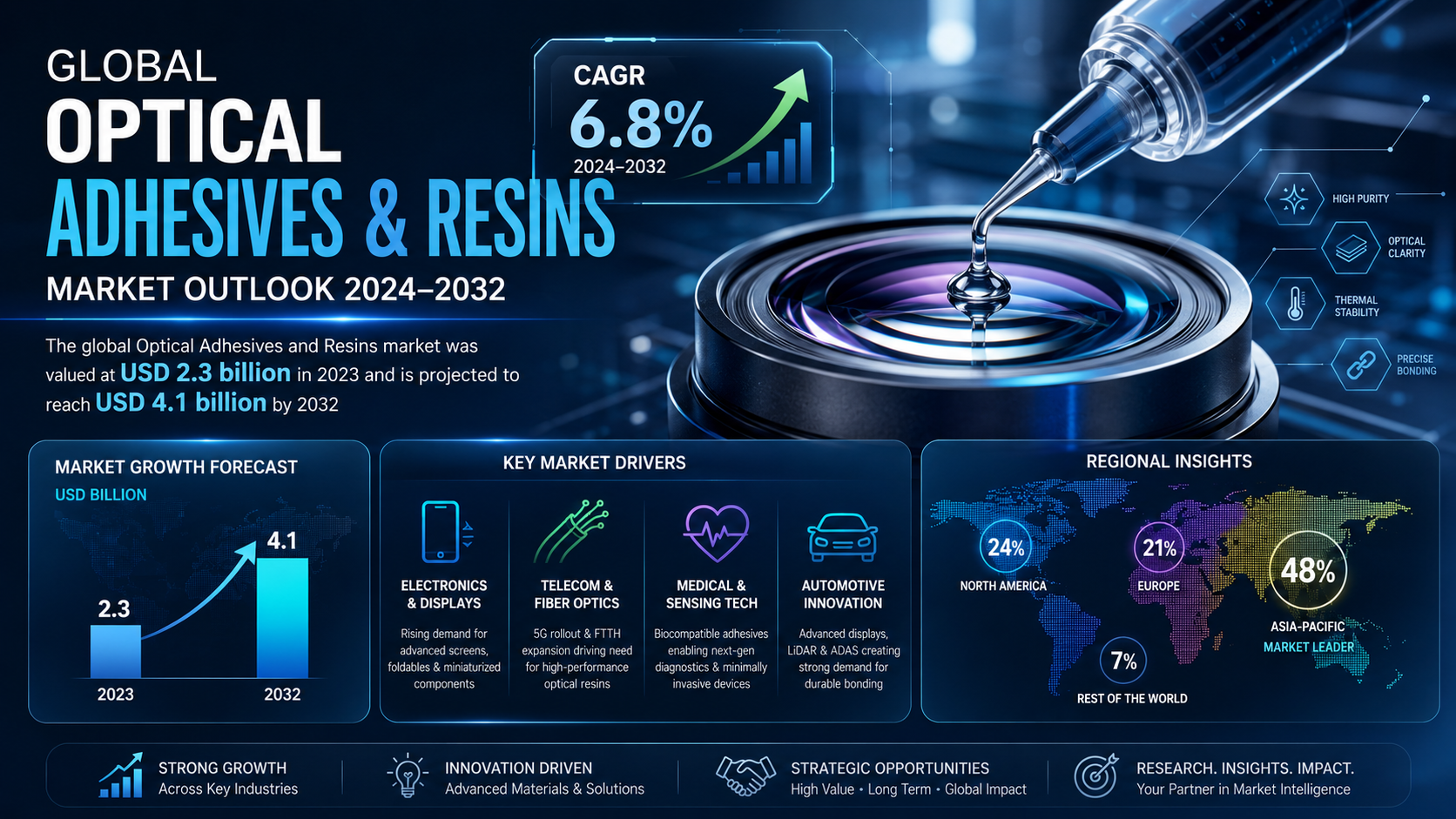

The global Optical Adhesives and Resins market was valued at USD 2.3 billion in 2023 and is projected to reach USD 4.1 billion by 2032, exhibiting a steady CAGR of 6.8% during the forecast period.

Optical Adhesives and Resins represent a specialized class of high-purity materials engineered for applications demanding exceptional light transmission, thermal stability, and precise bonding. These materials, including epoxies, silicones, acrylates, and polyurethanes, have become indispensable in modern technology because they enable the assembly of sensitive optical components without compromising optical clarity or introducing mechanical stress. Their ability to maintain performance under extreme environmental conditions—ranging from sub-zero temperatures to high humidity and intense UV exposure—makes them critical enablers of innovation across electronics, telecommunications, healthcare, and automotive sectors.

Get Full Report Here: https://www.24chemicalresearch.com/reports/263302/global-optical-adhesives-resins-forecast-market-2024-2030-455

Market Dynamics:

The market's trajectory is shaped by a complex interplay of powerful growth drivers, significant restraints that are being actively addressed, and vast, untapped opportunities.

