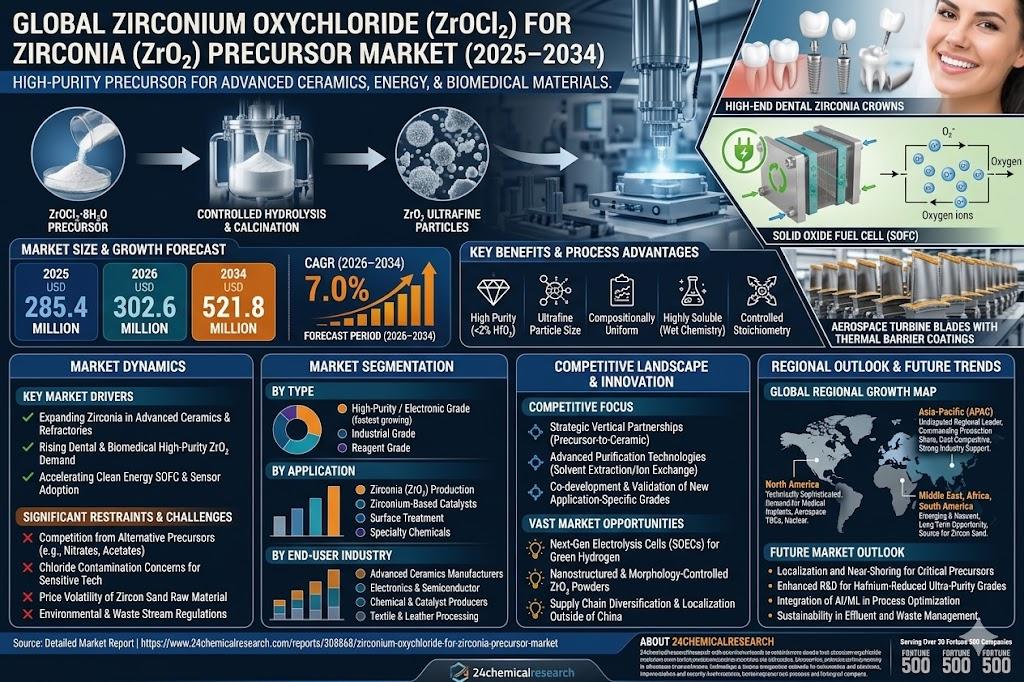

Global Zirconium Oxychloride (ZrOCl₂) for Zirconia (ZrO₂) Precursor market was valued at USD 285.4 million in 2025 and is projected to grow from USD 302.6 million in 2026 to USD 521.8 million by 2034, exhibiting a CAGR of 7.0% during the forecast period.

Zirconium Oxychloride (ZrOCl₂·8H₂O), commonly known as zirconyl chloride, has long served as one of the most commercially reliable inorganic precursors for synthesizing zirconia (ZrO₂) and its stabilized ceramic variants. Produced through the chlorination of zircon sand or baddeleyite, it functions as the critical feedstock for manufacturing high-purity zirconia powders that find application across advanced ceramics, surface coatings, heterogeneous catalysts, and refractory materials. What makes ZrOCl₂ particularly indispensable is its capacity to yield ultrafine, compositionally uniform zirconia particles upon controlled hydrolysis or thermal decomposition — a characteristic that is simply not easy to replicate using alternative precursor chemistries. As industries worldwide continue to push the performance boundaries of structural and functional ceramics, the upstream demand for consistent, high-purity ZrOCl₂ has risen proportionately, positioning this precursor market at the intersection of advanced materials science and industrial-scale chemistry.

Get Full Report Here: https://www.24chemicalresearch.com/reports/308868/zirconium-oxychloride-for-zirconia-precursor-market

Market Dynamics:

The market's trajectory is shaped by a complex interplay of powerful growth drivers, significant restraints that are being actively addressed, and vast, untapped opportunities across multiple high-growth industries.

Powerful Market Drivers Propelling Expansion

- Expanding Demand for Zirconia in Advanced Ceramics and Refractory Applications: Zirconium oxychloride serves as one of the most commercially significant precursors for the synthesis of zirconia, owing to its high solubility in water, ease of purification, and consistent stoichiometric yield during thermal decomposition. The advanced ceramics industry remains the primary end-use sector, where zirconia derived from ZrOCl₂ is valued for its exceptional mechanical strength, high fracture toughness, and thermal stability exceeding 2,700°C. These properties make it indispensable in the manufacture of cutting tools, dental prosthetics, and structural components operating under extreme thermal and mechanical stress. As global manufacturing sectors continue to adopt high-performance ceramics to replace metals and polymers in demanding applications, the upstream demand for high-purity ZrOCl₂ as a zirconia precursor has risen commensurately, and this trajectory shows no signs of slowing.

