2034, reflecting strong adoption of camera-based visibility systems globally.

Market Drivers

Increasing Vehicle Safety Regulations

Governments across major regions are enforcing strict safety standards to reduce blind spots and improve road visibility. Digital mirrors provide a wider field of view, making them essential for compliance with modern vehicle safety norms.

Rising Adoption of Electric Vehicles

Electric vehicles increasingly use digital mirrors to reduce aerodynamic drag and improve driving range. This makes them a preferred solution for next-generation EV platforms.

Growing Demand for Advanced Driver Assistance Systems

Digital mirrors are becoming an integral part of ADAS ecosystems, improving visibility through integration with lane assist, collision warning, and blind spot detection systems.

Market Challenges

High System Cost

Digital mirror systems require advanced cameras, displays, and processing units, increasing vehicle production costs and limiting adoption in entry-level segments.

Weather and Environmental Limitations

Performance can be affected under heavy rain, fog, or snow conditions where camera visibility may be reduced or distorted.

Consumer Acceptance Issues

Some drivers still prefer traditional mirrors due to familiarity and perceived reliability, slowing full-scale adoption.

Market Segmentation

By Type

Side Digital Mirrors

This segment dominates the market with a 52.4% share in 2025 due to widespread adoption in passenger vehicles and electric SUVs, offering improved aerodynamics and safety.

Rear Digital Mirrors

Expected to grow at the fastest rate due to enhanced rear visibility and integration with ADAS systems.

Interior Digital Mirrors

Used in premium vehicles for improved rear visibility and display integration.

Smart Integrated Mirror Systems

Advanced systems combining multiple visibility functions into a single digital interface.

By Vehicle Type

Passenger Vehicles

This segment dominates with a 61.8% share in 2025 due to high adoption in SUVs, sedans, and EVs.

Commercial Vehicles

Expected to grow steadily due to demand for fleet safety and visibility improvements.

Electric Vehicles

Strong adoption due to aerodynamic efficiency and energy optimization benefits.

Luxury Vehicles

Early adopters of digital mirror technology due to premium feature integration.

By Technology

Camera-Based Systems

This segment dominates with a 58.7% share in 2025 due to high reliability and wide-angle visibility.

AI-Integrated Systems

Expected to grow fastest due to object detection, adaptive imaging, and smart assistance features.

Display-Based Systems

Provide real-time visual output for improved driver awareness.

Sensor Fusion Systems

Combine camera, radar, and sensor inputs for enhanced accuracy and safety.

Key Players Analysis

Gentex Corporation

Gentex is a leading innovator in digital vision systems with strong expertise in electro-optical automotive technologies.

Magna International

Magna focuses on integrated vehicle systems and advanced mobility solutions, including digital mirror technologies.

Bosch

Bosch develops advanced automotive electronics and camera-based systems for safety and visibility enhancement.

Ficosa International

Ficosa specializes in smart automotive vision systems and advanced driver assistance technologies.

Samvardhana Motherson Group

A major supplier of automotive components including mirror systems and electronic mobility solutions.

Panasonic Corporation

Panasonic provides imaging and electronic display technologies for automotive applications.

Continental AG

Continental develops advanced ADAS systems integrating digital mirror and sensor technologies.

Valeo

Valeo focuses on intelligent mobility solutions including camera-based visibility systems.

Denso Corporation

Denso develops automotive electronics and high-precision sensing systems.

Hyundai Mobis

Hyundai Mobis is expanding its ADAS and smart mobility technology portfolio, including digital mirrors.

Regional Analysis

North America

North America holds a 35.2% share in 2025 due to strong adoption of ADAS systems and increasing integration in premium vehicles.

Europe

Europe accounts for 29.4% share, driven by strict safety regulations and strong demand for aerodynamic vehicle designs.

Asia Pacific

Asia Pacific is the fastest-growing region with a CAGR of 16.1%, driven by EV growth, rising vehicle production, and smart mobility adoption.

Middle East & Africa

Growth is supported by increasing luxury vehicle demand and improving road safety standards.

Latin America

Steady adoption driven by modernization of vehicle fleets and rising awareness of advanced safety systems.

Conclusion

The Automotive Digital Mirror Market is set for strong expansion through 2034, driven by increasing safety regulations, rising EV adoption, and rapid advancements in camera-based vehicle technologies. While high costs and environmental limitations remain challenges, continuous innovation in AI-integrated systems and ADAS integration is expected to drive long-term market growth.

Get Your Sample Report Here: https://www.redlinepulse.com/report/automotive-digital-mirror-market/request-sample