Powerful Market Drivers Propelling Expansion

- Explosive Growth in Consumer Electronics and Displays: The relentless demand for thinner, lighter, and more robust consumer electronics represents the primary growth engine. Optical adhesives are crucial in bonding cover glass to displays and sensors in smartphones, tablets, and laptops, a market that ships over 1.5 billion units annually. The advent of foldable displays has created a new frontier, requiring adhesives with unprecedented flexibility and durability to withstand 200,000+ bending cycles. Furthermore, the miniaturization trend in automotive displays and AR/VR headsets is pushing the boundaries of material science, demanding optically clear adhesives (OCAs) with refractive indices perfectly matched to glass and polycarbonate substrates to eliminate ghosting and glare.

- Revolution in Telecommunications and Fiber Optics: The global rollout of 5G infrastructure and the ongoing expansion of fiber-to-the-home (FTTH) networks are creating massive demand for high-performance optical resins. These materials are used to pot and protect delicate fiber optic connectors and splices, ensuring signal integrity by mitigating issues like insertion loss and back reflection, which can degrade network performance by up to 15%. With the global fiber optics market projected to exceed $9 billion by 2028, the need for resins that can withstand thermal cycling from -40°C to 85°C while maintaining a stable refractive index is more critical than ever.

- Advances in Medical and Sensing Technologies: The medical device and diagnostic sector relies heavily on biocompatible optical adhesives for assembling endoscopes, biosensors, and laser-based medical equipment. These materials must pass stringent ISO 10993 biocompatibility tests and often require autoclave stability at 134°C. In diagnostic applications, the precision bonding of lenses in PCR machines and DNA sequencers is vital for accuracy. The rapid growth of minimally invasive surgery, which increases the demand for sophisticated endoscopic systems by 7-10% annually, is a significant and sustained driver for high-reliability optical bonding solutions.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/263302/global-optical-adhesives-resins-forecast-market

Significant Market Restraints Challenging Adoption

Despite its promise, the market faces hurdles that must be overcome to achieve universal adoption.

- High Material Costs and Complex Processing: The synthesis of high-purity, optical-grade materials requires ultra-refined raw ingredients and controlled manufacturing environments, elevating production costs by 30-50% compared to standard industrial adhesives. Furthermore, the application processes often demand capital-intensive equipment like precision dispensers, degassing chambers, and UV curing systems, which can represent an investment of $200,000 to $500,000 for a production line. This high barrier to entry can deter smaller manufacturers from adopting the latest optical bonding technologies, especially for low-volume, high-mix production.

- Stringent Regulatory and Performance Standards: In sectors like medical devices and automotive, certification timelines are lengthy and arduous. Achieving USP Class VI certification for medical use or specific automotive OEM qualifications can take 18 to 24 months. The materials must also comply with evolving regulations like REACH and RoHS, which restrict the use of certain chemical substances. Any reformulation to comply with new regulations can cost manufacturers between $250,000 and $1 million and delay product launches, creating significant uncertainty and risk.

Critical Market Challenges Requiring Innovation

The transition from laboratory success to industrial-scale manufacturing presents its own set of challenges. Achieving consistent cure kinetics and bubble-free bonds on high-speed assembly lines is difficult, with yield rates for complex assemblies sometimes starting below 85%. Furthermore, balancing key properties is a perennial challenge; for instance, improving impact resistance can sometimes slightly reduce optical clarity, and enhancing thermal stability might affect flexibility. These trade-offs require sophisticated chemical engineering and extensive validation testing.

Additionally, the market contends with a complex global supply chain for key raw materials like specialized epoxies and silicones. Geopolitical tensions and trade policies can disrupt availability and cause price volatility of 10-20% annually. The just-in-time manufacturing models prevalent in electronics are particularly vulnerable to these disruptions, potentially halting production lines and costing millions in lost revenue.

Vast Market Opportunities on the Horizon

- Next-Generation Automotive Applications: The automotive industry is a burgeoning frontier. The average high-end vehicle now contains over 10 square feet of display surfaces, from digital dashboards to head-up displays (HUDs) and center consoles. Optical adhesives are essential for bonding these large, curved, and complex-shaped glass panels. Furthermore, the rise of LiDAR and advanced driver-assistance systems (ADAS) requires durable optical bonding for sensors that must remain functional and clear for the entire 15-year lifespan of a vehicle, creating a loyal and high-value market segment.

- Green Technology and Energy Efficiency: Optical resins play a pivotal role in renewable energy. In the solar industry, they are used as encapsulants for photovoltaic cells, protecting them from environmental degradation while maximizing light transmission to improve efficiency by 2-4%. With the global push towards renewables, this application presents a substantial growth avenue. Similarly, the development of light-emitting capacitors (LECs) and organic light-emitting diodes (OLEDs) for energy-efficient lighting depends on advanced optical adhesives for encapsulation and bonding, opening new possibilities in smart building technologies.

- Collaborative R&D and Custom Formulations: The market is witnessing a shift towards deep collaboration between material suppliers and OEMs. Over 40 major co-development partnerships were formed in the last two years to create application-specific formulations. For example, partnerships between adhesive manufacturers and smartphone companies have yielded products with unique properties like automated bubble expulsion and tunable refractive indices. These alliances are crucial for solving specific design challenges, reducing time-to-market by up to 35%, and creating highly differentiated, value-added products that command premium prices.