- Growth of the Dental and Biomedical Sector Fueling High-Purity Zirconia Requirements: The dental ceramics segment represents one of the fastest-growing application areas for zirconia, with yttria-stabilized zirconia (YSZ) — synthesized in large part from ZrOCl₂ precursors — becoming the material of choice for crowns, bridges, and implant abutments. The biocompatibility, aesthetics, and load-bearing capacity of YSZ have driven its widespread adoption in restorative dentistry, particularly as patient preference shifts away from traditional metal-ceramic restorations. Because dental-grade zirconia demands exceptional chemical purity with tightly controlled particle size distribution, manufacturers rely on ZrOCl₂ as a starting material due to its amenability to wet-chemical purification processes. This trend is especially pronounced in North America, Europe, and increasingly across East and Southeast Asia, where rising disposable incomes are driving greater access to advanced dental care. The dental zirconia market was valued at approximately USD 2.1 billion in 2025 and is projected to expand steadily through 2034, directly reinforcing upstream demand for high-purity precursor-grade ZrOCl₂.

- Accelerating Adoption of Solid Oxide Fuel Cells and Clean Energy Technologies: Beyond ceramics and biomedical uses, ZrOCl₂ plays a critical role in the production of zirconia electrolytes used in solid oxide fuel cells (SOFCs) and lambda sensors for automotive exhaust management. The ionic conductivity of doped zirconia at elevated temperatures makes it uniquely suitable for oxygen ion transport — a property directly dependent on the purity and phase composition of the precursor-derived oxide. With global emphasis on cleaner energy systems and tighter vehicle emission standards driving sustained investment in fuel cell technology, the demand for electrolyte-grade zirconia, and consequently for ZrOCl₂, is expected to maintain a clearly upward trajectory over the medium-to-long term. Yttria-stabilized zirconia produced via ZrOCl₂ processing remains the electrolyte material of choice in SOFCs due to its superior ionic conductivity at high temperatures.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/308868/zirconium-oxychloride-for-zirconia-precursor-market

Significant Market Restraints Challenging Adoption

Despite its established industrial position, the ZrOCl₂ precursor market faces genuine structural and economic hurdles that participants must navigate carefully.

- Competition from Alternative Zirconia Precursors Limiting Market Penetration: While ZrOCl₂ is the dominant commercial precursor for zirconia synthesis, it faces meaningful competition from alternative zirconium compounds including zirconium nitrate, zirconium acetate, zirconium propoxide, and zirconium carbonate. Each of these alternatives offers specific processing advantages depending on the downstream application. Zirconium alkoxides, for instance, are preferred in sol-gel processes for thin film and coating applications where chloride contamination — a known issue with ZrOCl₂-derived precursors — can degrade dielectric or optical performance. The residual chloride ions introduced during ZrOCl₂ processing can require additional washing and calcination steps to achieve acceptable purity in sensitive applications, adding cost and reducing throughput efficiency compared to chloride-free precursor routes.

- Price Volatility of Zircon Sand and Its Impact on Downstream Precursor Economics: The economic viability of ZrOCl₂ production is closely tied to the price of zircon sand, which has historically exhibited significant cyclical volatility driven by fluctuations in the construction sector, shifts in mining output from major producers, and speculative inventory behavior among traders. This price volatility translates directly into input cost uncertainty for ZrOCl₂ manufacturers, making long-term supply contracting with downstream customers difficult and compressing margins during periods of elevated raw material costs. Smaller producers with limited hedging capacity and fewer economies of scale are disproportionately affected, which has contributed to market consolidation around larger integrated operators while creating real barriers to entry for new participants.

Critical Market Challenges Requiring Innovation

A fundamental challenge facing the ZrOCl₂ for zirconia precursor market is the geographic concentration of both raw material supply and processing capacity. Zirconium oxychloride is produced primarily through the chlorination or acid digestion of zircon sand (ZrSiO₄), and the global supply of zircon sand is dominated by Australia and South Africa, which together account for the majority of world production. This geographic concentration introduces supply security risks, as any disruption from regulatory changes, mining limitations, or logistical constraints in these regions can cascade through the entire downstream value chain.

Furthermore, high-end applications such as dental ceramics, fuel cell electrolytes, and optical coatings demand ZrOCl₂ with hafnium content below defined thresholds — typically less than 2% HfO₂ on a zirconia basis — along with tightly controlled levels of iron, silicon, and other metallic impurities. Achieving and maintaining this purity at commercial scale requires sophisticated multi-stage purification technologies, including solvent extraction and ion exchange processes. Inconsistency in raw material quality from zircon sand sources of varying mineralogical composition complicates batch-to-batch reproducibility, creating real quality assurance headaches for manufacturers supplying critical industrial and biomedical customers. The production of ZrOCl₂ also generates acidic effluents, chlorine-containing waste streams, and silica by-products that are subject to increasingly rigorous environmental regulations across major producing and consuming regions, including China, the European Union, and the United States. In China — which accounts for a substantial share of global ZrOCl₂ production capacity — periodic environmental enforcement campaigns have historically led to temporary plant curtailments, contributing to supply tightness and price volatility in the international market.