In-Depth Segment Analysis: Where is the Growth Concentrated?

By Type:

The market is segmented into Optical Adhesives and Optical Resins. Optical Adhesives, particularly UV-curable acrylics and epoxies, currently lead the market. They are favored for their rapid curing times (seconds versus hours), which is critical for high-throughput electronics manufacturing. Their versatility allows for bonding a wide range of substrates, including glass, metal, and various plastics. Optical Resins, often silicone-based, are essential for potting and encapsulation applications where extreme environmental resistance and long-term stability are paramount, such as in outdoor fiber optic splices and under-the-hood automotive sensors.

By Application:

Application segments include Fiber Optics, Lenses and Prisms, LEDs and Displays, Optical Sensors, and Others. The LEDs and Displays segment is the dominant force, driven by the ubiquitous demand for consumer electronics and the rapid adoption of energy-efficient lighting solutions. However, the Optical Sensors segment is poised for the highest growth rate, fueled by the expansion of IoT devices, automotive ADAS, and industrial automation, all of which rely on precisely assembled sensors to function accurately.

By End-User Industry:

The end-user landscape includes Electronics, Automotive, Telecommunications, Healthcare, and Others. The Electronics industry is the largest consumer, utilizing these materials in nearly every device with a screen or sensor. The Automotive and Healthcare sectors are emerging as the fastest-growing end-users, reflecting the increased electronic content in modern vehicles and the ongoing technological revolution in medical diagnostics and treatment equipment.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/263302/global-optical-adhesives-resins-forecast-market-2024-2030-455

Competitive Landscape:

The global Optical Adhesives and Resins market is fragmented and highly competitive, characterized by continuous innovation and strategic positioning. The top three companies—Henkel (Germany), Dow Inc. (U.S.), and DELO Industrial (Germany)—collectively command approximately 40% of the market share as of 2023. Their leadership is cemented by extensive research and development capabilities, a broad portfolio of patented technologies, and global manufacturing and support networks that cater to the just-in-time needs of major multinational customers.

List of Key Optical Adhesives and Resins Companies Profiled:

● Henkel (Germany)

● Dow Inc. (U.S.)

● DELO Industrial (Germany)

● 3M (U.S.)

● NTT Advanced Technology (Japan)

● Tesa SE (Germany)

● Nitto Denko Corporation (Japan)

● Lintec Corporation (Japan)

● Saint-Gobain (France)

● Dymax Corporation (U.S.)

● Hitachi Chemical (Japan)

● Cyberbond LLC (U.S.)

● Toray Industries (Japan)

● ITW (U.S.)

● H.B. Fuller (U.S.)

● Hexion (U.S.)

● Mitsubishi Chemical (Japan)

● Shinetsu (Japan)

● Daikin (Japan)

● Panacol-Elosol GmbH (Germany)

The overarching competitive strategy focuses on intensive R&D to develop novel chemistries that offer faster curing, higher performance, and better environmental compatibility. This is complemented by forming strategic, long-term partnerships with leading OEMs to co-engineer solutions tailored to next-generation products, thereby securing a pipeline of future demand.

Regional Analysis: A Global Footprint with Distinct Leaders

● Asia-Pacific: Is the dominant force, holding a 48% share of the global market. This leadership is fueled by the region's status as the world's electronics manufacturing hub, with countries like China, South Korea, Japan, and Taiwan housing the production facilities for most major consumer electronics brands. Strong government support for technology manufacturing and a vast network of component suppliers create a powerful ecosystem for growth.

● North America and Europe: Together, they form a highly advanced and innovation-driven bloc, accounting for 45% of the market. North America's strength lies in its robust R&D infrastructure and leadership in emerging technologies like AR/VR and advanced telecommunications. Europe excels in high-value manufacturing, particularly in the automotive and industrial sectors, where precision and reliability are paramount, driving demand for the highest quality optical materials.

● Rest of the World (ROW): These regions, including South America and the Middle East & Africa, represent the emerging growth frontier. While currently a smaller market, increasing industrialization, investments in telecommunications infrastructure, and the growing adoption of advanced technology are expected to drive significant future demand, offering long-term expansion opportunities for market players.

Get Full Report Here: https://www.24chemicalresearch.com/reports/263302/global-optical-adhesives-resins-forecast-market-2024-2030-455

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/263302/global-optical-adhesives-resins-forecast-market-2024-2030-455

About 24chemicalresearch

Founded in 2015, 24chemicalresearch has rapidly established itself as a leader in chemical market intelligence, serving clients including over 30 Fortune 500 companies. We provide data-driven insights through rigorous research methodologies, addressing key industry factors such as government policy, emerging technologies, and competitive landscapes.

● Plant-level capacity tracking

● Real-time price monitoring

● Techno-economic feasibility studies

International: +1(332) 2424 294 | Asia: +91 9169162030

Website: https://www.24chemicalresearch.com/