Vast Market Opportunities on the Horizon

- Expanding Role of Zirconia in Next-Generation Energy Technologies: The global energy transition is opening substantial new application avenues for zirconia that directly underpin demand for ZrOCl₂ as a precursor. Solid oxide electrolysis cells (SOECs), which convert electricity into hydrogen or syngas, rely on dense, high-purity zirconia electrolytes to achieve the ion transport properties needed for efficient operation. As governments and private sector actors scale investment in green hydrogen production infrastructure, the demand for electrolyte-grade zirconia is projected to grow in parallel. Additionally, the use of thermal barrier coatings (TBCs) based on yttria-stabilized zirconia in advanced gas turbines — including next-generation aviation engines designed to operate at higher temperatures for improved fuel efficiency — continues to expand the addressable market for precursor-grade ZrOCl₂ in ways that were simply not anticipated a decade ago.

- Technological Advancements in Zirconia Synthesis Opening Premium Market Segments: Innovations in precipitation and hydrothermal synthesis routes using ZrOCl₂ as a starting material are enabling the production of nanostructured and morphology-controlled zirconia powders with superior sintering behavior and enhanced mechanical properties. These advanced powder grades command significant price premiums over conventional zirconia and are finding adoption in high-value applications such as multilayer ceramic capacitors (MLCCs), piezoelectric devices, and photocatalysis. The ability to precisely tune particle size, surface area, and phase composition through controlled hydrolysis and calcination of ZrOCl₂ solutions gives this precursor a genuine technical advantage in accessing these emerging premium segments. Manufacturers that invest in process optimization and application-specific product development are well positioned to capture disproportionate value as these markets mature.

- Supply Chain Diversification Creating New Investment Opportunities: The growing localization of advanced materials supply chains — driven by geopolitical considerations and industrial policy initiatives in the United States, European Union, Japan, and South Korea — is creating meaningful opportunities for the establishment of new ZrOCl₂ production and refining capacity outside of China. This supply chain diversification trend is attracting investment interest from both established chemical manufacturers and new entrants seeking to serve domestic or allied-nation customers who require assured, auditable supply of critical precursor materials for defense, energy, and healthcare applications. For players who can move quickly and build the right quality credentials, this represents a genuine first-mover advantage.

In-Depth Segment Analysis: Where is the Growth Concentrated?

By Type:

The market is segmented into Industrial Grade Zirconium Oxychloride, High-Purity / Electronic Grade ZrOCl₂, and Reagent Grade ZrOCl₂. High-Purity / Electronic Grade ZrOCl₂ represents the most strategically significant and fastest-evolving type segment within the Zirconia precursor market. As downstream industries such as advanced ceramics, fuel cells, and semiconductor packaging increasingly demand ZrO₂ with minimal trace metal contamination, the requirement for ultra-pure precursor inputs has become a critical quality differentiator. Industrial grade ZrOCl₂, while widely available and cost-effective, continues to serve bulk processing applications where extreme purity tolerances are less critical. Reagent grade material occupies a niche position, primarily catering to laboratory research, catalyst development, and specialty chemical synthesis environments where precise stoichiometric control and reproducibility are paramount.

By Application:

Application segments include Zirconia (ZrO₂) Production, Zirconium-Based Catalyst Synthesis, Surface Treatment & Textile Finishing, and Specialty Chemicals & Others. Zirconia (ZrO₂) Production commands a dominant position as the primary application driving demand for Zirconium Oxychloride, given its role as the most efficient and widely adopted chemical precursor for synthesizing zirconia powders through precipitation and hydrothermal routes. The controlled hydrolysis of ZrOCl₂ in aqueous media enables precise manipulation of particle size, phase composition, and surface area — attributes that are directly consequential to the performance of the resulting zirconia in structural ceramics, thermal barrier coatings, and solid oxide fuel cell electrolytes. Zirconium-based catalyst synthesis represents a growing application, particularly in petroleum refining and green chemistry processes, where zirconia-supported catalysts offer exceptional thermal stability and surface acidity.

By End-User Industry:

The end-user landscape includes Advanced Ceramics Manufacturers, Chemical & Catalyst Producers, Electronics & Semiconductor Industry, and Textile & Leather Processing Industry. Advanced Ceramics Manufacturers represent the most prominent and technically demanding end-user segment for Zirconium Oxychloride as a ZrO₂ precursor. These manufacturers rely on high-consistency ZrOCl₂ feedstocks to synthesize zirconia powders with tightly controlled phase purity — whether monoclinic, tetragonal, or cubic — essential for applications ranging from dental prosthetics and cutting tools to aerospace thermal barrier coatings. The electronics and semiconductor industry is emerging as a high-value end-user segment, leveraging high-purity zirconia derived from ZrOCl₂ for dielectric coatings, optical thin films, and gate oxide layers in advanced device fabrication.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/308868/zirconium-oxychloride-for-zirconia-precursor-market

Competitive Landscape:

The global Zirconium Oxychloride (ZrOCl₂) for Zirconia (ZrO₂) Precursor market is characterized by a concentrated group of established chemical manufacturers, with Chinese producers commanding the dominant share of global supply capacity. The market is semi-consolidated, shaped by intense competition on quality consistency, purity specifications, and production scale. Chinese manufacturers hold the most prominent position in this market, given China's abundant zircon sand processing infrastructure and its role as the world's leading producer of zirconium chemicals. Companies such as Shandong Hongyuan New Material Technology Co., Ltd. and Zibo Jinkun Chemical Co., Ltd. have established themselves as high-volume producers, while European and Japanese players such as Saint-Gobain ZirPro (France) and Nippon Denko Co., Ltd. (Japan) differentiate on product quality and technical service for premium-grade applications. The competitive strategy across the landscape is overwhelmingly focused on advancing purification process technologies, expanding production capacity, and forming strategic vertical partnerships with downstream zirconia ceramic manufacturers to co-develop and validate application-specific precursor grades.

List of Key Zirconium Oxychloride (ZrOCl₂) Companies Profiled:

● Shandong Hongyuan New Material Technology Co., Ltd. (China)

● Saint-Gobain ZirPro (France)

● Zibo Jinkun Chemical Co., Ltd. (China)

● Nippon Denko Co., Ltd. (Japan)

● Guangdong Shaoneng Group Co., Ltd. (China)

● Tata Chemicals Limited (India)

● Jiangxi Kingan Hi-Tech Co., Ltd. (China)

● Showa Denko K.K. (Japan)

● Luxfer MEL Technologies (United Kingdom)

● Shandong Zibo Chemicals Co., Ltd. (China)

The competitive strategy across all major participants is overwhelmingly focused on advancing R&D to enhance precursor purity and reduce production costs, alongside forming strategic vertical partnerships with downstream zirconia powder manufacturers and ceramics companies to co-develop and validate new application-specific grades, thereby securing long-term demand relationships.

Regional Analysis: A Global Footprint with Distinct Leaders

● Asia-Pacific: Is the undisputed regional leader, anchored by China's commanding position as both the world's dominant producer and a major consumer of ZrOCl₂. The region benefits from vertically integrated supply chains spanning zircon sand processing through to ceramics manufacturing, cost-competitive production, and strong policy support for advanced materials industries. Japan and South Korea contribute premium demand driven by their world-class electronics, fuel cell, and specialty coatings industries, while India is emerging as a noteworthy growth corridor with expanding investments in technical ceramics and surface coating applications.

● North America & Europe: Together they represent technically sophisticated, premium-grade markets. North America is driven by well-established end-use industries in advanced ceramics, aerospace thermal barrier coatings, nuclear applications, and medical implants. Europe maintains a significant presence characterized by high technical standards, strong regulatory frameworks, and demand concentrated in dental zirconia, surface engineering, and catalytic materials. Both regions rely considerably on imports for raw zirconium materials while maintaining specialized processing capabilities and stringent quality requirements.

● South America, Middle East & Africa: These regions represent the emerging and nascent frontier of the ZrOCl₂ precursor market. While currently smaller in scale, Africa holds strategic upstream importance as a source region for zircon mineral sands through South Africa, Mozambique, and Senegal. Brazil serves as the principal South American market, supported by a growing ceramics industry. The Middle East is gradually building demand through industrial diversification efforts. These regions collectively present significant long-term growth opportunities as industrialization deepens and advanced materials adoption expands.

Get Full Report Here: https://www.24chemicalresearch.com/reports/308868/zirconium-oxychloride-for-zirconia-precursor-market

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/308868/zirconium-oxychloride-for-zirconia-precursor-market

About 24chemicalresearch

Founded in 2015, 24chemicalresearch has rapidly established itself as a leader in chemical market intelligence, serving clients including over 30 Fortune 500 companies. We provide data-driven insights through rigorous research methodologies, addressing key industry factors such as government policy, emerging technologies, and competitive landscapes.

● Plant-level capacity tracking

● Real-time price monitoring

● Techno-economic feasibility studies

International: +1(332) 2424 294 | Asia: +91 9169162030

Website: https://www.24chemicalresearch.com/